Author : Enerpize Team

Cash Flow Statement: Definition & How To Read

Table of contents:

- What Is A Cash Flow Statement?

- Purpose of Cash Flow Statement

- The Cash Flow Statement Main Components

- How to Prepare a Cash Flow Statement?

- Cash Flow Statement Example

- How to Calculate Cash Flow Statements?

- How to Read a Cash Flow Statement

- Cash Flow Statement VS Financial Statements

- How to Improve Cash Flow for Your Business

- Common Mistakes in Creating Cash Flow to Avoid

- How Enerpize Helps You Create Your Cash Flow Statement

- FAQs

A cash flow statement definition helps you assess your business's position in the most important business metric: real cash. It shows how money moves in and out of your business, making it easier to determine if you can cover expenses, invest in growth, or handle financial challenges.

While profit reports can look positive, the cash flow statement reveals what’s actually happening behind the numbers. The cash flow statement summarizes operating performance, investment, and financing operations, providing you with a comprehensive view of your business's financial health and stability.

Key Takeaways

- Cash flow statements are vital financial tools that show a company’s real-time cash inflows and outflows. They help determine if a business can meet financial obligations and maintain a healthy cash position.

- Unlike income statements and balance sheets, cash flow statements track only actual cash transactions. They’re especially useful for managing liquidity and planning budgets.

- Cash flow comes from three main sources: operations, investing, and financing. These activities show how cash moves through business functions like sales and asset purchases.

- Cash flow from operations includes sales revenue, payments, taxes, and payroll, capturing the cash impact of day-to-day activities that keep the business running.

- Investing cash flow shows money spent on or earned from assets like equipment or property. Inflows include selling investments, while outflows involve purchases or loans.

- Financing cash flow involves money raised from or paid to shareholders and creditors. Issuing stock or taking loans brings cash in, while repaying debts or dividends sends cash out.

- Businesses can prepare cash flow statements using either the direct method or the indirect method, helping reconcile cash balances accurately.

What Is A Cash Flow Statement?

A cash flow statement is a financial report that shows the movement of cash in and out of a business over a specific period. It helps businesses understand how money is generated and used, providing insight into liquidity and financial health.

A cash flow statement can help you determine whether a business has enough cash to cover its expenses, invest in growth, and pay debts, making it essential for financial planning.

Cash flow statements can also be prepared using the indirect cash flow statement method, which adjusts net income for changes in working capital and non-cash items to calculate cash from operating activities.

A cash flow statement is typically divided into three sections:

- Operating Activities: Cash generated or used from the core business operations, like receiving payments from customers or paying suppliers and employees.

- Investing Activities: Cash spent on or received from investments, such as buying equipment, property, or selling investments.

- Financing Activities: Cash received from or paid to investors and lenders, including loans, dividends, or issuing stock.

Purpose of Cash Flow Statement

The statement of cash flow provides a clear view of cash movement for a business, helping a business owner, stakeholders, or investors understand the company’s liquidity position and overall financial health.

It also answers why the cash flow statement is important for businesses, because it shows actual cash availability, supporting operational decisions, investment planning, and debt management.

Tracking Cash Inflow and Outflows

This part of the statement shows where money is coming from. It helps business identifies major cash sources, such as customer payments or investment income, and areas where cash is going out, like supplier payments, salaries, or loan repayment.

Liquidity Assessment

The key indicator of a company’s financial position is its ability to meet short-term obligations, in other words, its liquidity. The cash flow statement allows business owners and managers to see if there is enough cash on hand to cover day-to-day expenses, repay debts, or handle unexpected costs. A positive cash flow indicates financial stability, while a negative cash flow signals the need for careful planning.

Future Planning

Cash flow statements provide critical insights that support strategic decisions. For example, management can decide whether to invest in new equipment, expand operations, or delay certain expenditures. It also helps lenders and investors evaluate the company’s financial health before providing funding.

Operational Efficiency Tracking

By analyzing cash generated from core business operations, companies can assess how efficiently they convert sales into cash. Consistent positive operating cash flow indicates a healthy business model, while repeated shortfalls may highlight issues like slow collections or high operating costs.

