Author : Haya Assem

A Comprehensive Guide to Current Liabilities

Table of contents:

- Key Takeaways

- What Are Current Liabilities?

- Current Liabilities Examples

- Importance Of Current Liabilities In Accounting

- How To Calculate Current Liabilities

- Current VS Long-Term Liabilities

- Streamlining Current Liabilities Calculation With Enerpize ERP Software

- Conclusion

- FAQs About Current Liabilities

Current liabilities are short-term financial obligations a business must settle within a year. Understanding and managing these obligations is essential for maintaining financial stability and making informed business decisions. In this guide, you’ll learn what current liabilities are, how to calculate them, and how modern ERP tools simplify the process.

Key Takeaways

- Current liabilities are short-term obligations due within 1 year and are essential for measuring a company’s liquidity and financial health.

- Examples include accounts payable, accrued wages, short-term loans, taxes payable, unearned revenue, and current portions of long-term debt.

- These liabilities directly affect key financial metrics, such as the current ratio, quick ratio, and cash ratio.

- Accurate calculation involves listing all short-term obligations, summing them up, and excluding long-term debts.

- Current vs. long-term liabilities differ in duration and financial impact: short-term liabilities affect liquidity; long-term liabilities impact long-range solvency.

- Effective liability management supports better cash flow planning, creditworthiness, and informed decision-making.

What Are Current Liabilities?

The current liabilities definition is short-term financial obligations that a company is legally required to pay within a short period, usually one year. These liabilities are frequently generated from day-to-day business activities and might include accounts payable, short-term loans, accrued expenses, taxes payable, and other similar debts.

Current (short-term) liabilities are a key component of a company's balance sheet since they help determine its short-term financial health and liquidity. Managing current liabilities ensures that a company can meet its commitments without affecting operations or cash flow.

Current Liabilities Examples

Understanding what falls under current liabilities is essential for maintaining accurate financial records. When preparing the trial balance, all current liabilities must be recorded accurately to ensure that debits and credits balance.

The following are common examples of current liabilities that companies typically record in their accounting systems:

1- Accounts Payable

Accounts payable (AP) are the short-term financial obligations a company owes to its suppliers or creditors for goods or services that have been received but not yet paid.

These obligations arise from routine business transactions and are recorded on the balance sheet under current liabilities, reflecting amounts that must typically be settled within a short period.

When a company receives goods or services on credit, the supplier issues an invoice, and the company records the amount as accounts payable in its accounting records.

In essence, accounts payable represent the total value of unpaid supplier invoices and serve as a form of short-term financing, allowing the business to obtain the resources it needs before making payment.

From a financial management perspective, accounts payable play a key role in working capital management. While suppliers prefer shorter payment cycles to maintain their own cash flow, businesses may strategically manage payment timing to preserve cash in the short term—provided this is done without harming supplier relationships.

Example: If a business receives raw materials worth $3,000 but hasn't paid the supplier yet, that $3,000 is recorded as accounts payable.

2- Wages Payable

Wages Payable (or Salaries Payable) is a current liability representing the total amount of salaries and wages earned by employees but not yet paid by the company at a specific point in time. These amounts arise from routine payroll activities and are recorded as obligations until they are settled.

Because employee compensation is usually paid on a weekly, biweekly, or monthly basis, any unpaid portion at the end of an accounting period is classified as a current liability on the balance sheet.

In addition to basic wages and salaries, payroll-related obligations due within the year—such as amounts withheld for taxes or employee benefits (e.g., health insurance premiums or retirement contributions)—may also be included as part of these short-term liabilities.

Wages payable reflect the company’s responsibility to compensate employees for work already performed, making it an essential component of accurate financial reporting and short-term cash flow planning.

You may need: Payroll Template

3- Taxes Payable

Taxes Payable is a current liability representing the taxes a company owes to government authorities but has not yet paid. These obligations arise from the company’s financial activities and must typically be settled within a short period, which is why they are classified as short-term liabilities on the balance sheet.

Taxes payable may include several types of taxes depending on the business’s operations. The most common examples include income taxes owed on company profits, payroll taxes withheld from employees but not yet remitted, and taxes collected from customers—such as sales tax or VAT—that must be paid to the government.

Together, these obligations reflect the company’s responsibility to transfer collected or accrued taxes to the appropriate authorities within the required timeframe, making taxes payable an essential component of accurate financial reporting and compliance.

