Author : Haya Assem

Reviewed By : Enerpize Team

What Are Lease Journal Entries: Types, Standards & Calculating Steps

Key Takeaways

- Lease Journal Entries record financial transactions for asset leasing, covering initial recognition, ongoing payments, and expenses.

- There are two main types: Finance/Capital Leases and Operating Leases.

- Finance/Capital Leases transfer ownership risks, requiring recognition of a Right-of-Use (ROU) asset and lease liability on the balance sheet. Payments are then split into interest expense and principal repayment.

- Operating Leases don't transfer ownership risks; payments are typically recorded as straight-lined lease expenses on the income statement.

- Key Lease Accounting Standards include ASC 842 (US GAAP) and IFRS 16 (International), both generally requiring lessees to recognize ROU assets and lease liabilities for most leases.

- Calculating entries involves determining lease classification, calculating the present value of lease payments, and then recording distinct initial and subsequent journal entries based on lease type.

What is a Journal Entry for Lease?

A journal entry for a lease records the financial transactions related to the leasing of an asset. This involves documenting the initial recognition of lease obligations and assets, as well as ongoing payments and expenses. For a finance lease, the entry includes recognizing a right-of-use asset and a corresponding lease liability on the balance sheet. For an operating lease, the lease payments are recorded as lease expenses in the income statement. The entries ensure accurate tracking of the lease's impact on financial statements and compliance with accounting standards.

Lease Journal Entries Types

Lease journal entries generally fall into two main types, depending on the nature of the lease. Under ASC 842 lease accounting journal entries, distinct treatments are applied for different lease types.

1. Finance / Capital Lease Accounting Journal Entries

Finance lease accounting journal entries, also known as a capital lease, transfer substantially all the risks and rewards of ownership of the leased asset to th lessee. Under ASC 842, the lessee is required to recognize a Right-of-Use (ROU) asset and a corresponding lease liability on the balance sheet at the commencement of the lease.

The lease liability is measured at the present value of the lease payments, while the ROU asset is initially measured as the sum of the lease liability and any direct costs incurred. Subsequent lease payments are split between interest expense (on the liability) and principal repayment.

Initial Recognition

- Debit: Right-of-Use Asset (ROU)

- Credit: Lease Liability

Subsequent Payments

- Debit: Interest Expense (portion of the payment that is interest)

- Debit: Lease Liability (portion of the payment that reduces the principal)

- Credit: Cash

2. Operating Lease Accounting Journal Entries

Operating leases do not shift the rewards and risks of ownership to the lessee. Under ASC 842, the lessee does not recognize an asset or liability for the lease on the balance sheet, except in the case of longer-term operating leases, where the lease liability and ROU assets are still recognized. For these cases, the journal entry for operating lease would include the recognition of lease expenses as they are incurred.

Lease payments are instead treated as lease expenses and recorded on the income statement over the lease term, typically on a straight-line basis. This means the payments are expensed evenly, regardless of the actual payment schedule.

Monthly Lease Payment

- Debit: Lease Expense

- Credit: Cash

Lease Accounting Journal Entries Standards

Lease accounting journal entries are governed by specific accounting standards that provide guidelines for recognizing and recording leases. The two main standards are ASC 842 (used primarily in the US) and IFRS 16 (used internationally). Both standards aim to improve transparency and consistency in lease reporting by requiring companies to recognize lease-related assets and liabilities on their balance sheets.

1. IFRS 16 (International Financial Reporting Standards)

Lessee Accounting

- Initial Recognition: At the commencement date, the lessee recognizes a right-of-use asset and a lease liability. The liability is measured at the present value of lease payments, while the asset includes the initial lease liability and any initial direct costs.

- Subsequent Recognition: The asset is depreciated over the lease term, and the liability is reduced as payments are made with interest expense recognized on the outstanding balance.

Interest and Amortization:

The lease liability is split into two components: interest expense and amortization of the lease liability. As payments are made, the interest portion is expensed, and the remainder reduces the lease liability. The right-of-use asset is also amortized over its useful life or the lease term.

Read More: Amortization of Intangible Assets: Methods and How To Calculate

Lessor Accounting

Lessors continue to classify leases as either finance or operating leases, with different treatment for each.

2. ASC 842 (US GAAP)

Lessee Accounting

Similar to IFRS 16, lessees recognize a right-of-use asset and a lease liability on the balance sheet for both finance and operating leases.

The finance lease results in interest and depreciation expenses, while operating leases show a single lease expense typically straight-lined over the lease term.

Lessor Accounting

Lessors classify leases as either sales-type, direct financing, or operating leases based on the transfer of risks and rewards.

These standards ensure leases are reflected on the balance sheet, enhancing transparency and consistency in financial reporting.

Read Also: What Is A Sales Journal Entry?

