Create and send online quotations and invoices, track sales, monitor staff performance, and sell & sync all your products via our POS and more.

Posted on 2 February 2025

Author : Haya Assem

Reviewed By : Enerpize Team

Author : Haya Assem

Reviewed By : Enerpize Team

Direct VS Indirect Cash Flow: A Comprehensive Guide

Table of contents:

- What Is The Cash Flow Direct Method?

- Direct Method Cash Flow Example

- Pros And Cons Of Direct Cash Flow

- What Is The Cash Flow Indirect Method?

- Indirect Cash Flow Example

- Pros and Cons of Indirect Cash Flow

- Direct Vs Indirect Cash Flow

- Direct Vs Indirect Methods And Cash Flow Statement

- Direct Vs Indirect Cash Flow Which Is Better?

- Streamline Cash Flow Management with Enerpize

Managing cash flow is essential for any business’s success, but understanding how cash moves in and out can be complex. This comprehensive guide explores the two main methods of preparing a cash flow statement: direct vs indirect method cash flow. We’ll break down how each method works, its advantages and disadvantages, and help you determine which is best suited for your financial analysis or reporting needs.

What Is The Cash Flow Direct Method?

The direct method of preparing a cash flow statement shows cash inflows and outflows directly by listing specific cash transactions. It’s a straightforward way of presenting how cash is received and spent during a period, without adjusting for non-cash transactions.

Under the direct method, the cash flow statement will typically include:

- Cash received from customers: Cash collected from sales of goods or services.

- Cash paid to suppliers and employees: Outflows related to operating expenses like paying for inventory, wages, etc.

- Cash paid for operating expenses: This can include rent, utilities, and other costs necessary for running the business.

- Other direct cash payments: Any other cash-related transactions.

Direct Method Cash Flow Example

In the direct method, the operating activities section lists actual cash receipts and cash payments. Here’s an example:

Operating Activities Section (Direct Method):

- Cash Receipts from Customers: $500,000

(It's the direct cash inflow from operations.) - Cash Paid to Suppliers: $(200,000)

(The cash outflow the company paid to suppliers for materials or inventory purchased during the period.) - Cash Paid to Employees: $(100,000)

(This is the total cash outflow paid to employees in the form of salaries, wages, and benefits.) - Interest Paid: $(10,000)

(The cash outflow related to the company's financing activities (interest on loans, credit lines, etc.). - Income Taxes Paid: $(30,000)

(The cash outflow for income taxes the company paid during the period.)

Net Cash Provided by Operating Activities: $160,000

This is the total cash flow from operating activities. It is calculated by adding all the cash inflows and subtracting all the cash outflows:

Cash Inflows: $500,000

Cash Outflows: $(200,000), $(100,000), $(10,000), $(30,000)

$500,000 - $200,000 - $100,000 - $10,000 - $30,000 = $160,000. This is the net amount of cash generated from the company’s core operations.

Read Also: Pro Forma Cash Flow Statement: A Comprehensive Guide

Pros And Cons Of Direct Cash Flow

While the direct cash flow method provides detailed insights into a company's liquidity and financial health, it also comes with challenges in terms of preparation and consistency with other financial statements.

