Create and send online quotations and invoices, track sales, monitor staff performance, and sell & sync all your products via our POS and more.

Posted on 8 October 2024

Author : Enerpize Team

Author : Enerpize Team

Explain Cash Flow Statements: Importance and How to Use

Table of contents:

- What are Cash Flow Statements (CFS)?

- Importance of Cash Flow Statements

- Explain Cash-Flow Statements

- How to Create Cash Flow Statements?

- How to Calculate Cash Flow Statements?

- Cash Flow Statement Example

- Cash Flow Statement VS Financial Statements

- How Can Enerpize Help You in Cash Flow Statement?

- Final Thoughts

You cannot manage what you cannot measure.

Companies, big and small, always want to monitor every financial transaction. The reason is quite simple: managing financial flows—that is, inflows and outflows—not only helps companies track short-term gains and losses but, more importantly, plans long-term for possible expansions, mergers and acquisitions, investments or divestments, and more.

Cash flow statements are established financial management and planning documents everywhere. Along with a range of other financial statements and sheets, cash flow statements enable companies to identify any cash inflow or outflow gaps, reconcile for discrepancies, consolidate with one or more financial documents, and audit all for regulatory use and reporting.

However, there is a need to clarify what a cash flow statement means. Often, business owners, executive managers, and entrepreneurs —who may not necessarily be accounting experts but may only have some accounting knowledge or background—are at odds about how cash flow statements are created and calculated and how they differ from balance sheets and income statements.

This post aims to explain cash flow statements, how they work, how to calculate them, and how they compare to other critical financial statements and sheets.

What are Cash Flow Statements (CFS)?

Cash flow statements are critical financial documents that monitor a company's cash inflows (incoming) and outflows (outgoing) to establish a well-defined cash position for the company and decide whether it can generate enough cash to pay off debts and meet its obligations.

Importance of Cash Flow Statements

Cash flow statements come with many benefits for businesses. Here are some:

Managing Cash

By definition, cash flow statements aim primarily to manage a given company’s cash inflows and outflows. Unlike balance sheets and income statements (explained in a bit), cash flow statements only include records of actual cash inflow and outflow activities that have already occurred, not possible future cash flows.

Read Also: Main Differences Between Income Statement and Balance Sheet

Auditing

Adjustments can be made anytime to reconcile accounts or entries. As a record of all cash flows, cash flow statements are critical financial documents for financial control and auditing. Indeed, cash flow statements are particularly important for small companies, where cash is more common as an asset compared to bonds, stocks, and investments, which are more common at bigger companies.

Read Also: Adjusting Journal Entries: Definition, Types, and Examples

Financial Planning

As a record of all cash flows, cash flow statements - along with balance sheets and income statements - present business owners, executive managers, and investors with a clear-cut view of a company’s overall financial health and robustness. As such, cash flow statements are indispensable for financial planners, controllers, and accountants to prepare solid financial outlooks informed by just as solid financial statements.

Explain Cash-Flow Statements

Cash flow statements are straightforward financial documents. Unlike balance sheets and income statements, for example, cash flow statements are primarily made up of or generated from four main components or sources:

- Cash flow from operating activities

- Cash flow from investing activities

- Cash flow from financing activities

- Non-cash activity disclosures

For current purposes, only cash flow from operating activities, investing activities, and financing activities are of interest.

Cash Flow from Operating Activities

Cash flows generated from operating activities are incoming or outgoing cash flows a given company gains or spends from performing business activities such as sales, interest payments (to banks or from customers), income tax payments (to tax authorities), payroll, and fixed expenses (e.g., lease or mortgage). In short, operating activities cash flow refers to cash inflows or outflows resulting from operating a business.

Cash flows generated from portfolio investments, for example, are also included in cash flow statements because portfolio management is considered a business activity. However, as mentioned, portfolios, stocks, and bonds are cash sources for bigger companies, and smaller companies are more likely to generate cash from a narrower business activity window.

Cash Flow from Investing Activities

Cash flows generated from investing activities are flows produced from investments made. If a company generates cash from M&A activities, loans suppliers or customers, or sells assets, all those activities are considered inflows where cash comes in.

Conversely, cash used to buy assets (e.g., equipment or real estate) or financial instruments (e.g., bonds, securities, derivatives, etc.) is considered outflow where cash goes out.

