Author : Haya Assem

Reviewed By : Enerpize Team

How To Do Closing Entries: Explanation with Examples

In the double-entry system, closing entries are essential for resetting temporary accounts like revenues, expenses, and withdrawals at the end of each accounting period. This process transfers balances to permanent accounts such as retained earnings or capital, ensuring accurate records and preparing the books for the next period. Whether done manually or using software, closing entries help maintain clear and compliant financial reporting.

Key Takeaways

- Closing entries transfer temporary account balances to permanent accounts: This process resets revenue, expense, and withdrawal accounts to zero and updates the capital or retained earnings account for the new period.

- The process involves four main steps: Closing revenue accounts, expense accounts, the income summary account, and finally, dividends or drawings, ensuring that all temporary accounts are cleared.

- Proper closing ensures accurate financial statements: By finalizing the books, businesses can generate reliable financial reports and maintain consistency in their records for future periods.

What Are Closing Entries?

Closing entries are journal entries made at the end of an accounting period to transfer the balances of temporary accounts (like revenue, expenses, and dividends) to permanent accounts (such as retained earnings). This process resets the temporary accounts to zero for the next period.

What Is The Purpose Of Closing Entries?

Closing entries are essential for maintaining accurate financial records at the end of an accounting period. Their main purpose is to reset temporary accounts and update permanent accounts, ensuring that the financial information accurately reflects the company's performance and position. Below are the key purposes of closing entries:

Reset Temporary Accounts

Closing entries clear the balances in temporary accounts such as revenues, expenses, and dividends, resetting them to zero. This process prepares these accounts for the next accounting period, ensuring that they track only the financial activity of the upcoming period.

Transfer Net Income or Loss

Closing entries transfer the net income or loss from the accounting period to the retained earnings account. This step ensures that the income or loss is accurately reflected in the company’s permanent accounts, which track long-term financial performance.

Update Retained Earnings

By transferring the net income (or loss) and any dividends paid to the retained earnings account, closing entries keep the retained earnings balance up to date. This ensures that the company’s accumulated profits or losses are accurately reported in the financial statements.

Read Also: How to Calculate Retained Earnings on A Balance Sheet

Temporary Accounts Vs Permanent Accounts

Accounts are classified into two categories: temporary accounts and permanent accounts. These classifications help distinguish between accounts that are reset at the end of an accounting period and those that carry forward their balances to the next period. For proper financial record-keeping, here is the difference between each type:

Temporary Accounts

Temporary accounts are used to track financial transactions for a specific period, and their balances are reset to zero at the end of the accounting period. These accounts include:

- Revenue Accounts: Track income earned during the period (e.g., sales revenue).

- Expense Accounts: Track costs incurred during the period (e.g., rent, salaries, utilities).

- Dividend Accounts: Track dividends paid to shareholders during the period.

Once the period ends, the balances in temporary accounts are closed to permanent accounts, such as retained earnings.

Permanent Accounts

Permanent accounts, also known as real accounts, carry their balances forward from one period to the next. They are not reset at the end of the period and reflect the ongoing financial position of the company. These accounts include:

- Assets: Represent what the company owns (e.g., cash, inventory, property).

- Liabilities: Represent what the company owes (e.g., accounts payable, loans).

- Equity: Represents the owner's interest in the company, including retained earnings, common stock, etc.

The balances in permanent accounts accumulate over time and are carried forward to future periods, reflecting the company’s long-term financial status.

Read Also: Adjusting Journal Entries: Definition, Types, and Examples

Closing Entries Examples

Closing entries are recorded at the end of an accounting period to move the balances from temporary accounts to permanent accounts. This process prepares the company's books for the next period by resetting revenues, expenses, and dividends to zero. Here are common closing journal entries examples:

Closing Revenue Accounts

At the end of the accounting period, all revenue account balances must be closed out to begin the new period with a zero balance. This is done by transferring the total revenue earned during the period into the Income Summary account, which temporarily holds all income before calculating net results.

Example:

The company earned $50,000 in revenue during the year.

Journal Entry:

| Date | Account | Debit | Credit |

| 31/12/2024 | Reveue | $50,000 | |

| Income Summary | $50,000 |

Closing Expense Accounts

To prepare for a new accounting period, all individual expense accounts (such as rent, salaries, utilities, etc.) must be closed. This is done by transferring their balances to the Income Summary account. Doing so resets the expense accounts to zero and helps determine the period’s net income or net loss.

Example:

The total expenses for the year are $30,000.

Journal Entry:

