Create and send online quotations and invoices, track sales, monitor staff performance, and sell & sync all your products via our POS and more.

Posted on 7 April 2025

Author : Haya Assem

Reviewed By : Enerpize Team

Author : Haya Assem

Reviewed By : Enerpize Team

Payroll Journal Entries in Accounting: Definition, Types, and Examples

Payroll journal entries are essential for accurate financial accounting, especially when it comes to managing employee compensation. They capture every detail of the payroll process, from gross pay to deductions, and ensure that all financial impacts are properly recorded. Whether it's regular wages, accrued payrolls, or manual payments, understanding how to create and manage these entries is essential for maintaining financial integrity and compliance within your business.

What are Payroll Journal Entries?

Payroll journal entries are essential accounting records that detail the financial impact of compensating employees. They track the gross pay, which is the total earnings before any deductions. Deductions include withholdings for taxes, social security, and other benefits, which are recorded as liabilities until paid.

Additionally, employer contributions to benefits like health insurance and retirement plans are accounted for. The net pay, which is the amount actually paid out to employees after deductions, is also recorded. These entries help accurately reflect payroll expenses and manage related liabilities, ensuring precise financial reporting and compliance with regulations.

Importance of Payroll Journal Entries in Accounting

Payroll journal entries are critical to the accounting process because they provide a basis for tracking and managing employee-related financial transactions. Businesses that regularly record payroll details may keep precise and reliable financial records, which are required for several objectives, from financial reporting to strategic planning. The importance of these entries extends beyond mere bookkeeping, as they directly impact a company's compliance, financial management, and overall financial health.

Accurate Financial Reporting

Payroll journal entries ensure that all employee compensation, including gross pay, deductions, and employer contributions, are accurately recorded in the financial statements. This provides a clear and complete picture of a company's payroll expenses.

Compliance with Regulations

Properly recorded payroll entries help businesses comply with tax laws and labor regulations. Accurate tracking of deductions like income tax and social security ensures that the correct amounts are withheld and reported to tax authorities, reducing the risk of penalties.

Expense Management

One of a business's largest expenses is payroll. By carefully recording payroll transactions, companies can better manage and control their payroll costs, identifying areas where efficiencies can be gained.

Liability Tracking

Payroll entries help track liabilities such as unpaid wages, employee benefits, and payroll taxes. This ensures that the business knows exactly what it owes and when payments are due, helping to manage cash flow effectively.

Budgeting and Forecasting

Accurate payroll records provide valuable data for budgeting and forecasting. Companies can analyze payroll trends, predict future payroll expenses, and make informed financial decisions based on this information.

3 Types of Payroll Journal Entries

Three main types of payroll journal entries are commonly used in accounting. Each type serves a specific purpose in accurately recording and tracking payroll transactions within a company:

- Initial Recording

- Accrued Wages

- Manual Payments

Initial Recording

This entry sounds like a primary entry that is created when payroll is completed and comprises all aspects of employee compensation. It records total gross pay, employee deductions, and employer contributions. The purpose of this entry is to record the overall payroll expenses and associated liabilities.

Accrued Wages

Accrued payroll entries are used to record payroll expenses that have been incurred but have not yet been paid. This is often done at the end of an accounting period to ensure that all payroll expenses are recorded in the correct period, even if the actual payment will be made in the next period.

Manual Payment

A manual payment entry is a type of payroll journal entry used when payroll payments are processed outside of the regular payroll system or software. This can occur in situations where an employee needs to be paid immediately, adjustments need to be made after payroll has already been processed, or for special payments like bonuses or terminations.

Learn more about adjusting journal entries.

How to Record Payroll Journal Entry

Recording payroll journal entries involves a systematic process to ensure that all aspects of employee compensation are accurately captured in the financial records. Here are the 6 main steps you need to follow:

1- Set Up Payroll Accounts

Start by setting up the necessary payroll accounts in your accounting system. This includes creating expense accounts for wages, salaries, and employer contributions, as well as liability accounts for deductions like taxes, social security, retirement contributions, and health insurance.

Properly categorized accounts ensure that all payroll-related transactions are recorded accurately. Ensure the account structure aligns with your company's chart of accounts, making it easier to track and report payroll expenses and liabilities.

2- Calculate Taxes and Other Deductions

Calculate the total gross pay for each employee based on their salary or hourly wage, including any overtime, bonuses, or commissions. Determine all required deductions from gross pay. This includes federal, state, and local taxes, social security, Medicare, health insurance premiums, retirement contributions, and any other withholdings.

These deductions will be recorded as liabilities in the payroll journal entry. Calculate the employer's share of payroll taxes (like social security and Medicare) and any contributions to employee benefits, which will be recorded as expenses.

3- Gather Payroll Reports

Gather detailed payroll reports from your payroll system or provider. These reports should include information on gross pay, deductions, employer contributions, and net pay for each employee. Double-check that the data is accurate and complete, as any errors in the payroll reports will lead to inaccurate journal entries.

4- Record Payroll Expenses

Using the data from your payroll reports, record the total gross pay as a debit in the appropriate payroll expense accounts. This includes wages, salaries, and employer-paid benefits.

Record any employer contributions as additional payroll expenses. For example, the employer's share of payroll taxes or contributions to retirement plans should be debited to the relevant expense accounts.

Learn more about payroll cheat sheets and how payroll is calculated.

5- Record Payables

For each deduction calculated, credit the corresponding liability account. For instance, withholdings for income tax should be credited to "Income Tax Payable," social security deductions to "Social Security Payable," and health insurance premiums to "Health Insurance Payable."