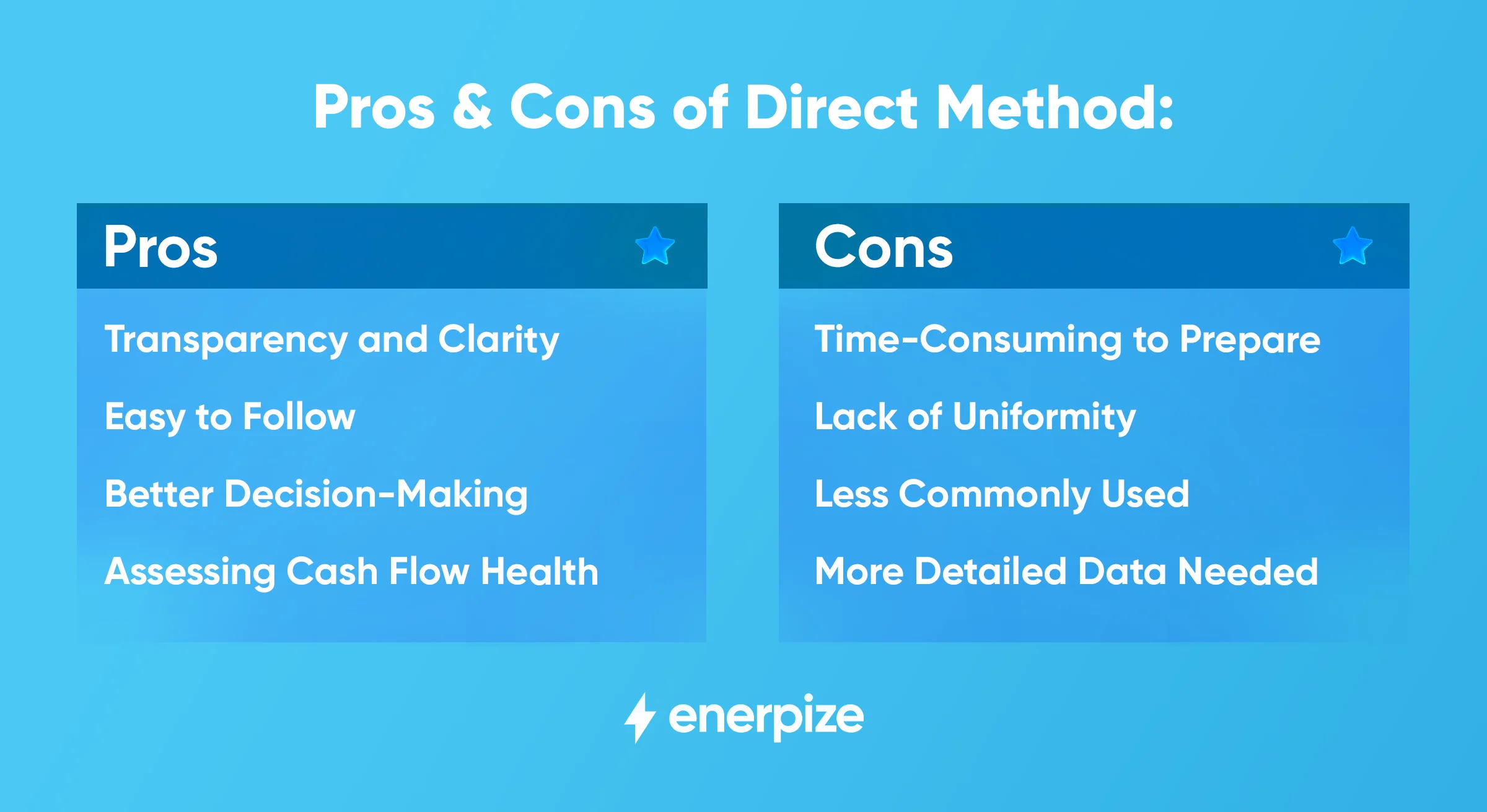

Direct Method Pros

Transparency and Clarity

The direct method provides a clear picture of actual cash inflows and outflows. It shows specific cash transactions, making it easier to understand the business’s cash position.

Easy to Follow

Since it directly lists cash received from customers and cash paid to suppliers and employees, it’s more straightforward for users (like investors or management) to track how cash is being generated and spent.

Better Decision-Making

By seeing how cash flows in and out of the business, management can make more informed decisions regarding liquidity, operations, and investments.

Better for Assessing Cash Flow Health

Because it focuses solely on cash inflows and outflows, it can give a more accurate representation of a company's ability to generate cash and meet short-term obligations.

Direct Method Cons

Time-Consuming to Prepare

The direct method requires detailed tracking of every cash transaction, which can be labor-intensive. Businesses with a high volume of transactions may find this challenging.

Lack of Uniformity

While the direct method offers clarity, it doesn’t always match the structure of other financial statements (like the income statement), which can make it harder to compare with industry peers using the indirect method.

Less Commonly Used

Most companies (especially larger ones) use the indirect method because it’s easier to prepare, relying on the already available data from the income statement. This makes the direct method less common and might make it harder to find resources or software that easily supports it.

More Detailed Data Needed

Companies need to have good systems in place to track every cash transaction, which can be a challenge, especially for businesses that use accrual accounting where revenues and expenses aren’t always aligned with actual cash flows.

What Is The Cash Flow Indirect Method?

The indirect method of preparing a cash flow statement starts with net income (or net loss) from the income statement and then adjusts for changes in non-cash items and working capital. Essentially, it shows how net income from operations is converted into cash flow by adding back non-cash expenses and adjusting for changes in assets and liabilities.

- Start with net income: The statement begins with the net income figure from the income statement.

- Adjust for non-cash items: This includes adding things like depreciation, amortization, and other expenses that didn’t involve actual cash outflow.

- Adjust for changes in working capital: This step accounts for changes in current assets and liabilities (like accounts receivable, accounts payable, inventory, etc.). For example:

- Increase in accounts receivable: This means sales were made on credit, reducing cash flow.

