Author : Haya Assem

Reviewed By : Enerpize Team

Steps to Make Journal Entries: A Comprehensive Guide

Journal entries are fundamental for accurate financial reporting, documenting every transaction to ensure proper record-keeping. This guide covers the importance of journal entries, including their role in accuracy, legal compliance, financial analysis, audit trails, decision-making, and error prevention. It also provides step-by-step instructions for creating various types of journal entries, such as general, adjusting, and payroll entries, along with practical examples to illustrate their application.

Key Takeaways

- Journal entries are essential for recording every financial transaction, ensuring accuracy, legal compliance, and organized bookkeeping.

- They form the basis of financial analysis, helping you track income, expenses, assets, and liabilities, which supports reliable reporting and business insight.

- Creating a journal entry involves identifying the transaction, determining affected accounts, applying double-entry rules, and recording details with a clear explanation.

- Types of journal entries include general, adjusting, closing, and payroll entries, each serving a unique purpose to keep your financial records accurate and up-to-date.

- Adjusting entries ensure accuracy at the end of a period by matching revenues and expenses to the correct accounting timeframe under accrual accounting.

- Payroll entries capture employee compensation, taxes, and benefits accurately, dividing them into appropriate expense and liability accounts.

- To maintain integrity, use posting references, audit trails, restricted access, and period closures to prevent unauthorized changes and support clean audit trails.