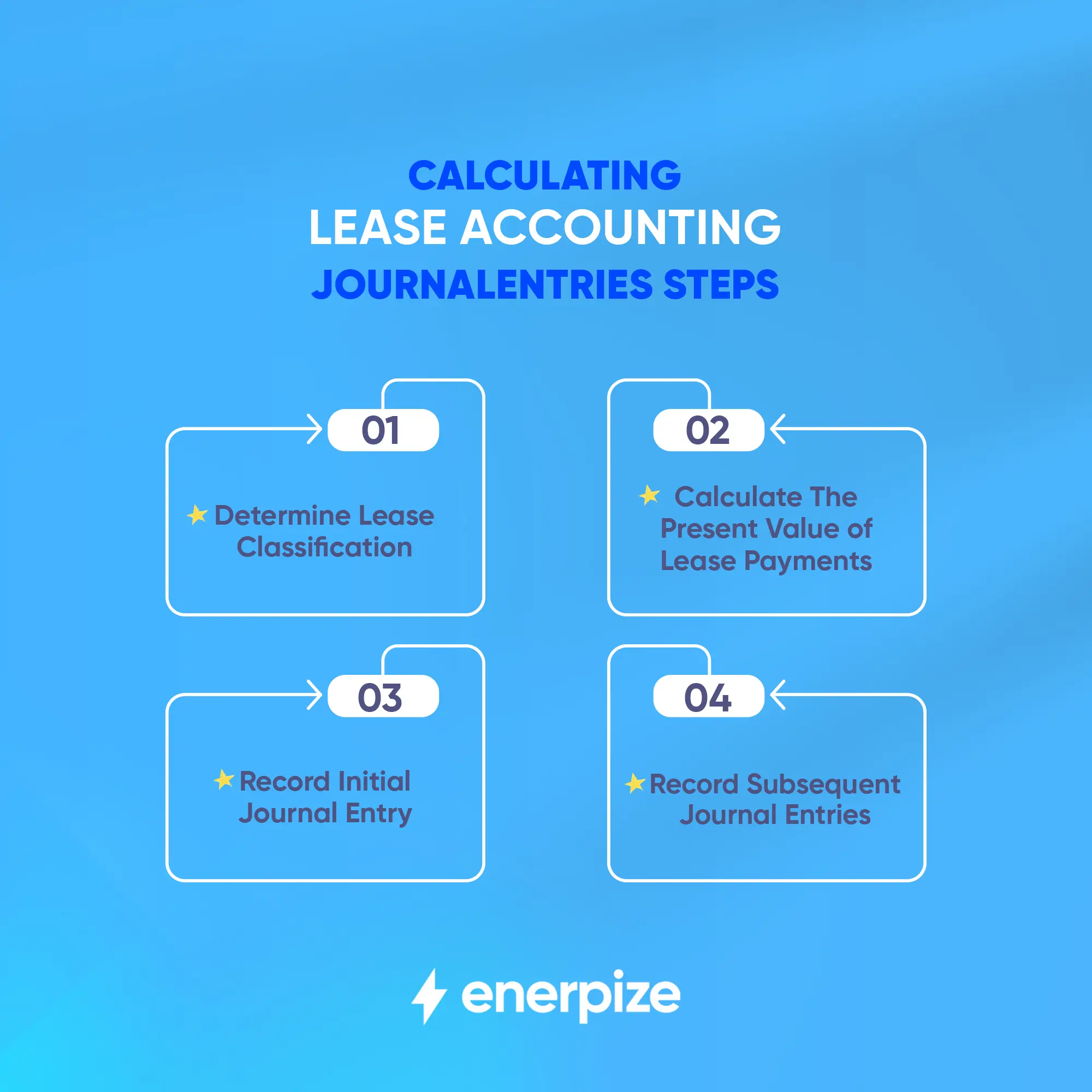

Calculating Lease Accounting Journal Entries Steps

Here are the steps for calculating lease accounting journal entries:

1- Determine Lease Classification

- Finance Lease: If the lease transfers substantially all the risks and rewards of ownership to the lessee, it's classified as a finance lease.

- Operating Lease: A lease is classified as an operating lease if it does not transfer most of the rewards and risks of ownership to the lessee.

2- Calculate the Present Value of Lease Payments

Use the lessee's incremental borrowing rate or the implicit rate in the lease (if determinable) to discount future lease payments. Consider any guaranteed residual value or purchase option.