The Cash Flow Statement Main Components

A cash flow statement is divided into three essential sections. Each one explains how different business activities affect cash movement during the period. The cash flow statement components are:

1- Operating Activities

This section shows the cash generated or used through the company’s regular business operations. It includes cash received from customers, payments made to suppliers, payroll, rent, utilities, and other day-to-day expenses. A consistent positive operational cash flow indicates that the core business is healthy and generating enough cash to sustain itself.

2- Investing Activities

Investing activities include long-term investments in the company. This involves purchasing or selling equipment, vehicles, buildings, or other fixed assets, as well as earnings or losses on investment securities.

Cash outflows often occur when businesses acquire new assets, while cash inflows result from the sale of existing or unused assets. This section displays how much the business is reinvesting in future growth.

3- Financing Activities

This component refers to how the company finances its operations and expansion. It includes cash from borrowing (such as business loans), repaying those loans, issuing shares, and paying dividends to owners or shareholders. Positive financing cash flow indicates that the company is raising money, while negative cash flow often suggests debt repayment or dividend disruptions.

Tip: Enerpize Accounting Software automatically categorizes cash transactions into operating, investing, and financing activities, generating accurate, easy-to-read cash flow statements that help you instantly understand your business’s financial direction.

Read Also: How to Calculate Discounted Cash Flow? Formula & Examples

How to Prepare a Cash Flow Statement?

Preparing a cash flow statement helps you understand exactly how cash moves in and out of your business. By following a systematic approach, you can ensure accuracy and gain insights that support better financial decisions.

1- Gather Required Financial Documents

Collect your opening and closing balance sheets, income statement (profit & loss), and supporting schedules such as debt records, fixed-asset purchases or sales, and dividend information. These documents form the basis for converting accrual accounting figures into actual cash movements.

2- Categorize Cash Activities

Separate cash transactions into three main categories:

- Operating Activities: Cash from core business operations.

- Investing Activities: Cash from buying or selling long-term assets.

- Financing Activities: Cash from loans, equity, or dividend payments.

3- Adjust for Non-Cash Items

Remove non-cash expenses, such as depreciation in the cash flow statement or amortization from your operating activities, as these do not affect actual cash flow.

4- Account for Changes in Working Capital

Adjust for increases or decreases in accounts receivable, accounts payable, and inventory to reflect the actual cash available from operations.

5- Calculate Net Cash Flow

Sum the cash flows from operating, investing, and financing activities to determine the net change in cash for the period.

6- Reconcile Cash Balances

Ensure that the net change in cash aligns with the difference between the opening and closing cash balances on your balance sheet.

You might also find this helpful: What are Opening Journal Entries in Accounting?

Note: Enerpize Accounting Software streamlines cash flow statement preparation by automatically categorizing transactions, tracking working capital, and reconciling cash balances.

To simplify the process, you can use the Enerpize Cash Flow Statement Template to organize your data and perform calculations efficiently.