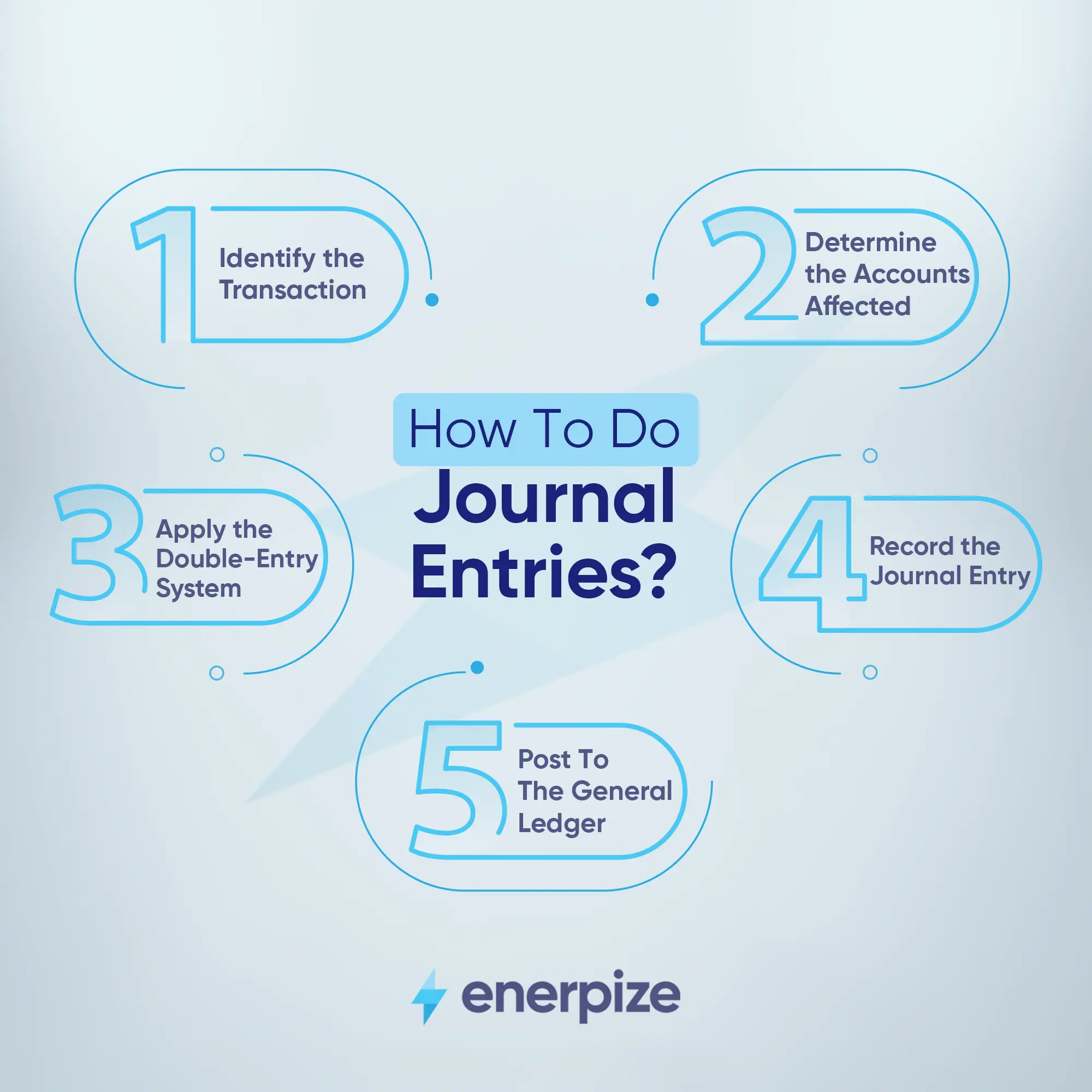

How to Do Journal Entries in Accounting?

Creating journal entries in accounting involves following a systematic process to record financial transactions. Here are the steps:

1- Identify the Transaction

Identify whether it’s related to sales, purchases, expenses, or any other type of financial activity. Categorize the transaction is it related to assets, liabilities, equity, income, or expenses?

Read Also: Prepaid Expense Journal Entries: Importance, Examples & How to Record?

2- Determine the Accounts Affected

Every transaction affects at least two accounts. One account will be debited, while the other will be credited.

3- Apply the Double-Entry System

Debit and credit are the foundation of accounting entries:

- Debit: Increases assets or expenses and decreases liabilities or equity.

- Credit: Increases liabilities, equity, or income and decreases assets or expenses.

Read Also: Single Entry VS Double Entry Accounting: A Comprehensive Guide

Note: Ensure the total amount of debits equals the total amount of credits.

4- Record the Journal Entry

Create the entry in the journal by listing:

- The date of the transaction.

- The accounts involved: Debited accounts are listed first, and credited accounts are indented and listed next.

- The amount for each debit and credit.

- A brief description of the transaction for reference.

5- Post to the General Ledger

After the entry is recorded in the journal, post it to the respective accounts in the general ledger. Each account will have its own ledger where debits and credits are recorded.

Read Also: Journal Entries For Sales: Examples And How To Record

Examples of Doing Journal Entries for Different Types

How to do Accounting Journal Entries?

Let’s assume that a company purchases office supplies worth $500 on September 10, 2024, and pays in cash.

Journal Entry

| Date | Account | Debit | Credit |

| September 10, 2024 | Office Supplies | 500 | |

| Cash | 500 |

Debit "Office Supplies": The supplies are an asset, and the company has more of them after the purchase. Therefore, you debit the account for $500.

Credit "Cash": Since cash was used to make the purchase, the cash account decreases, so you credit it for $500.

How to do General Journal Entries?

To prepare general journal entries, you document a business’s financial transactions in the general journal, which is the primary book of entry. Each entry records both a debit and a credit, adhering to the double-entry accounting system.

These entries capture all types of transactions—purchases, sales, expenses, and more—ensuring the accounting equation (Assets = Liabilities + Equity) remains balanced. By preparing general journal entries, businesses maintain accurate financial records and track the flow of money, which is essential for financial reporting and analysis.

Example

On March 1, 2024, your business purchased office furniture for $1,500 in cash.

Office Furniture is debited because it’s an asset that increases.

Cash is credited because it’s an asset that decreases.

| Date | Account | Debit | Credit |

| 01/03/2023 | Office Furniture | 1,500 | |

| Cash | 1,500 |

How to do Closing Journal Entries?

Closing journal entries are made at the end of an accounting period to transfer temporary account balances (like revenues, expenses, and dividends) to permanent accounts (such as retained earnings), resetting the temporary accounts back to zero for the following accounting period.

Example

Let's say a company has $5,000 in revenues and $3,000 in expenses at the end of the period.

Close revenue accounts

- Debit Revenue: $5,000

- Credit Retained Earnings: $5,000

Close expense accounts

- Debit Retained Earnings: $3,000

- Expenses: $3,000

| Date | Account | Debit | Credit |

| 31/12/2024 | Revenue | 5,000 | |

| Retained Earnings | 5,000 | ||

| Retained Earnings | 3,000 | ||

| Expenses | 3,000 |

How to do Adjusting Journal Entries?