You may need: Google Sheets Tax Template

4- Short-Term Loans

Short-Term Debt is a current liability that represents all financial obligations a company must repay within the next 12 months. It includes various forms of borrowing used to support day-to-day operations, such as short-term bank loans, lines of credit, overdraft facilities, short-term leases, and other short-term financing arrangements.

The portion of long-term debt that becomes due within the coming year is also classified as short-term debt.

Short-term debt plays a key role in working capital management, providing businesses with immediate funding for operational needs such as payroll, inventory, and supplier payments. Some companies may also raise funds through instruments such as commercial paper, which is an unsecured, short-term promissory note issued to cover temporary financing needs.

From a financial analysis perspective, the ratio of short-term to long-term debt is an important indicator of a company’s liquidity and risk profile. A business with a high proportion of short-term obligations may face cash flow pressure if it does not generate sufficient revenue to meet upcoming payments.

This could impact its ability to maintain operations smoothly or meet commitments, such as dividend payments to shareholders.

Therefore, effectively managing short-term debt is essential for maintaining financial stability, ensuring liquidity, and supporting ongoing business operations.

5- Unearned Revenue (Deferred Revenue)

Unearned revenue refers to payments a company receives in advance for goods or services that have not yet been delivered or performed. Because the company still has an obligation to fulfill its promise to the customer, this amount is recorded as a current liability on the balance sheet.

Once the product is delivered or the service is completed, the liability is reduced, and the amount is recognized as earned revenue in the income statement.

Example: If a customer pays $2,000 upfront for a one-year software subscription, and 10 months remain, that unearned portion is a current liability.

6- Accrued Liabilities

Accrued Expenses are costs that a company has incurred during a specific accounting period but has not yet paid or recorded through a standard transaction.

Under the accrual basis of accounting, expenses are recognized when they are incurred rather than when cash is paid, so these amounts must be captured through adjusting entries at the end of the month or year.

During the closing process, the company records an adjusting journal entry that debits the appropriate expense account and credits an accrued expenses liability account to reflect the outstanding obligation. At the beginning of the following accounting period, this entry is typically reversed so the actual payment can be recorded correctly when it occurs.

Accrued expenses are presented in the current liabilities section of the balance sheet because they represent short-term obligations expected to be settled within a year using current assets, such as cash.

Common examples of accrued expenses include supplies received but not yet invoiced, interest on loans that have accrued but not yet been paid, and warranty obligations related to products or services.

They also include real estate and property taxes accumulated over a period, accrued government taxes, and employee-related costs such as wages, bonuses, and commissions that have been earned but will be paid in a subsequent period.

Example: An unpaid electricity bill of $300 that covers the last two weeks of the month would fall under accrued expenses.

7- Dividends Payable

Dividends Payable is a current liability that arises when a company’s board of directors formally approves and declares a cash dividend to shareholders. At the time of declaration, even though the cash has not yet been paid, the company records a liability because it has committed to distributing funds in the near term.

The amount recorded as dividends payable equals the total dividend declared and is presented on the balance sheet as a short-term obligation. From an accounting perspective, the declaration reduces retained earnings and creates a corresponding payable, meaning retained earnings are debited, and dividends payable are credited.

The actual cash outflow occurs later, on the payment date, when the dividends payable account is cleared (debited) and cash is reduced (credited). Although dividends are typically distributed after declaration, it is important to note that they are discretionary decisions made by management and are not legally binding obligations like interest payments on debt.

8- Current Portion of Long-Term Debt

The Current Portion of Long-Term Debt refers to the portion of a company’s long-term borrowings that is due for repayment within the next 12 months. Although these debts are part of long-term obligations, the portion that will be settled within the upcoming year is classified as a current liability on the balance sheet.

This distinction helps users of financial statements understand the company’s short-term repayment obligations separately from its long-term debt commitments.

Importance Of Current Liabilities In Accounting

Current liabilities affect a company's short-term financial health and operational efficiency. They reflect immediate obligations a business must meet, making them essential for several vital accounting operations and financial decisions.

Assessing Liquidity

These current liabilities directly affect key liquidity metrics, making their proper management crucial for meeting short-term obligations and maintaining financial stability, such as:

- The current ratio measures a company’s ability to cover its current liabilities with its current assets.

- The quick ratio (or acid-test ratio) evaluates liquidity using only the most liquid assets, excluding inventory

- The cash ratio measures a company’s ability to pay current liabilities with only cash and cash equivalents.

Monitoring these ratios helps ensure that the company maintains sufficient liquidity to meet its short-term obligations. According to research published in the Transnational Academic Journal of Economics in 2020, companies that strategically balance current liabilities and current assets not only maintain better liquidity but also enhance profitability and financial stability.