3- Record Initial Journal Entry

Finance Lease:

- Debit ROU asset (Present value of lease payments)

- Credit Lease liability (Present value of lease payments)

Operating Lease:

- Debit Lease expense (Total lease payments divided by lease term)

- Credit Cash (Lease payment)

4- Record Subsequent Journal Entries

Finance Lease:

- Debit Interest expense (Interest rate * Lease liability)

- Credit Lease liability (Principal portion of lease payment)

- Debit Amortization expense (ROU asset / Useful life of asset)

- Credit ROU asset

Operating Lease:

- Debit Lease expense (Total lease payments divided by lease term)

- Credit Cash (Lease payment)

Read Also: How to Do Journal Entries: A Comprehensive Guide

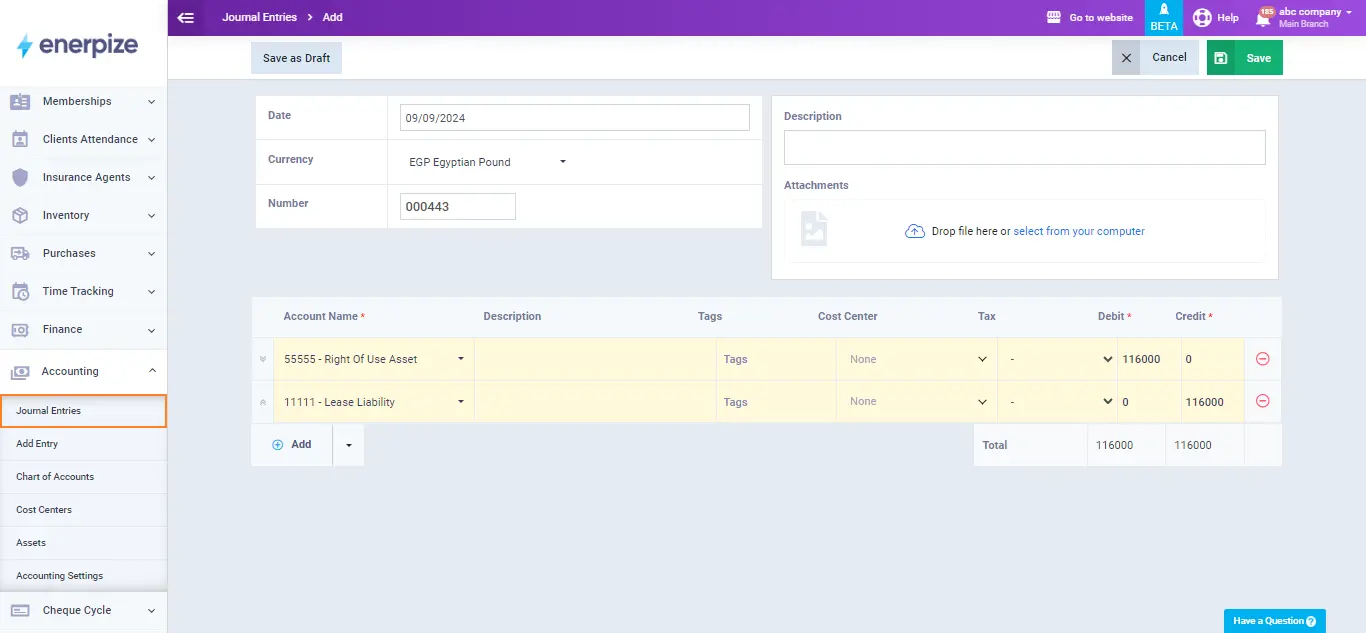

Lease Accounting Journal Entries Example

A company enters into a 5-year finance lease for a piece of equipment. The lease payments are $10,000 per year, and the implicit rate in the lease is 8%. The lease payment's present value is $41,161.

Initial Journal Entry

| Account | Debit | Credit |

| ROU Asset | 41,161 | |

| Lease Liability | 41,161 |

Subsequent Journal Entries (Year 1):

- Interest Expense

| Account | Debit | Credit |

| Interest Expense | 3,293 | |

| Lease Liability | 3,293 |

- Amortization of ROU Asset

| Account | Debit | Credit |

| Amortization Expense | 8,232 | |

| ROU Asset | 8,232 |

- Lease Payment

| Account | Debit | Credit |

| Lease Liability | 6,707 | |

| Cash | 10,000 |

Making Lease Journal Entries Easier with Enerpize

Enerpize online accounting software simplifies the process of making lease journal entries through several powerful features. Its automated tracking system minimizes manual data entry errors and saves valuable time by handling lease payments and related expenses automatically.

Users benefit from pre-built journal entry templates for common lease transactions, which ensures consistency and reduces the need for repetitive manual input. All lease-related information, including terms, payments, and accounting treatment, can be stored in one place. This makes it easier to access and update data when needed.

The system’s automated reporting capabilities allow users to easily monitor lease-related expenses and make informed financial decisions. Integration with other financial modules, such as accounts payable and the general ledger, provides a seamless workflow, enhancing overall efficiency. Additionally, Enerpize's intuitive interface makes it user-friendly, even for those without extensive accounting knowledge. Real-time updates keep users informed about their lease transactions, aiding in effective cash flow management and financial oversight.

Lease journal entries are easy with Enerpize.

Try our accounting module to handle your entries.

Lease journal entries are easy with Enerpize.

Try our accounting module to handle your entries.