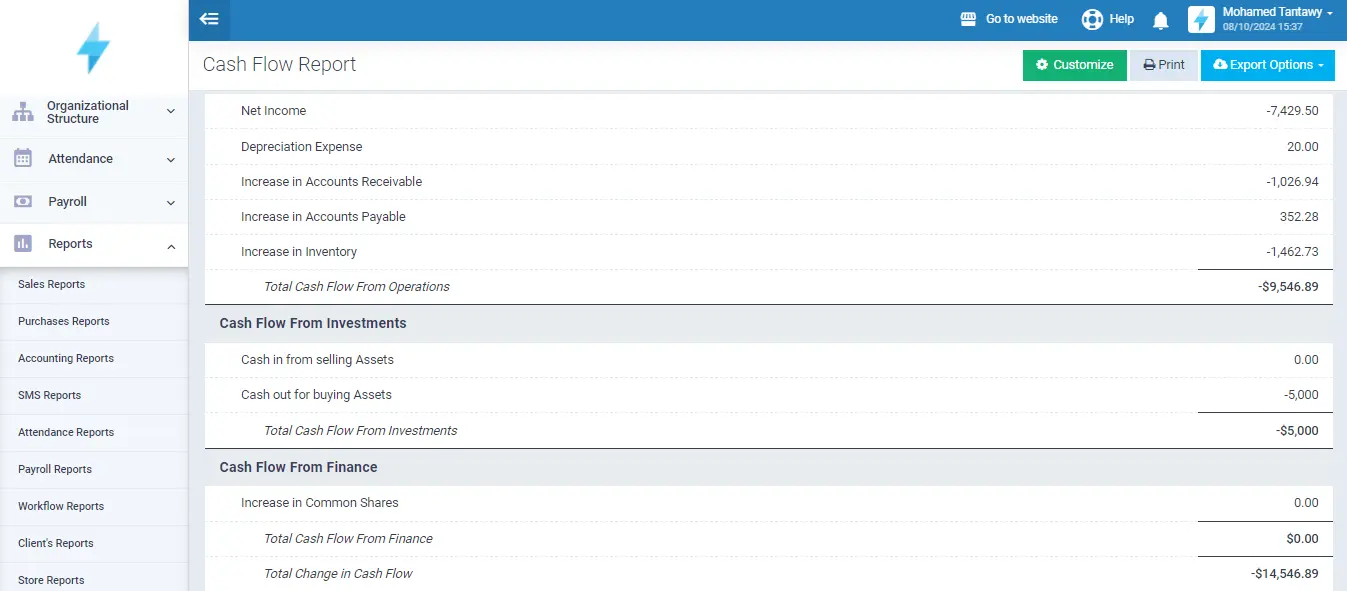

Cash Flow Statement Example

| Cash Flows from Operating Activities | Amount (USD) |

| Net Income | 80,000 |

| Adjustments for: | |

| - Depreciation | 15,000 |

| - Amortization | 7,000 |

| - Gain on sale of equipment | (3,000) |

| - Increase in accounts receivable | (6,000) |

| - Increase in inventory | (10,000) |

| - Increase in accounts payable | 5,000 |

| - Decrease in accrued expenses | (2,000) |

| Net Cash from Operating Activities | 86,000 |

| Cash Flows from Investing Activities | Amount (USD) |

| Purchase of equipment | (25,000) |

| Proceeds from sale of equipment | 12,000 |

| Purchase of investments | (8,000) |

| Net Cash Used in Investing Activities | (21,000) |

| Cash Flows from Financing Activities | Amount (USD) |

| Proceeds from issuance of common stock | 20,000 |

| Payment of dividends | (10,000) |

| Repayment of long-term debt | (15,000) |

| Net Cash Used in Financing Activities | (5,000) |

The above cash flow statement shows a positive net cash flow of USD 86,000 for 2023 generated from operating activities. This positive value generally reflects a robust and active investment strategy and signals sound financial health for investors. A robust financial performance will likely positively impact a company’s valuation. One recent example is that of OpenAI, which, having been front and center of Generative AI innovation, is now valued at USD 157 bn.

The USD 10,000 end-of-year net cash flow underscores its comfortable cash cushion to invest more, pay off debts, or buffer against possible emerging contingencies.

Read Also: What is Levered Free Cash Flow? And How to Calculate?

How to Calculate Cash Flow Statements?

Calculating cash flow can be performed in two primary ways:

Direct Cash Flow Method:

Add up all cash payments and receipts. Or, you can use your beginning and ending balances of a range of your asset and liability accounts and examine net decreases or increases in your selected accounts.

Indirect Cash Flow Method:

Adjust net income by adding or subtracting non-cash entries differences, as reported in your company’s asset and liability accounts (which should also appear in your balance sheet). Predictably enough, decreases or increases in all asset and liability accounts (such as accounts receivable and inventory) reflect non-cash calculation actions where deductions or additions are made, respectively, in each relevant account.

Read More: Direct VS Indirect Cash Flow: A Comprehensive Guide

How to Read a Cash Flow Statement

Reading a cash flow statement effectively helps you understand a company’s liquidity, operational efficiency, and overall financial health. By examining each section carefully, you can identify strengths, weaknesses, and potential risks in cash management. Follow the steps below to learn how cash moves through your business:

1- Start with Operating Activities

Start with examining the operating activities section, which reflects how much cash the company generates from its core business operations.