- Example: if a business has $50,000 in current assets and $30,000 in current liabilities, its current ratio is 1.67—indicating a healthy liquidity position.

Supporting Cash Flow Management

Businesses can better manage cash flow by monitoring current liabilities, as knowing when payments are due, such as loans, taxes, or supplier invoices, helps ensure timely disbursements.

May Help You: How to Calculate Net Cash Flow

Providing Insight Into Financial Stability

A manageable level of short term liabilities suggests operational discipline. On the other hand, consistently rising short-term obligations without corresponding growth in assets may indicate financial strain.

Guiding Credit and Investing Decisions

Lenders and investors often review a company’s current liabilities to assess risk. A high liability-to-asset ratio might make it harder to secure loans or favorable credit terms.

Ensuring Accurate Financial Reporting

Correctly classifying liabilities ensures that financial statements, especially the balance sheet, accurately represent a company’s financial position, which is vital for audits, compliance, and strategic planning.

You may also like: What Is Contingent Liability in Accounting?

How To Calculate Current Liabilities

Calculating current liabilities is straightforward: add up all short-term financial obligations a business must settle within 1 year.

These typically include accounts payable, accrued expenses, short-term loans, taxes payable, and any portion of long-term debt due within the year. The exact components may vary depending on the business and its operations. Follow the steps below to accurately calculate current liabilities:

Step 1: List All Short-Term Obligations

Identify all liabilities that are due within 12 months or your business’s operating cycle. These short-term obligations vary from one business to another. They may include:

- Accounts payable

- Accrued expenses (e.g., wages, utilities)

- Short-term loans

- Taxes payable

- Unearned revenue

- Current portion of long-term debt

Step 2: Gather the Amounts

Look into your accounting records or balance sheet and note the outstanding amounts for each liability.

Step 3: Use the Formula

Apply the current liabilities formula:

Current Liabilities = Accounts Payable + Accrued Expenses + Short-Term Debt + Other Short-Term Obligations

Step 4: Verify and Classify Correctly

Ensure that only liabilities due within one year are included. Exclude long-term debts and non-financial obligations.

Example

A small retail store is reviewing its finances at the end of the fiscal quarter. The goal is to calculate the store’s current liabilities to understand its short-term financial obligations and prepare accurate financial statements. The following liabilities are due within the next 12 months:

- Accounts Payable: $6,200

- Accrued Wages: $2,800

- Short-Term Loan: $10,000

- Taxes Payable: $1,500

- Unearned Revenue: $3,000

- Current Portion of Long-Term Debt: $4,000

Current Liabilities = 6,200 + 2,800 + 10,000 + 1,500 + 3,000 + 4,000 = $27,500

So, the total current liabilities for this business would be $27,500.

Manually tracking current liabilities can be error-prone and time-consuming. Enerpize ERP automates processes, accurately managing accounts payable, accrued expenses, short-term loans, and taxes, while providing real-time reports and liquidity insights—no manual calculations required.

Read also: How to Calculate Liabilities: Formula and Examples

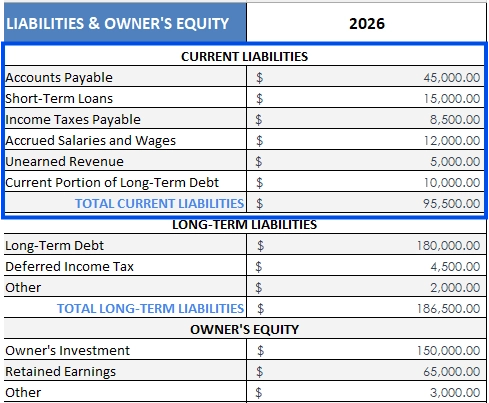

Current VS Long-Term Liabilities

Businesses often carry both current and long-term liabilities as part of their financial structure. These obligations vary based on when they are due and their impact on a company’s liquidity and financial planning.

Current liabilities are short-term obligations due within a year, while long-term liabilities are debts or commitments payable beyond one year. Understanding the distinction between the two is critical for assessing a company's short-term liquidity and long-term financial stability.

