Create and send online quotations and invoices, track sales, monitor staff performance, and sell & sync all your products via our POS and more.

Posted on 18 August 2024

Author : Haya Assem

Reviewed By : Enerpize Team

Author : Haya Assem

Reviewed By : Enerpize Team

Adjusting Journal Entries: Definition, Types, and Examples

Journal entries are the main pillar of accurate accounting records, they play a critical role in tracking a business's financial position. Each entry records a financial transaction, ensuring all activities are properly documented and accounted for. According to the recurring nature of this process, with companies generating numerous journal entries daily, there is always the potential for errors or the need to account for transactions that still need to be recorded. This is where adjusting entries becomes essential.

Adjusting entries are crucial for correcting inaccuracies, accounting for unrecorded transactions, and ensuring that all income and expenses are accurately reflected in the appropriate accounting period. By making these adjustments, businesses can uphold the integrity of their financial records and produce reliable financial statements that truly represent their financial position.

What are Adjusting Journal Entries?

Adjusting entries are essential modifications made to the accounting records at the end of an accounting period. These entries are required to ensure that all income and expenses are accurately recorded in the correct period, reflecting the accurate financial position of the business.

Adjusting entries often involve accrued revenues, accrued expenses, deferred revenues, deferred expenses, and depreciation. By making these adjustments, businesses may guarantee that their financial statements meet accounting standards and accurately reflect their financial performance and condition.

Read Also: How to Track Business Expenses?

The Main purpose of Adjusting Entries

The main purpose of adjusting entries is to ensure that a company's financial records accurately reflect its financial position at the end of an accounting period. Adjusting entries are used to account for revenues that have been earned but not yet recorded, expenses that have been incurred but not yet paid or recorded, and other financial activities that may not be captured by regular journal entries.

By making these adjustments, businesses can ensure that their financial statements provide a true and fair view of their financial performance, comply with accounting standards, and allow for informed decision-making.

Importance of Adjusting Entries

Adjusting entries are an essential aspect of the accounting process, ensuring that a business's financial records are both accurate and complete. By making these necessary adjustments at the end of an accounting period, businesses can maintain the integrity of their financial data. The following points highlight the key importance of adjusting entries in achieving reliable and precise financial reporting:

Maintain Accurate Financial Records

Adjusting entries are crucial for maintaining precise financial records by ensuring that all financial transactions are accurately recorded within the correct accounting period. This helps prevent discrepancies and ensures that journal entries reflect the true financial position of the business.

Tracking Payables and Receivables Efficiently

These entries also aid in accurately tracking payables and receivables, ensuring that all payments owed to and by the company are recorded correctly. This is essential for managing cash flow and ensuring that financial obligations are met on time.

Accurately Record Expenses

By adjusting entries, businesses can ensure that all expenses are accurately recorded in the correct period. This is critical for aligning costs with revenues, leading to more accurate financial reporting.

Correct Inaccuracies in Entries

Adjusting entries allow businesses to rectify errors in previous entries, such as omissions or misstatements. This ensures that any inaccuracies are addressed and the financial records remain reliable.

Read Also: Transposition Error: Definition, Example, And How To Correct

Ensure Financial Statements Accuracy

The accuracy of financial statements relies heavily on the use of adjusting entries. These adjustments ensure that all financial activities are properly recorded, providing a true and accurate view of the company's financial performance and state.