| Date | Account | Debit | Credit |

| 31/12/2024 | Income Summary | $30,000 | |

| Expenses | $30,000 |

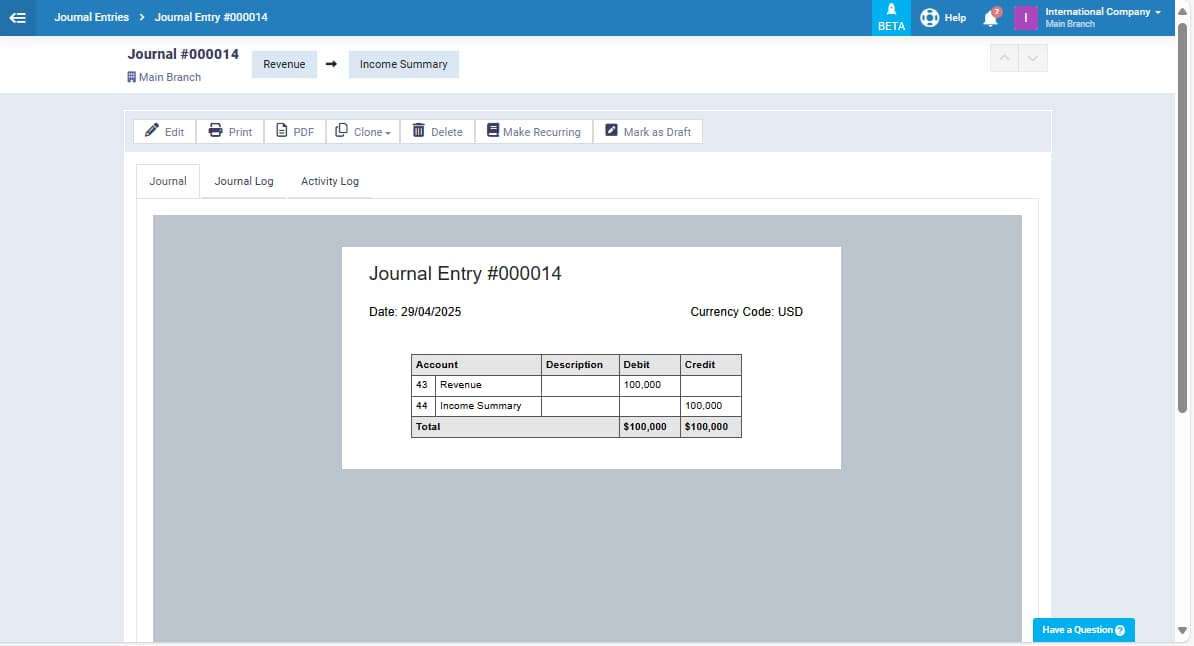

Closing the Income Summary Account

After transferring all revenues and expenses to the Income Summary account, the remaining balance shows the company’s net income or net loss for the period. This final balance needs to be moved to the Retained Earnings account to update the company’s equity and reflect the overall financial result of the period.

Example:

The company earned a net income of $20,000, calculated as $50,000 in revenue minus $30,000 in expenses.

| Date | Account | Debit | Credit |

| 31/12/2024 | Income Summary | $20,000 | |

| Retained Earnings | $20,000 |

Read Also: Prepaid Expense Journal Entries: Examples & How to Record

How To Prepare Closing Entries?

At the end of an accounting period, closing entries are made to transfer the balances of temporary accounts—revenues, expenses, and dividends or withdrawals—into permanent accounts. This process resets the temporary accounts to zero and prepares the books for the next period.

1- Close Revenue Accounts

Revenue accounts, like Sales Revenue, are closed by transferring their balances to the Income Summary account. This is done by debiting the revenue account and crediting the Income Summary, resetting the revenue accounts to zero.

Journal Entry Example:

| Account | Debit | Credit |

| Sales Revenue | $10,000 | |

| Income Summary | $10,000 |

2- Close Expense Accounts

Expense accounts are closed by transferring their balances to the Income Summary account. You do this by debiting the Income Summary and crediting each expense account, which resets the expense balances to zero.

Journal Entry Example:

| Account | Debit | Credit |

| Income Summary | $5,000 | |

| Rent Expense | $2,000 | |

| Salary Expense | $3,000 |

3- Close the Income Summary Account

The Income Summary account, which reflects the net income or loss, is then closed to Retained Earnings (or Capital). This is done by debiting the Income Summary and crediting Retained Earnings if there’s net income, or vice versa for a net loss.

Journal Entry (Net Income Example):

| Account | Debit | Credit |

| Income Summary | $5,000 | |

| Retained Earnings | $5,000 |

4- Close Dividends or Withdrawals

If dividends or owners’ withdrawals have been made, their balance is transferred to Retained Earnings (or Capital). This resets the Dividends or Withdrawals account to zero.

Journal Entry:

| Account | Debit | Credit |

| Retained Earnings | $1,000 | |

| Dividends | $1,000 |

Automate Closing Entries With Enerpize

Enerpize is an online accounting software designed to streamline financial tasks for small and medium-sized businesses. It provides real-time access to your financial data and integrates powerful tools for accounting, inventory, payroll, and more, all within a secure and user-friendly platform.

One of its key features is the ability to automate accounting closing entries, eliminating the need for manual journal entries at the end of each accounting period. With just a few clicks, Enerpize accurately transfers balances from revenue and expense accounts to the income summary and updates retained earnings or capital. This not only saves time but also ensures accuracy and consistency in your financial records, helping you close your books confidently.

FAQs

How To Do Closing Entries?

To do closing journal entries, start by closing all revenue accounts into an Income Summary account. Then, close all expense accounts into the same Income Summary. After that, transfer the resulting net income or loss from the Income Summary to Retained Earnings (or Capital for sole proprietorships). Finally, close any Dividends or Owner’s Drawings accounts to Retained Earnings to reset all temporary accounts for the new period.

Read Also: How to Do Journal Entries

What Are The 4 Closing Entries?

The four standard closing entries are:

- Close revenue accounts to Income Summary.

- Close expense accounts to Income Summary.

- Close the Income Summary to Retained Earnings (or Capital).

- Close Dividends or Withdrawals to Retained Earnings (or Capital).

How To Record Closing Entries?

Closing entries are recorded as journal entries in the general ledger. Each temporary account (revenues, expenses, dividends/drawings) is reduced to zero by transferring its balance to the appropriate permanent account using debit and credit entries.

Recording closing entries is easy with Enerpize.

Try our accounting module to do closing entries with a few clicks.

Recording closing entries is easy with Enerpize.

Try our accounting module to do closing entries with a few clicks.