In short, investing activities cash flow refers to cash inflows or outflows resulting from investment activities such as just been explained a given company performs.

Cash Flow from Financing Activities

Cash flows generated from financing activities are flows produced from payments made to or from banks and shareholders. For example, cash from selling bonds or dividends is considered incoming or inflow. Conversely, cash paid to shareholders in dividend form is considered outgoing or outflow. In short, financing activities cash flow refers to cash inflows or outflows resulting from financing activities a given company performs.

How to Create Cash Flow Statements?

Preparing a cash flow statement is pretty straightforward:

- Collect all required financial statements, mainly your income statement (a record of revenue, expense, and net income) and balance sheet (a record of assets, liabilities, and equity over your specified reporting period).

- Specify your reporting period on a monthly, quarterly, or annual basis, according to your financial needs.

- Select your preparation method: direct (by listing all cash-based transactions over your specified reporting period) or indirect (by starting from your net income and adjusting for non-cash transaction changes).

- Prepare your cash flow statement.

To prepare your cash flow statement, you need to do so using cash flow information from your operating, investing, and financing activities as follows:

- Cash Flow from Operating Activities:

Direct Method:

- List all cash receipts.

- List all cash payments.

- Calculate net cash flow from your operating activities by subtracting your overall cash receipts from your overall cash payments.

Indirect Method:

- Start with your net income from your income statement.

- Adjust for non-cash entries by adding prior depreciation and amortization.

- Adjust for changes in working capital by accounting for changes in working capital accounts, such as accounts payable, accounts receivables, inventory, etc.

- Calculate net cash flow from your operating activities by combining adjusted net income with any changes in working capital.

- Cash Flow from Investing Activities:

- Identify investment-based cash transactions.

Calculate net cash flow from investing activities by subtracting all investment-based cash payments from all investment-based cash receipts.

- Cash Flow from Financing Activities:

- Identify financing-based cash transactions.

- Calculate net cash flow from financing activities by subtracting all financing-based cash payments from all financing-based cash receipts.

- Combine all sections by adding net cash flows from operating, investing, and financing activities to get an overview of all cash and cash equivalents changes over your specified period.

- Reconcile with beginning cash by adding changes to your beginning cash balance up to your ending cash balance. Ensure your reconciled cash balance matches your cash balance as reported in your balance sheet.

Download Now: Free cash flow statement template from Enerpize

How to Calculate Cash Flow Statements?

Calculating cash flow can be performed in two primary ways:

Direct Cash Flow Method:

Add up all cash payments and receipts. Or, you can use your beginning and ending balances of a range of your asset and liability accounts and examine net decreases or increases in your selected accounts.

Indirect Cash Flow Method:

Adjust net income by adding or subtracting non-cash transaction differences, as reported in your company’s asset and liability accounts (which should also appear in your balance sheet). Predictably enough, decreases or increases in all asset and liability accounts (such as accounts receivable and inventory) reflect non-cash calculation actions where deductions or additions are made, respectively, in each relevant account.