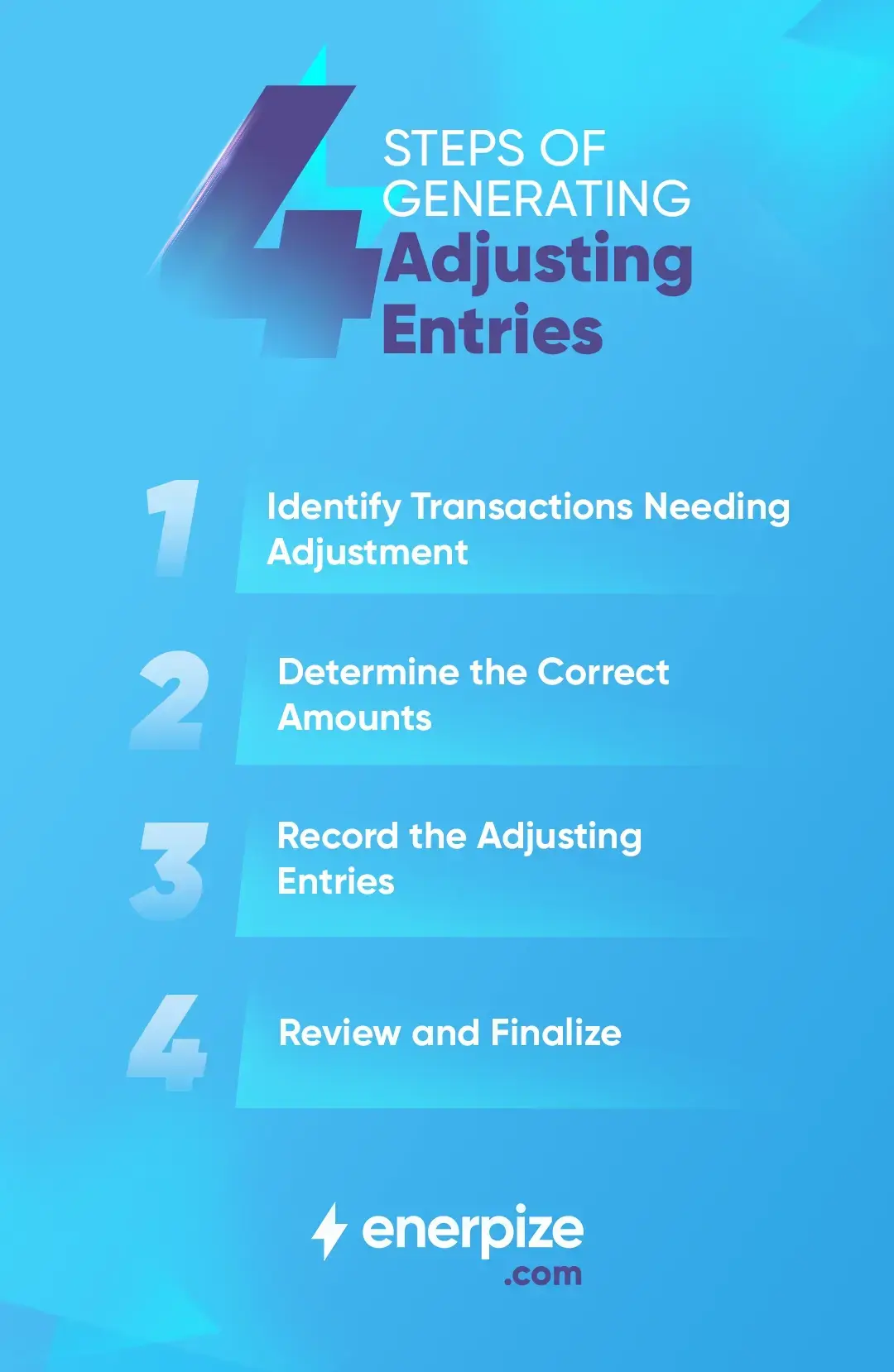

How Does Adjusting Journal Entries Work?

Adjusting journal entries work by making necessary modifications to a company's financial records at the end of an accounting period. These entries ensure that all revenues and expenses are recorded in the correct period, reflecting the true financial position of the business. The process of generating adjusting entries works as follows:

Identify Transactions Needing Adjustment

The first step is to identify transactions that have occurred but have not yet been recorded. This includes accrued revenues, accrued expenses, prepaid expenses, and depreciation.

Determine the Correct Amounts

For each identified transaction, determine the accurate amount that needs to be recorded. This might involve calculating interest earned, expenses incurred but not yet paid, or the amount of depreciation to be applied.

Record the Adjusting Entries

Once the amounts are determined, adjusting journal entries are recorded in the accounting system. These entries typically involve debits and credits to the appropriate accounts, ensuring that the balance sheet and income statement reflect the correct figures.

Review and Finalize

After recording the adjusting entries, they are reviewed to confirm their accuracy and ensure all necessary adjustments have been made. Once verified, the accounting period is closed, and the financial statements are prepared, providing a clear and accurate representation of the company's financial position and performance.

Main Types of Adjusting Journal Entries

Adjusting entries are categorized based on the nature of the transactions they address. These entries are essential for ensuring that all financial activities are accurately reflected in the financial statements at the end of an accounting period. The main types of adjusting entries are:

Accruals

Accruals record revenues and expenses that have been earned or incurred but not yet received or paid, ensuring financial statements reflect the actual activities within the period.

Accrued Expenses

These are expenses that have been incurred but not yet paid or recorded in the books. For example, wages earned by employees but not yet paid by the end of the accounting period need to be recorded as accrued expenses to reflect the true liability.

Accrued Revenues

Accrued revenues represent income that has been earned but not yet received or recorded. This might include services provided to a customer that have not yet been billed. Adjusting entries for accrued revenues ensure that income is recognized in the period it is earned, regardless of when payment is received.

Deferrals

Deferrals involve payments or receipts made in advance, with recognition delayed until the appropriate period, aligning costs and income with the correct accounting period.

Deferred Expenses

Also known as prepaid expenses, these are payments made in advance for goods or services to be received in the future. For example, if rent is paid for a year in advance, the expense is initially recorded as an asset and then gradually expensed over the period it relates to.

Learn more about prepaid expense journal entries, and their importance and examples.