Adjusting journal entries are essential for ensuring accurate financial reporting and involve updating account balances at the end of an accounting period. These entries are necessary to reflect revenues and expenses in the period they occur, following the accrual basis of accounting.

If you need to know how to do adjusting journal entries, it typically involves recording accrued revenues, accrued expenses, deferred revenues, and deferred expenses to align financial statements with the correct period.

Example

Assume a company has earned $1,000 in interest revenue that has not yet been recorded by the end of the period.

Adjust for accrued interest revenue

- Debit: Interest Receivable: $1,000

- Credit: Interest Revenue: $1,000

| Date | Account | Debit | Credit |

| 24/11/2024 | Interest Receivable | 1,000 | |

| Interest Revenue | 1,000 |

How to do Payroll Journal Entries?

Payroll journal entries are crucial for accurately recording employee wages, taxes, and benefits in financial records. To understand how to do payroll journal entries, you need to record the gross wages expense, as well as any withholdings and employer liabilities.

This includes debiting the wages expense account and crediting accounts for taxes payable, benefits payable, and any fees associated with payroll processing. This ensures that payroll expenses and related liabilities are accurately reflected in your financial statements.

Example

Assume a company pays $3,000 in wages, with $500 in taxes withheld and $100 in employee benefits. The company also incurs a $50 payroll processing fee.

Record wages expense:

- Debit Wages Expense: $3,000

- Credit Cash/Bank: $2,450 (Net payment to employees after withholdings and benefits)

- Credit Payroll Taxes Payable: $500

- Credit Employee Benefits Payable: $100

- Credit Payroll Processing Fee Expense: $50

| Date | Account | Debit | Credit |

| 31/12/2024 | Wages Expenses | 5,000 | |

| Cash/Bank | 2,450 | ||

| Payroll Taxes Payable | 500 | ||

| Employee Benefits Payable | 100 | ||

| Payroll Processing Fee Expense | 50 |

Read Also:

Journal Entries for Bank Reconciliation: A Comprehensive Guide

Intercompany Transactions Journal Entries: Importance & Examples

Lease Accounting Journal Entries: Types, Standards & Calculating Steps

Importance of Recording Journal Entries

Accuracy and Organization:

Journal entries ensure that all financial transactions are accurately recorded. They provide a detailed log of every transaction, allowing businesses to track their financial activity efficiently.

Legal Compliance:

Maintaining proper journal entries helps businesses comply with legal and regulatory requirements. Many tax laws and financial regulations require businesses to keep accurate records of their financial transactions.

Financial Analysis:

Journal entries allow for detailed financial analysis. By organizing transactions, helps businesses track income, expenses, assets, and liabilities, which is essential for creating financial statements like the income statement and balance sheet.

Audit Trail:

Each journal entry serves as an audit trail. If an audit or financial review is required, journal entries provide clear documentation of every transaction, making it easier to verify the accuracy of financial statements.

Decision-Making:

With accurate journal entries, businesses can generate reliable financial reports that inform strategic decision-making, such as budgeting, forecasting, and evaluating profitability.

Prevention of Errors:

Recording each transaction with proper journal entries helps prevent errors and fraud, as they create a detailed and systematic record that can be reviewed and reconciled regularly.