- A positive operating cash flow means the business is generating enough cash to sustain itself.

- A negative operating cash flow may signal poor collections, high expenses, or operational inefficiencies.

2- Analyze Investing Activities

Next, review the investing activities section. This shows cash spent on long-term assets like equipment, property, or investments.

- Cash outflows here often indicate growth and expansion (e.g., buying equipment).

- Cash inflows may come from selling assets.

Look for a balance: frequent heavy outflows may indicate growth, but too many inflows from asset sales could be a warning sign.

3- Evaluate Financing Activities

The Financing Activities section shows how the company funds its operations through loans, owner contributions, issuing shares, or paying dividends.

- Positive cash flow here means the company is raising capital.

- Negative cash flow often means repaying loans or paying dividends.

This helps you understand whether the company relies heavily on external funding.

4- Compare Net Cash Flow to Income

Compare net cash flow (total cash movement) with net income from the income statement.

- If net income is high but cash flow is low, the business may have collection problems or be too tied up in inventory.

- If cash flow is strong but income is low, the business may be efficient in cash management or delaying expenses.

This comparison gives a deeper insight into actual performance beyond profit figures.

5- Check the Opening and Closing Cash Balances

Finally, make sure the movement of cash matches the change from opening to closing cash.

This ensures the cash flow statement is consistent with the balance sheet and helps you confirm the accuracy of the calculations.

Note: Enerpize simplifies reading cash flow statements by automatically categorizing transactions, tracking cash inflows and outflows, and reconciling balances. This provides a clear, real-time view of liquidity, helping you analyze operating efficiency and make informed financial decisions quickly