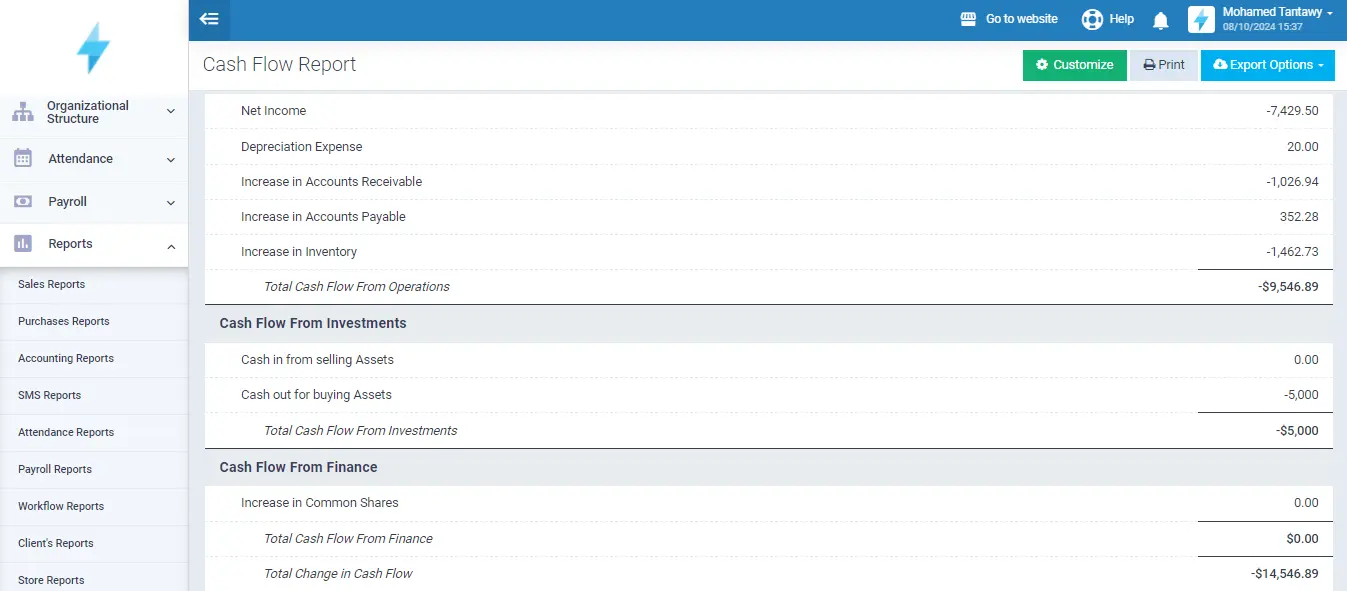

Cash Flow Statement Example

| Cash Flows from Operating Activities | Amount (USD) |

| Net Income | 80,000 |

| Adjustments for: | |

| - Depreciation | 15,000 |

| - Amortization | 7,000 |

| - Gain on sale of equipment | (3,000) |

| - Increase in accounts receivable | (6,000) |

| - Increase in inventory | (10,000) |

| - Increase in accounts payable | 5,000 |

| - Decrease in accrued expenses | (2,000) |

| Net Cash from Operating Activities | 86,000 |

| Cash Flows from Investing Activities | Amount (USD) |

| Purchase of equipment | (25,000) |

| Proceeds from sale of equipment | 12,000 |

| Purchase of investments | (8,000) |

| Net Cash Used in Investing Activities | (21,000) |

| Cash Flows from Financing Activities | Amount (USD) |

| Proceeds from issuance of common stock | 20,000 |

| Payment of dividends | (10,000) |

| Repayment of long-term debt | (15,000) |

| Net Cash Used in Financing Activities | (5,000) |

The above cash flow statement shows a positive net cash flow of USD 86,000 for 2023 generated from operating activities. This positive value generally reflects robust and active investment strategy and signals sound financial health for investors. A robust financial performance will likely positively impact a company’s valuation. One recent example is that of OpenAI, which, having been front and center of Generative AI innovation, is now valued at USD 157 bn.

The USD 10,000 end-of-year net cash flow underscores its comfortable cash cushion to invest more, pay off debts, or buffer against possible emerging contingencies.

Cash Flow Statement VS Financial Statements

The cash flow statement records all cash-based incoming or outgoing financial transactions. Importantly, cash flow statements record actual, not future, cash transactions. As such, cash flow statements represent an indispensable account of financial records for all transactions made exclusively in cash.

Still, necessary as are, cash flow statements alone are not enough to account for all financial activities, such as non-cash transactions. This is where a wide range of financial statements provide more detailed information.

How income statements and balance sheets compare to cash flow statements are discussed next.

Cash Flow Statement VS Income Statement

Cash flow and income statements provide detailed financial movements for financial planners, controllers, and investors. However, while cash flow statements account for cash-based flows, income statements are more holistic and include broader cash and non-cash (depreciation and amortization) information.

Moreover, while cash flow and income statements are prepared for a given period, they have some key differences. Specifically, while cash flow statements account for actual cash transactions, income statements account for cash and non-cash transactions and, importantly, for future positive or negative monetary values a given company has or owes over a specified reporting period.

This difference has broad implications for how financial planners, controllers, and accountants use each to achieve specific financial management purposes.

Cash flow statements can be used to monitor a company's short-term cash position and decide whether to invest in capital assets, for example.

Meanwhile, income statements are usually used to gain insights into a company’s overall financial health by understanding how, over a given period, cash and non-cash revenues and expenses perform to decide whether to expand in a new market, solicit funding, or invest in capital-intensive activities such as R&D.