- Increase in accounts payable: This means the company delayed payments, so cash flow is increased.

- Other adjustments: Depending on the specifics of the business, adjustments might also be made for gains or losses on the sale of assets, taxes, or interest paid.

Indirect Cash Flow Example

The following is an example of a company's cash flow statement using the indirect method, showing how net income is adjusted to reflect actual cash flow:

Indirect Method Cash Flow Statement for the Year Ended December 31, 2024

Net Income: $120,000

Adjustments to reconcile net income to net cash provided by operating activities:

- Add: Depreciation: $30,000

(Non-cash expense that reduces net income but doesn’t impact cash flow) - Add: Loss on sale of equipment: $5,000

(Non-cash loss, which will be added back to reflect the actual cash flow) - Subtract: Gain on sale of investments: $(8,000)

(Non-cash gain, so it's subtracted since it doesn’t represent a real cash inflow)

Changes in working capital:

- Increase in accounts receivable: $(15,000)

(More sales on credit, meaning less cash received) - Decrease in inventory: $10,000

(Reduction in inventory, meaning cash was freed up) - Increase in accounts payable: $7,000

(Paid less to suppliers, which increases cash flow)

Net Cash Provided by Operating Activities: $149,000

Read Also: Levered Free Cash Flow Formula: Calculating & Examples

Pros and Cons of Indirect Cash Flow

The indirect method is the most commonly used method for preparing cash flow statements, mainly because it’s easier to prepare using data readily available from financial statements. However, it doesn’t provide as clear a picture of actual cash inflows and outflows as the direct method does.