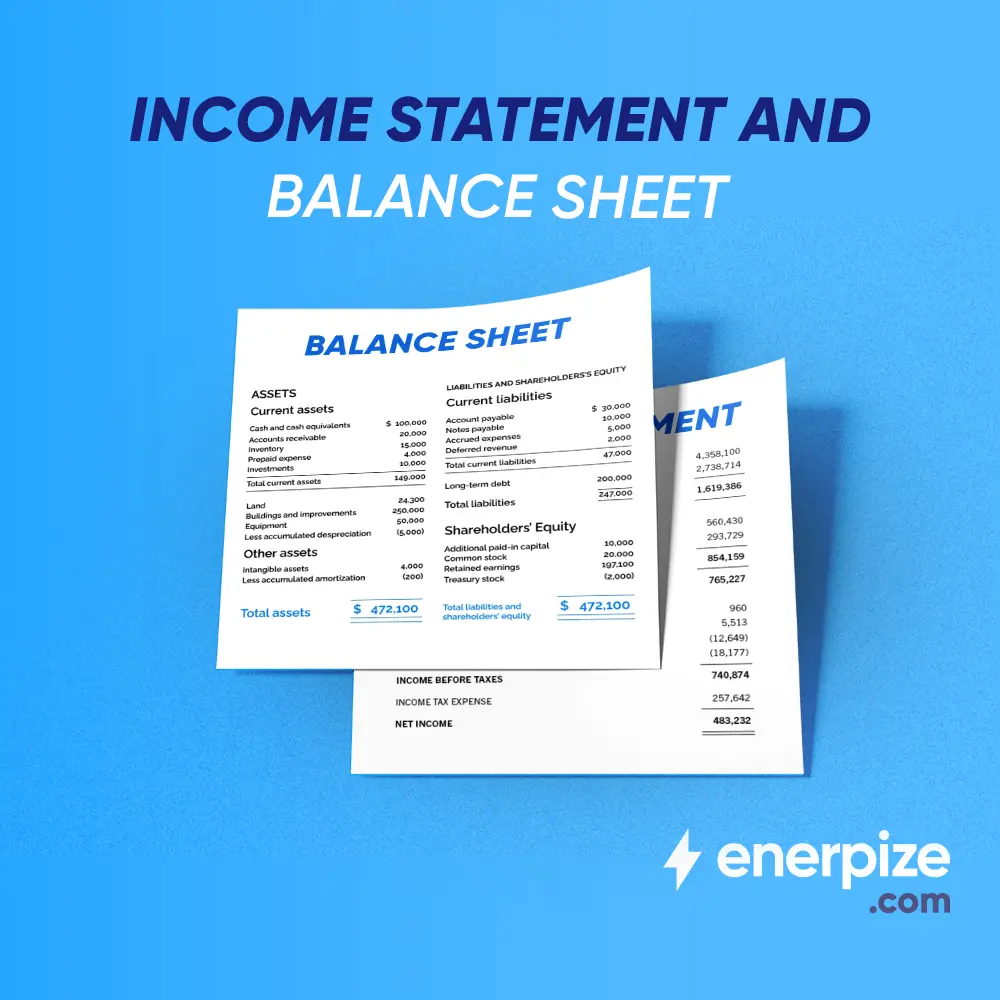

Cash Flow Statement VS Financial Statements

The cash flow statement records all cash-based incoming or outgoing financial transactions. Importantly, cash flow statements record actual, not future, cash transactions. As such, cash flow statements represent an indispensable account of financial records for all transactions made exclusively in cash.

Still, necessary as they are, cash flow statements alone are not enough to account for all financial activities, such as non-cash transactions. This is where a wide range of financial statements provides more detailed information.

How income statements and balance sheets compare to cash flow statements is discussed next.

Read Also: Pro Forma Cash Flow Statement: A Comprehensive Guide

Cash Flow Statement VS Income Statement

| Points of Comparison | Cash Flow Statement | Income Statement |

| Focus | Shows the actual movement of cash entering and leaving the business. | Shows the company’s revenues, expenses, and net profit, even if cash has not yet been exchanged. |

| Basis | Records only cash-based transactions. Non-cash items are excluded. | Uses the accrual method, including non-cash items such as depreciation, amortization, and credit sales. |

| Purpose | Help determine whether the business has enough cash to operate, pay bills, invest, or handle short-term obligations. | Help determine profitability and how efficiently the business generates income from its operations. |

| Timing | Measures real cash activity during a specific period | Covers financial performance during a period, focusing on income earned and expenses incurred, not actual cash. |

| Insights Provided | Reveals Liquidity strength, cash shortages, working capital trends, and operational efficiency. | Reveals gross profit, net profit, expenses behavior, and overall operational performance. |

| Use Cases | Useful for evaluating investment decisions, monitoring daily cash needs, and planning payments | Useful for strategic decisions such as expansion, securing funding, pricing strategy, and performance evaluation. |

| Primary Users | Financial planners, controllers, and investors are monitoring the company’s cash position. | Managers, investors, and lenders assess profitability and long-term growth potential. |

Read Also: How to Prepare an Income Statement

Cash Flow Statement VS Balance Sheet

| Points of Comparison | Cash Flow Statement | Balance Sheet |

| Focus | Track cash inflows and outflows from operating, investing, and financing activities. | Presents the company’s assets, liabilities, and shareholders' equity at a specific point in time. |

| Basis | Contains only cash and cash-equivalents information, showing what was actually received or spent. | Contains all financial resources and obligations, including cash, receivables, inventory, equipment, loans, and equity. |

| Purpose | Help assess short-term liquidity and the company’s ability to manage cash effectively. | Shows overall financial health, stability, and the company’s net worth. |

| Timing | Covers cash activity over a reporting period. | Provides a snapshot of the company’s financial position on a specific date. |

| Insights Provided | Highlights operational efficiency, investment activity, and funding sources. | Reveals leverage, asset base, liquidity ratios, solvency, and shareholder value. |

| Use Cases | Used to plan cash needs, manage working capital, and make short-term decisions. | Used to evaluate long-term viability, borrowing capacity, valuation, and financial risk. |

| Primary Users | Planners and controllers analyze cash health and short-term stability. | Investors, analysts, lenders, and executives assess overall financial strength and growth potential. |

Read Also: Comparative Balance Sheet: A Comprehensive Guide

How to Improve Cash Flow for Your Business

Cutting costs can slightly improve your cash flow, but there are other, smarter, and faster financial decisions you can make to keep your business's cash flow moving effectively, such as:

Speed Up Customer Payments

Send invoices promptly, offer early payment discounts, and utilize automated invoicing software to minimize delays.