Deferred Revenues

Deferred revenues, or unearned revenues, are payments received before delivering goods or services. For instance, a business might receive payment for a subscription service before the service is provided. Adjusting entries for deferred revenues ensure that income is only recognized when it is earned.

Non-Cash Adjustments

These entries involve allocating the cost of long-term assets over their useful lives (depreciation and amortization) or setting aside funds for future liabilities (provisions). Adjustments for estimates are made to account for potential losses or future expenses that cannot be precisely measured. These non-cash adjustments ensure the financial statements accurately reflect the usage, wear, or expected obligations associated with the assets and liabilities.

Adjusting Journal Entries Examples

Adjusting entries can be categorized into accruals, deferrals, and non-cash items as explained previously, each addressing specific transactions requiring adjustment to match revenues and expenses with the correct period properly. Below are examples of each type of adjusting entry.

Accrued Revenues

A consulting firm provided $5,000 worth of services in December but hasn't invoiced the client yet. Although no invoice has been sent, the firm must recognize this income for December to accurately reflect its earnings.

Adjusting Entry:

- Debit: Accounts Receivable $5,000

- Reflects the amount owed by the client for services provided.

- Credit: Service Revenue $5,000

- Recognizes the revenue earned during December, even though payment hasn't been received.

Deferral Expenses:

A company prepaid $1,800 for six months of rent starting in July. By September 30, three months' worth of rent has expired.

Adjusting Entry:

- Debit: Rent Expense $900

- Recognizes the expense for the expired portion of the rent.

- Credit: Prepaid Rent $900

- Reduces the Prepaid Rent account to reflect the used portion.

Read Also: Lease Accounting Journal Entries

Non-Cash Entries

These entries adjust accounts that do not involve cash transactions but are necessary for accurate financial reporting.

Depreciation

A company purchased machinery for $12,000 with a five-year useful life. At year-end, the company needs to record $2,400 of depreciation expense to reflect the machinery's usage.

Adjusting Entry:

- Debit: Depreciation Expense $2,400

- Credit: Accumulated Depreciation $2,400

This entry allocates the machinery's cost over its useful life, showing its reduced value on the balance sheet.

You can find more examples here.

Read Also:

Payroll Journal Entries in Accounting: Definition, Types, & Examples

Intercompany Transactions Journal Entries: Importance & Examples

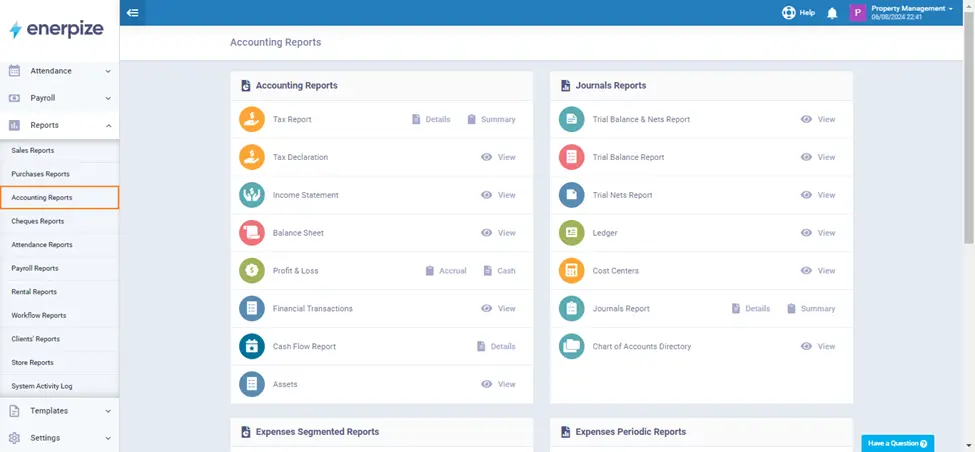

How Can Enerpize Help You in Adjusting Journal Entries?

Enerpize automates the creation of adjusting entries for accruals, deferrals, depreciation, and other necessary adjustments. This minimizes manual work and reduces the risk of errors. The system provides real-time access to financial data, making it easier to identify when adjusting entries are needed. This ensures that your financial statements reflect the most accurate and up-to-date information.

Enerpize's online accounting software allows you to set up recurring adjusting entries, such as monthly prepaid expenses or annual depreciation. It tracks these schedules, ensuring that entries are made consistently and on time. It also provides detailed reports and audit trails for all adjusting entries. This transparency is essential for reviewing the accuracy of your adjustments, preparing financial statements, and ensuring compliance with accounting standards.

The software is designed with user-friendly interfaces that guide users through the process of making adjusting entries, allowing even those with limited accounting experience to manage their adjustments accurately and with ease.

Journal Entries Adjusting is easy with Enerpize.

Try our accounting module to manage your entries.

Journal Entries Adjusting is easy with Enerpize.

Try our accounting module to manage your entries.