Below is a structured comparison that outlines the key differences between current and long-term liabilities:

| Feature | Current Liabilities | Long-Term Liabilities |

| Definition | Financial obligations a business must settle within one year or its operating cycle. | Obligations not due for settlement within the next 12 months. |

| Purpose | Evaluate a company's ability to meet short-term obligations. | Assess a company’s long-term financial commitments and sustainability. |

| Payment Duration | Due within one year or less. | Due in more than one year. |

| Examples | Accounts payable, salaries, taxes payable, and short-term loans. | Bonds payable, long-term loans, deferred tax liabilities, and lease obligations. |

| Impact on Financials | Directly affect short-term liquidity and working capital. | Influence long-term solvency and debt management. |

| Used in Calculating | Current ratio, quick ratio, and other liquidity ratios. | Debt-to-equity ratio, solvency ratios, and leverage analysis. |

| Financial Management Focus | Prioritize cash flow management and short-term funding. | Emphasize long-term investment planning and capital structure management. |

Streamlining Current Liabilities Calculation With Enerpize ERP Software

Based on everything discussed in this article, current liabilities play a key role in assessing a business’s short-term financial health, but managing them can quickly become complex.

As a business grows and transactions increase, tracking current liabilities manually becomes time-consuming and error-prone. That’s where Enerpize Online Accounting Software makes a difference by automating liability tracking and delivering real-time financial insights, which helps businesses stay accurate, efficient, and in control.

How Enerpize Makes It Easier:

- Automated Classification: As soon as purchases, expenses, or payroll are recorded, Enerpize auto-updates related liability accounts (e.g., accounts payable, accrued wages, short-term debt) directly in the chart of accounts.

- Live Balance Sheet Insights: Enerpize’s real-time reporting shows current liabilities side-by-side with current assets, making it easy to monitor liquidity and calculate ratios like the cash ratio, current ratio, and quick ratio instantly.

- Comprehensive Financial Reporting: With built-in reports, P&L, balance sheet, and cash flow, Enerpize automatically includes current liabilities in your financial statements, enhancing accuracy and compliance.

- Seamless Module Integration: Whether expenses are captured via purchases, payroll, or inventory, those entries flow into liability accounts automatically, eliminating redundant data entry.

Conclusion

Current liabilities are a cornerstone of a company’s short-term financial health, directly impacting liquidity, cash flow, and operational efficiency. Properly identifying, monitoring, and managing these obligations—from accounts payable and accrued wages to short-term loans and taxes—ensures that a business can meet its immediate commitments while maintaining financial stability.

Manual tracking of these liabilities can be time-consuming and error-prone, which is why modern ERP solutions like Enerpize are invaluable. By automating classification, updating balances in real time, and integrating across accounting, payroll, and inventory modules, Enerpize simplifies liability management, enhances reporting accuracy, and provides actionable insights into liquidity and financial performance.

In short, effective current liabilities management not only safeguards a company’s day-to-day operations but also strengthens its long-term financial decision-making and strategic planning.

FAQs About Current Liabilities

Are notes payable current liabilities?

Yes, notes payable are considered current liabilities if they are due within one year. If the repayment period extends beyond 12 months, they are classified as long-term liabilities.

What are current liabilities on a balance sheet?

On the balance sheet, current liabilities appear under liabilities and include short-term obligations such as accounts payable, wages payable, taxes payable, and short-term loans, typically due within a year.

How to find current liabilities?

To find current liabilities, check the liabilities section of the balance sheet. Add up all line items due within 1 year.

Are bonds payable current liabilities?

No, bonds payable are usually classified as long-term liabilities unless the bond matures within the next 12 months; in that case, the portion due is moved to current liabilities.

Are retained earnings current liabilities?

No, retained earnings are not liabilities at all. They represent accumulated net profits and are reported under shareholders’ equity, not as liabilities.

What are considered current liabilities?

Common current liabilities include:

- Accounts payable

- Accrued wages and expenses

- Short-term loans

- Taxes payable

- Unearned revenue

- Current portion of long-term debt

What are non-current liabilities?

Non-current liabilities, also called long-term liabilities, are debts and obligations not due within one year.

Are accrued expenses current liabilities?

Yes, accrued expenses such as unpaid wages, utilities, or interest are current liabilities because they are obligations incurred but not yet paid, due within a short period.

What are short-term liabilities?

Short-term liabilities are another term for current liabilities. These obligations are due within one year and directly impact a company’s liquidity and cash flow.

How to manage short-term liabilities?

To manage short-term liabilities effectively:

- Track due dates using accounting software like Enerpize

- Maintain sufficient cash reserves

- Monitor liquidity ratios (e.g., cash ratio, current ratio)

- Prioritize high-interest or time-sensitive payments

Managing current liabilities is easy with Enerpize.

Try Enerpize accounting software to track and manage current liabilities automatically.

Managing current liabilities is easy with Enerpize.

Try Enerpize accounting software to track and manage current liabilities automatically.