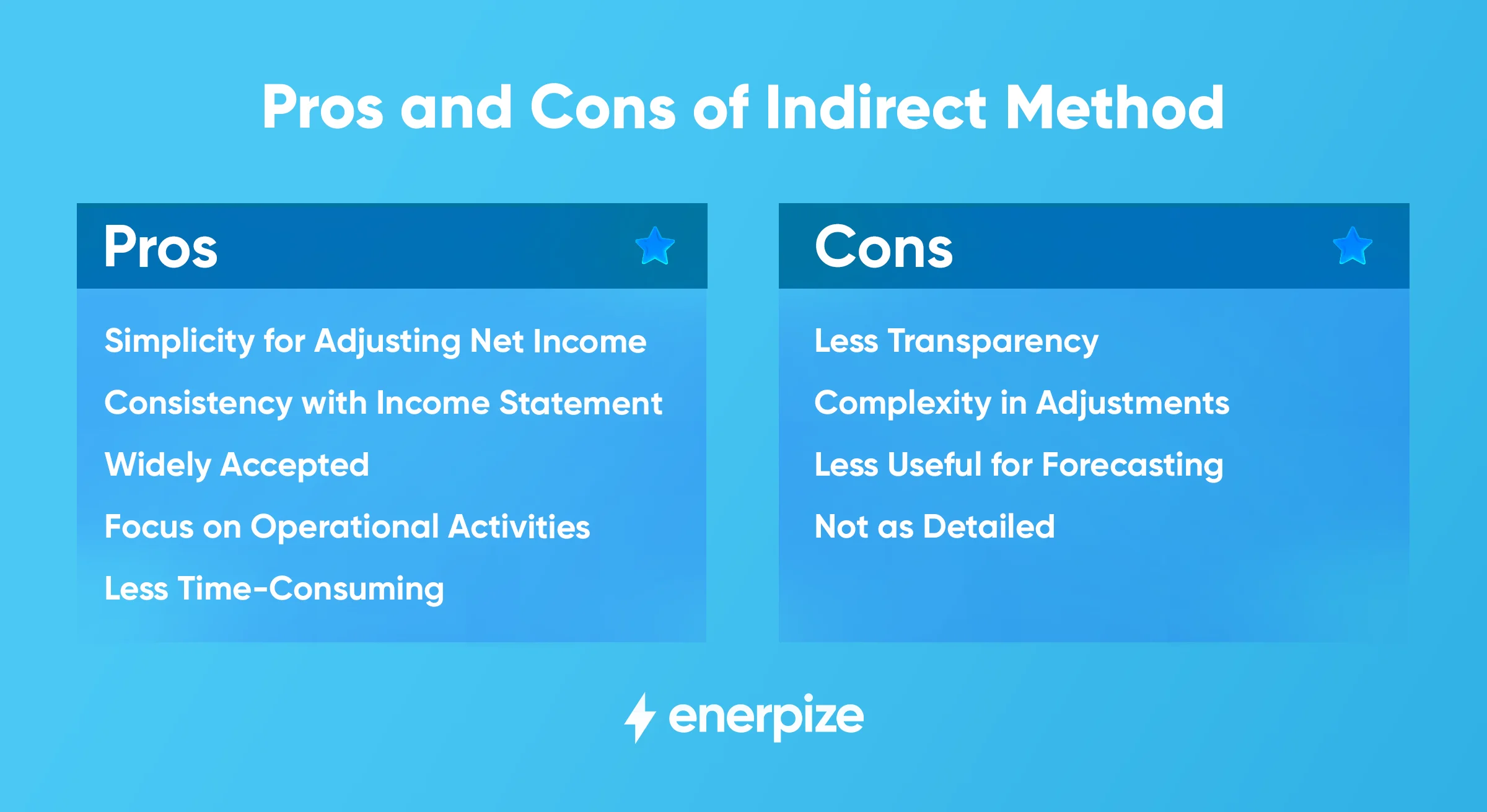

Indirect Method Pros

Simplicity for Adjusting Net Income

The indirect method starts with net income, making it easier to adjust for non-cash items like depreciation, changes in working capital, and other non-operating activities. This can be more intuitive for users who are already familiar with net income.

Consistency with Income Statement

Since it begins with net income, it offers a clear bridge between accrual accounting and cash flow, showing how accrual-based net income translates into actual cash.

Widely Accepted

It’s the more commonly used method in financial reporting, particularly for public companies. This means most financial analysts, investors, and stakeholders are accustomed to seeing it, making comparisons easier across companies and industries.

Focus on Operational Activities

The indirect method is good for highlighting the key operational factors that impact cash flow, such as changes in working capital and non-cash expenses like depreciation.

Less Time-Consuming

Compared to the direct method, it requires less effort to prepare because you don’t have to gather data on all the cash receipts and payments from operations. Instead, you just adjust the net income for the changes in non-cash items.

Indirect Method Cons

Less Transparency

The indirect method doesn't provide a detailed view of the specific cash inflows and outflows from operations. This can make it harder for users to understand exactly how cash is being generated or spent in the day-to-day business operations.

Complexity in Adjustments

While it starts with net income, adjusting for items like working capital changes, non-cash expenses, and gains/losses on asset sales can be complex. For users who aren’t familiar with accounting, it can be hard to follow the logic behind these adjustments.

Read Also: Adjusting Journal Entries: Definition, Types, and Examples

Less Useful for Forecasting

The indirect method doesn't give as clear a picture of future cash flows from operations because it’s based on historical accrual accounting. For investors or analysts focused on projecting future cash flow, the direct method may be more insightful.

Not as Detailed

Unlike the direct method, which shows exact cash receipts and payments, the indirect method can be less clear, where it's unclear how specific items impact cash flow. For example, changes in accounts payable or receivable aren't immediately obvious.