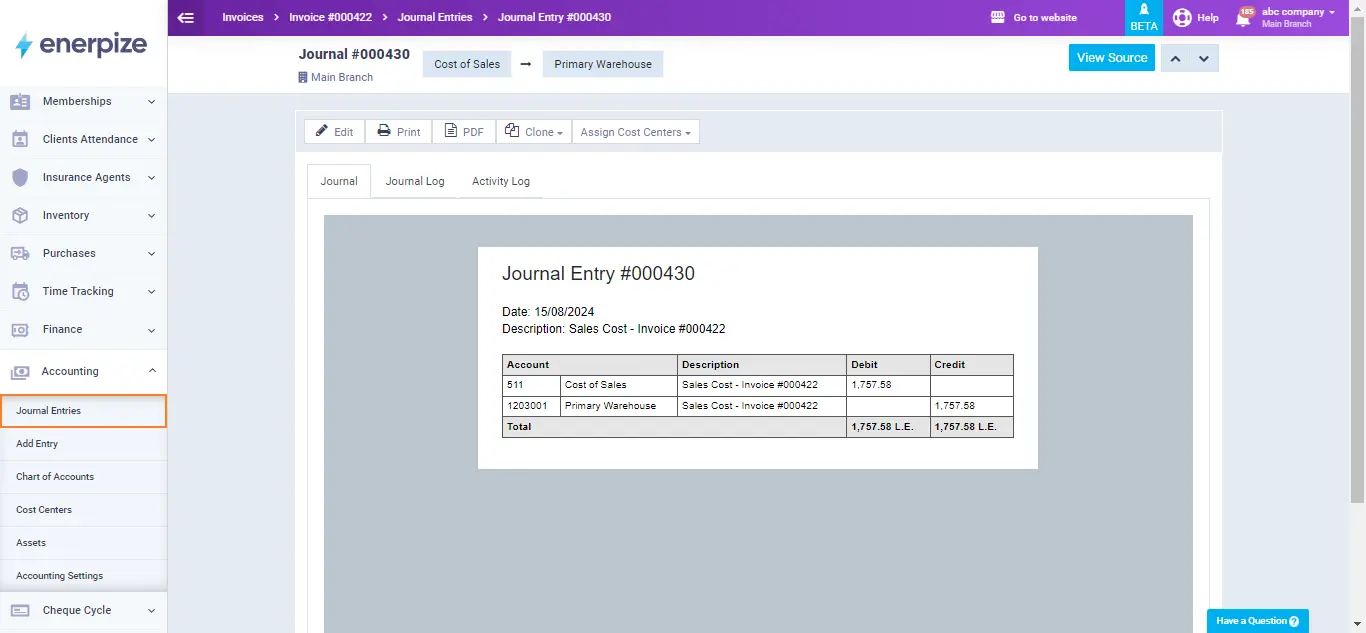

Enerpize: The Easiest Way To Do Journal Entries

Enerpize online accounting software streamlines the process of recording journal entries, making it easier for users to maintain accurate financial records. With its intuitive interface, Enerpize allows you to quickly input journal entries and automatically ensures that debits and credits are balanced. The software provides journal entries automation prevents common errors and maintains data integrity.

Additionally, Enerpize provides comprehensive posting references and audit trails, enabling efficient tracking and verification of each entry. This improves accuracy and enhances efficiency, as you can effortlessly generate reports and reconcile accounts. By automating and simplifying the journal entry process, Enerpize helps you manage your accounting tasks with greater confidence and precision.

FAQ About Preparing Journal Entries

Which 3 statements are true about recording journal entries?

- Journal entries must follow the double-entry accounting system, meaning each entry must have at least one debit and one credit, and the total debits must equal the total credits to keep the accounting equation balanced.

- Journal entries provide a systematic record of all financial transactions, which helps in tracking and verifying the details of each transaction for accurate financial reporting and auditing.

- Journal entries must be accompanied by supporting documentation (such as invoices, receipts, or contracts) to validate the transaction and provide a clear audit trail for future reference.

How can you prevent the creation or modification of journal entries to a specific accounting date?

1- Set Up Period Closures:

Use your accounting software to close the accounting period or fiscal year. Once a period is closed, no further changes can be made to journal entries within that period. This prevents accidental modifications and ensures that financial reports are based on finalized data.

2- Implement Access Controls:

Restrict access to journal entry functions based on user roles and permissions. Ensure that only authorized personnel can create or modify entries. Set permissions to prevent changes to periods that should be locked.

3- Enable Audit Trails:

Utilize features in your accounting software that provide audit trails. This tracks any attempts to create or modify journal entries and ensures accountability. Monitoring these logs can help identify and prevent unauthorized changes.

Why are posting references entered in the journal when entries are posted to the ledger accounts?

- Track and Verify Transactions: Posting references link journal entries to their corresponding ledger accounts. This helps in tracking where each entry has been posted, making it easier to verify that transactions have been recorded correctly and completely.

- Facilitate Cross-Referencing: They provide a cross-reference between the journal and the ledger. This allows accountants to trace the flow of transactions from the original journal entry to the ledger accounts, and vice versa, ensuring that records are accurate and consistent.

Improve Accuracy and Efficiency: By having a reference system, accountants can quickly locate and review entries in both the journal and the ledger, reducing the likelihood of errors and speeding up the reconciliation process.

Read Also: General Ledger VS Subledger: A Comprehensive Guide

Journal entries are easy with Enerpize.

Try our accounting module to handle your entries.

Journal entries are easy with Enerpize.

Try our accounting module to handle your entries.