Cash Flow Statement VS Balance Sheet

Cash flow statements and balance sheets compare pretty straightforwardly. Specifically, while cash flow statements record cash-based inflows and outflows, balance sheets provide a comprehensive record of a company’s overall assets and liabilities in whatever form: cash, non-cash, cash equivalents.

Similar to comparing cash flow statements and income statements, comparing cash flow and balance sheets enables financial planners, controllers, market analysts, and accountants to make informed decisions over the short and long terms.

Read Also: Comparative Balance Sheet: A Comprehensive Guide

Still, balance sheets go a step further from income statements.

Income statements allow financial controllers and analysts to plan for investments or divestments over a more extended period compared to cash flow statements and use more financial information (i.e., cash and non-cash transactions).

Meanwhile, balance sheets—recording all assets and liabilities at a given company—provide financial controllers and analysts with an even more holistic overview of how that company would perform based on financial data that go well beyond cash and non-cash transactions to include the company’s overall valuation. So, investors considering investing in a company always look at its balance sheet, where shareholder equity is recorded, not its cash flow statement or income statement.

How Can Enerpize Help You in Cash Flow Statement?

Enerpize is made for accounting. Cloud-based, agile, and automated, Enerpize is a go-to solution for many businesses who wish to manage accounting operations quickly, seamlessly, and compliantly.

At Enerpize, cash flow management is a given and an essential part of our online accounting software. Using Enerpize helps companies, big and small, manage cash flows and reports by:

- Adding cash inflows and outflows from any device anywhere.

- Posting billable cash-based invoices to customers.

- Generating detailed cash flow statements, including critical everyday cash transactions readily exportable to and mergeable with a range of financial statements.

- Facilitating cash flow auditing and reporting for tax compliance by automating report generation, updates, and notifications.

- Enabling companywide access to cash reserves to perform various business activities from collection to strategic investments.

- Maintaining accurate and readily accessible records of all cash transactions to prepare a range of financial statements, manually or automatically.

- Managing cash reserves maintained in multiple currencies per customer or jurisdiction to overcome currency volatilities, surges, or burns.

Enerpize is your gateway to a seamless cash flow management process and flawless, auto-adjusted cash flow statements.

Get a flavor of what Enerpize could offer you to make cash flow management and reporting a matter of process management, not a pain in identifying where your cash is going.

Final Thoughts

Cash flow statements report a company's cash-based inflows and outflows over a specific reporting period. The importance of cash flow management statements cannot be overemphasized. Used to manage cash flows and for auditing and financial purposes, cash flow statements are indispensable for getting a short-term view of a company’s cash position.

Cash flow statements are made up of four main components: (i) cash flow from operating activities, (ii) cash flow from investing activities, (iii) cash flow from financing activities, and (iv) non-cash activity disclosures.

Cash flow statements are created by:

- Collecting all required financial statements: income statement and balance sheet.

- Specifying reporting period on a monthly, quarterly, or annual basis.

- Selecting preparation method: direct or indirect.

- Preparing cash flow statement by:

- Calculating net cash flows from operating activities.

- Calculating net cash flows from investing activities.

- Calculating net cash flows from financing activities.

- Combining all net cash flows from all activities: operating, investing, and financing over your specified reporting period.

Reconciling with beginning cash by adding changes to your beginning cash balance up to your ending cash balance.

There are key differences between cash flow statements, income statements, and balance sheets.

Compared to income statements that include cash and non-cash records of expenses and revenue, cash flow statements are an account, a record, of all cash-based transactions only over a given reporting period.

Compared to balance sheets, which provide a comprehensive account of all a company's assets and liabilities, cash flow statements are limited to cash-based transactions only and do not include cash equivalents (i.e., assets that can be converted into cash).

As a business owner, executive manager, or entrepreneur, managing your cash right is indispensable so you can assess your cash position and, importantly, plan short-term for possible necessary capital or non-capital investments.

Many cash flow management software is around. A few provide some edge. Only exceptional, customer-centered applications stand out to generate cash flow statements that land you just as outstanding financial performance.

Cash flow statement is easy with Enerpize.

Try our accounting module to create financial statements automatically.

Cash flow statement is easy with Enerpize.

Try our accounting module to create financial statements automatically.