Read Also: How to Calculate Discounted Cash Flow? Formula & Examples

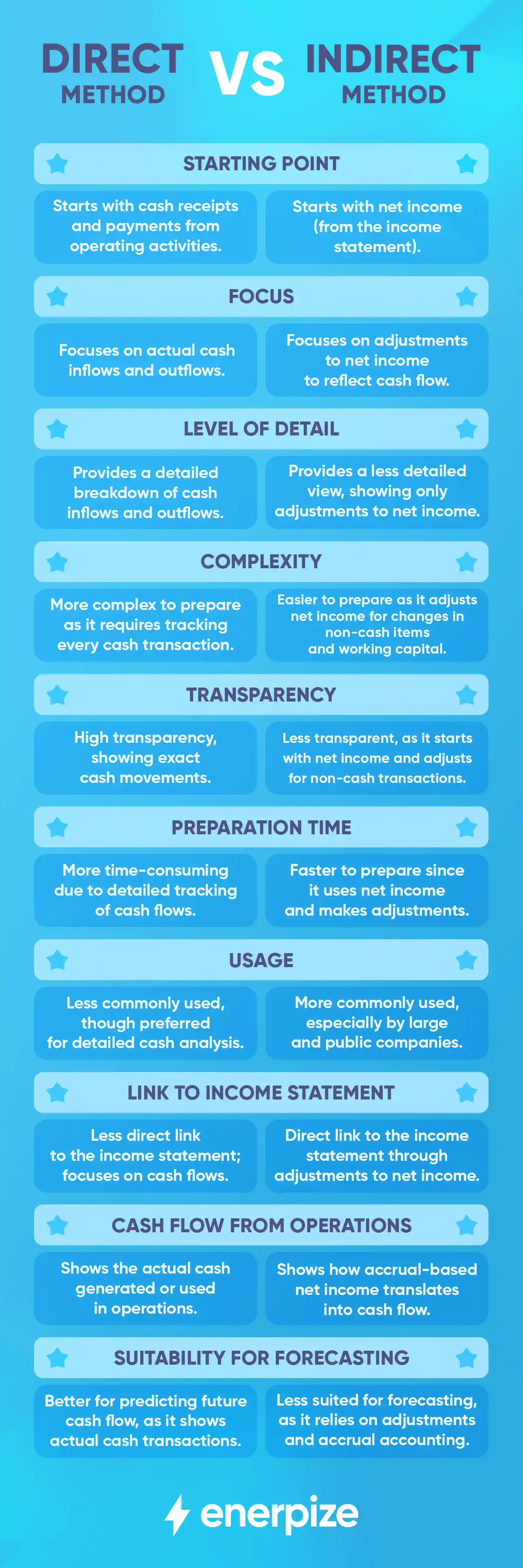

Direct Vs Indirect Cash Flow

The main difference between the direct and indirect methods lies in how cash flow is presented, with the direct method focusing on actual cash transactions and the indirect method adjusting net income for non-cash items. Here is a comparison between indirect vs direct cash flow based on various aspects:

Direct Vs Indirect Methods And Cash Flow Statement

The choice between the direct and indirect cash flow methods primarily affects the operating activities section. The key differences between them are:

- The direct method focuses on actual cash transactions, making it easier to understand cash flows but harder to prepare.

- The indirect method starts with net income and adjusts for non-cash items to reconcile it to cash flow, making it easier to prepare but less transparent about specific cash inflows and outflows.

1- Direct Cash Flow

The direct method shows actual cash inflows and outflows from operating activities. It lists major categories of cash receipts and payments, such as:

- Cash received from customers

- Cash paid to suppliers and employees

- Cash paid for interest and taxes

Reflection on the Cash Flow Statement:

- Provides a clearer view of where cash is coming from and going in the operating activities section.

- It is more intuitive but less commonly used because it requires detailed cash transaction data.

- The net cash provided by (or used in) operating activities is calculated directly from these cash receipts and payments.

2- Indirect Cash Flow

The indirect method starts with net income from the income statement and adjusts it for non-cash items and changes in working capital to arrive at net cash flow from operating activities.

- Non-cash adjustments include depreciation, amortization, and gains/losses on asset sales.

- Changes in working capital accounts (e.g., accounts receivable, inventory, accounts payable) are also adjusted.

Reflection on the Cash Flow Statement:

- Focuses on reconciling net income to cash flow from operations.

- It is more commonly used because it is easier to prepare using accrual-based accounting data.

- The net cash provided by (or used in) operating activities is derived indirectly by adjusting net income.

Direct Vs Indirect Cash Flow: Which Is Better?

The choice between the direct and indirect cash flow methods depends on the intended use and audience. The indirect method is generally considered better for external financial reporting because it is easier to prepare, aligns with accrual accounting systems, and is widely accepted by stakeholders. It starts with net income and adjusts for non-cash items and changes in working capital, making it more practical for most companies.

However, the direct method is better for internal management and cash flow analysis, as it provides a clearer, more detailed view of actual cash inflows and outflows, aiding in cash management and decision-making. While the direct method offers greater transparency, its complexity and data requirements make the indirect method the preferred choice for most external reporting purposes.

Streamline Cash Flow Management with Enerpize

Effective cash flow management is essential for the growth and stability of any business. With Enerpize advanced online accounting software, you can simplify the process of tracking, managing, and forecasting your cash flow. Enerpize offers a user-friendly platform that helps you gain full visibility into your financial operations in real-time, ensuring you always know where your cash is coming from and where it’s going.

By automating routine tasks like invoicing, bill payments, and transaction categorization, Enerpize reduces manual work, allowing you to focus on running your business. The software also provides intuitive financial statements, helping you predict future cash needs, avoid potential shortfalls, and make smarter financial decisions.

Enerpize integrates with your bank accounts, automatically syncing your transactions to give you up-to-date insights into your cash flow situation. Its detailed reports highlight key trends, enabling you to identify patterns, assess liquidity, and track cash flow from operations, all in one place. Whether you're managing accounts payable, accounts receivable, or preparing for taxes, Enerpize streamlines these processes and ensures you stay organized and compliant.

Managing cash flow is easy with Enerpize.

Try our accounting module to control your cash flow smoothly.

Managing cash flow is easy with Enerpize.

Try our accounting module to control your cash flow smoothly.