The amount of net pay, which is the gross pay minus deductions, should be credited to the "Cash" or "Bank" account, representing the actual payment made to employees.

Read Also: Journal Entries for Bank Reconciliation: A Comprehensive Guide

6- Review All Records

Carefully review all payroll journal entries to ensure that they are accurate and balanced. Check that the total debits (expenses) match the total credits (liabilities and cash outflows).

Implement internal controls such as approval processes and audits to ensure the integrity of the payroll records. This helps prevent errors and fraud. Ensure that all payroll entries comply with relevant tax laws and regulations, as incorrect entries can lead to compliance issues and penalties.

Download Now: Free Payroll Journal Entry Template Excel

Read also:

Prepaid Expense Journal Entries: Importance, Examples & How to Record?

Intercompany Transactions Journal Entries: Importance & Examples

Lease Accounting Journal Entries: Types, Standards & Calculating Steps

Payroll Journal Entries Examples

Initial Payroll Journal Entry

A company has processed payroll for the week. An employee earns $3,000 in gross pay. Deductions include $400 for federal income tax, $200 for state income tax, $230 for Social Security, $70 for Medicare, and $100 for health insurance. The employer's contributions include $230 for Social Security, $70 for Medicare, and $100 for health insurance.

Journal Entry:

Accrued Payroll Entry

Employees have earned payroll but will not be paid until the following period. Employees have earned $15,000 in gross wages, but the payment will be made next week. Deductions still need to be recorded; only the gross amount is accrued.

Journal Entry:

Manual Payment Entry

An employee is paid a bonus of $500, processed outside the regular payroll cycle. The bonus is subject to a 10% tax deduction.

Journal Entry:

Download Now: Free Payroll Template in Excel and Word

Best System for Payroll Journal Entries Recording

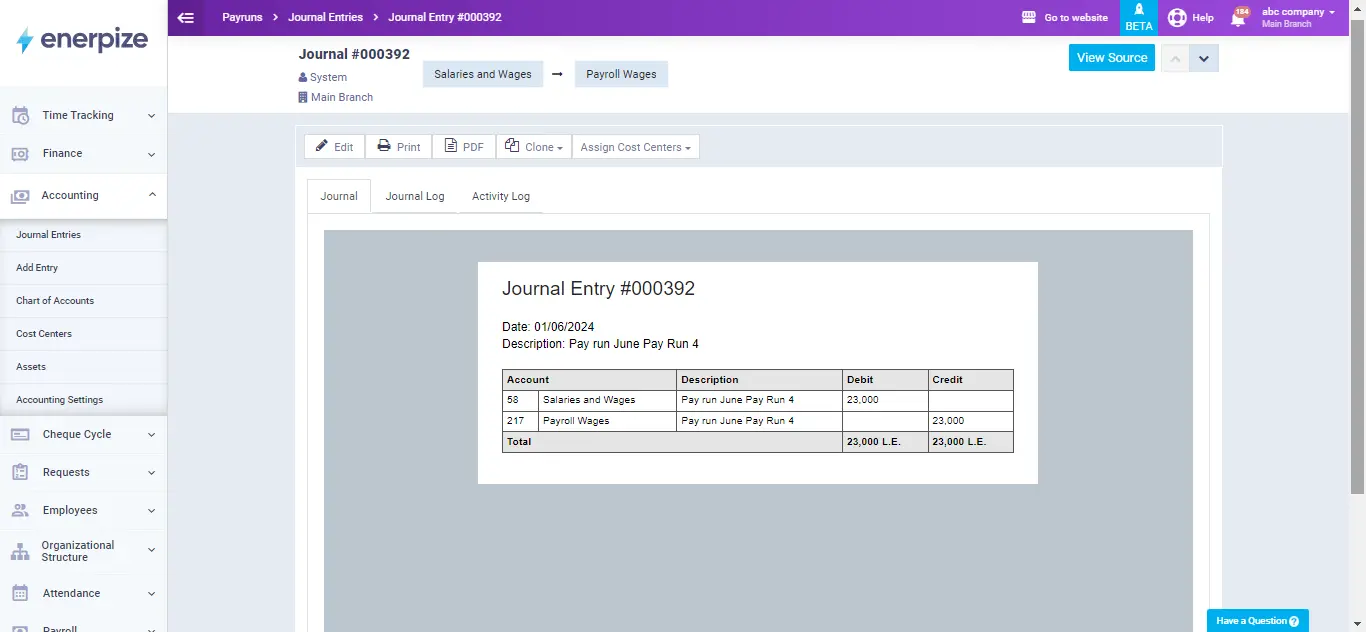

Managing payroll journal entries can be a time-consuming and challenging task, often involving manual calculations, careful balancing of accounts, and ensuring compliance with various regulations. This is where the payroll journal entry recording systems shine.

Enerpize's payroll management system automates the process by accurately calculating gross pay, deductions, and employer contributions and then seamlessly recording these transactions into the appropriate accounts. Once recorded, the system automatically balances the entries and transfers them to the general ledger, ensuring that your financial statements reflect the latest payroll data.

Additionally, Enerpize is developed to handle payroll complexities, such as accrued payrolls, and initial, and manual payments, effortlessly. By streamlining these tasks, our online accounting software saves your valuable time and reduces the risk of errors, making your accounting processes more efficient and reliable.

Payroll journal entries are easy with Enerpize.

Try our HR payroll module to manage your employee compensation.

Payroll journal entries are easy with Enerpize.

Try our HR payroll module to manage your employee compensation.