Control Expenses Without Disrupting Operations

Review subscriptions, renegotiate vendor contracts, and eliminate non-essential spending.

Keep Inventory Lean

Avoid overstocking. Use sales data to buy only what sells and free up cash tied up in slow-moving inventory.

Improve Profit Margins

Revisit pricing, bundle services, or introduce high-margin offerings to boost revenue without increasing costs.

Strengthen Your Billing Process

Implement clear payment terms, set automated reminders, and follow up consistently.

Access Financing When Needed

Use short-term loans, credit lines, or invoice factoring to cover temporary cash gaps.

Optimize Cash Flow with Technology

Cash flow tools and accounting platforms, like Enerpize, help track real-time inflows and outflows so you can act before issues arise.

Common Mistakes in Creating Cash Flow to Avoid

Several common errors can lead to misleading results in creating an accurate cash flow statement. Avoid these mistakes to ensure your cash flow reflects your business’s real financial position:

Mixing Cash and Non-Cash Items

Including non-cash expenses like depreciation or amortization in cash flow totals leads to inaccurate results. These items belong in the income statement, not the cash flow statement.

Misclassifying Cash Activities

Placing operating activities under investing or financing (or vice versa) can distort insights. Each cash movement must be assigned to the correct category.

Ignoring Changes in Working Capital

Forgetting to adjust for changes in accounts receivable, accounts payable, or inventory often results in overstated or understated cash flow from operations.

Overlooking One-Time Transactions

Special items such as asset sales, loan drawdowns, or large tax payments should be recorded correctly to avoid misleading cash trends.

Not Reconciling Beginning and Ending Cash Balances

Failing to ensure the final cash balance matches the balance sheet creates inconsistencies and signals errors in the statement.

Relying on Estimates Instead of Actual Data

Using assumptions instead of verified numbers leads to inaccurate cash flow insights and poor financial decision-making.

Note: Enerpize helps you avoid these mistakes by automatically categorizing cash transactions, tracking working capital changes, and reconciling cash balances.

How Enerpize Helps You Create Your Cash Flow Statement

Managing cash flow can be challenging, especially when relying on manual processes. Enerpize is an online accounting software and ERP system designed to simplify financial management for businesses of all sizes.

It helps track transactions accurately, automates calculations, and provides a clear, real-time view of a company’s financial position. When preparing a cash flow statement, Enerpize streamlines the process, ensuring accuracy and providing business owners and managers with reliable insights into cash movements for better decision-making.

- Automated Cash Categorization: All cash transactions are automatically sorted into operating, investing, and financing activities, saving time and reducing errors.

- Real-Time Cash Flow Tracking: Enerpize provides an up-to-date view of cash inflows and outflows so you can make decisions with confidence.

- Easy Reconciliation: Beginning and ending cash balances are automatically matched with your balance sheet, ensuring accuracy.

- Working Capital Insights: Track accounts receivable, accounts payable, and inventory changes to clearly understand operational cash flow.

- Quick Reports and Forecasts: Generate detailed cash flow statements and projections instantly to plan for short-term and long-term needs.

- Fewer Errors, More Confidence: Automation reduces manual mistakes, letting you rely on your cash flow data for better financial decisions.

FAQs

Why is the cash flow statement important?

The cash flow statement is important because it shows how cash moves in and out of a business. It helps business owners, managers, and investors understand liquidity, assess the ability to meet short-term obligations, and make informed financial decisions. Unlike profit-focused statements, it reflects the actual cash available to run operations, invest, and manage debts.

What does a cash flow statement show?

A cash flow statement shows the inflows and outflows of cash during a specific period, categorized into operating, investing, and financing activities. It highlights where cash is coming from, where it is going, and the net change in cash, providing a clear picture of a company’s financial health and liquidity.

Cash flow statement is easy with Enerpize.

Try our accounting module to create financial statements automatically.

Cash flow statement is easy with Enerpize.

Try our accounting module to create financial statements automatically.