Create and send online quotations and invoices, track sales, monitor staff performance, and sell & sync all your products via our POS and more.

Posted on 26 February 2024

Author : Haya Assem

Reviewed By : Enerpize Team

Author : Haya Assem

Reviewed By : Enerpize Team

Depreciation Methods and Calculations: Comprehensive Guide

Assets are everything that a company or individual possesses in a project that has monetary or economic worth and is likely to generate profit. Furthermore, everything that might boost sales, reduce expenses, or protect future cash flow is considered an asset. This applies to both patents and machinery.

It is essential to recognize that assets depreciate with time. Depreciation is a gradual decline in an asset's value caused by causes such as wear and tear, technical obsolescence, or the passage of time.

This accounting concept enables organizations to spread the cost of an asset throughout its useful life, accurately representing its declining worth on financial statements. Understanding and accounting for depreciation is critical to keeping accurate financial records and making informed business decisions.

Key Takeaways

- Depreciation is an accounting method showing asset value consumption over time. Calculated in different GAAP-based methods, impacting book value and revenue.

- Depreciation, beyond wear and tear, is a strategic financial tool with six advantages: cost representation, tax reduction, business valuation impact, gradual cost recovery, accurate value depiction, and consistent reporting.

- Depreciation, a key financial consideration, involves methods like Straight-Line, Declining Balance, and Units of Production. Method choice impacts asset value, revenue, and financial health, requiring careful evaluation.

- Depreciation method choice affects reported expenses and asset values on the balance sheet. Straight-line provides consistent reduction, Declining Balance offers initial higher reduction, and Units of Production link closely to actual usage.

What is Depreciation?

Depreciation is an accounting method that illustrates how much of an asset's value has been consumed over a specific time period. Depreciation provides a more accurate picture of an asset's worth and profitability since it is recorded as a recurring expense on the income statement.

Depreciation may be calculated in different methods based on generally accepted accounting principles (GAAP). When selecting a depreciation method, it is crucial to take into account both the asset itself and its intended use. The chosen method has a direct impact on the book value and revenue.

Importance of Depreciation in Accounting

The significance of depreciation extends well beyond mere accounting measures of wear and tear. It develops as a strategic and multifaceted tool, deeply involved in financial decision-making.

Depreciation is an important factor in shaping a company's fiscal picture, providing complex advantages that extend beyond simple cost allocation. Here are the six major advantages of depreciation:

1. Considered as an Expense/Cost

Depreciation is a financial outflow that represents the recurring expense associated with asset wear and tear. This accounting method recognizes that assets lose value over time and counts this loss as a cost spent during the operation of a business.

Read Also: Depreciable Cost: What is & How To Calculate?

2. Can Reduce Your Tax Amount

Depreciation methods can lead to tax benefits, as they allow businesses to deduct the depreciated value of assets from their taxable income. This reduction in taxable income can result in a lower overall tax liability, providing a financial advantage to the business.

3. Impact on Business Valuation

The application of depreciation methods has a direct impact on the overall valuation of a business. As assets depreciate over time, the recorded value on financial statements reflects a more accurate representation of the business's current worth, influencing its perceived financial health.

4. Gradual Asset Cost Recovery

Depreciation serves as a systematic way for businesses to recover the initial cost of acquiring assets. Instead of expensing the entire cost upfront, depreciation allows for a gradual allocation of the asset's cost over its useful life, aligning with the principle of matching expenses to revenues.

5. Contributes to an Accurate Depiction of Value

By factoring in the depreciation of assets, financial statements provide a more precise and realistic depiction of a business's net worth. This precision enables stakeholders, including investors and creditors, to make informed decisions regarding the company's financial position and future development prospects.

6. Consistent Financial Statement

Implementing depreciation ensures consistency in financial reporting by following a systematic approach to recognizing the decline in asset value over time. This consistency facilitates comparability between financial statements over different periods, helping analysts, and stakeholders asses the business's performance and stability.

Read Also: What is the Difference Between Liquid and Illiquid Assets?

Different Ways to Calculate Depreciation

Depreciation is calculated using a variety of methods, each with a distinct influence on asset value, book value, and revenue. Businesses must carefully consider different options since each one has a distinct influence on value than the others.

This decision significantly influences financial reporting and tax considerations, necessitating a thorough understanding of each method's nuances and their implications for overall financial health.

1- Straight-Line Depreciation Method

As simple as it is called, this method is the most basic and most used one to calculate depreciation. The straight-line depreciation method is a typical accounting approach that distributes the cost of a tangible asset evenly over its useful life.

This strategy assumes that the asset's value decreases at a constant rate each year. The formula to calculate straight-line depreciation is:

Depreciation Expense = Cost of Asset - Salvage Value ÷ Useful Life

.png)

Where:

Depreciation Expense: The amount of depreciation to be recorded each year.

Cost of Asset: The original cost or purchase price of the asset.

Salvage Value: The estimated residual value of the asset at the end of its useful life.

Useful Life: The expected number of years the asset will be in service before reaching its salvage value.

Importance of Straight-Line Method

Straight-line depreciation is crucial for its simplicity, consistency, compliance with accounting principles, and its role in facilitating clear and accurate financial reporting.

It ensures that costs align with income, leading to a more consistent and precise assessment of a company's overall profitability. This is achieved through equal and constant depreciation charges, making budgeting and financial planning more straightforward.

It's important to note that the choice of method depends on factors such as the nature of the asset and its pattern of use.

Example of Straight-Line Depreciation

Consider the straight-line depreciation of printing and photocopying equipment owned by an advertising agency. The machine costs 10,000 USD and is projected to perform perfectly for 5 years, thus it has a useful life of 5 years. After 5 years of depreciation, the machine should have a salvage value of 1,000 USD.

Asset Cost: 10,000 USD

Useful Life: 5 Years

Salvage Value: 1,000 USD

Apply the Straight-Line formula:

Depreciation Expense = 10,000 USD - 1,000 USD ÷ 5 = 9,000 USD ÷ 5 = 1,800 USD

Annual Depreciation:

1st Year: 10,000 USD - 1,800 USD = 8,200 USD

2nd Year: 8,200 USD - 1,800 USD = 6,400 USD

3rd Year: 6,400 USD - 1,800 USD = 4,600 USD

4th Year: 4,600 USD - 1,800 USD = 2,800 USD

5th Year: 2,800 USD - 1,800 USD = 1,000 USD (Salvage Value reached; Book Value at the end of Year 5: 1,000 USD

2- Declining Balance (Percentage) Depreciation Method

The Declining Balance method, also known as the double declining balance method, is a popular accelerated depreciation method in accounting. Unlike the straight-line method, the declining balance method allocates higher depreciation expenses in the early years of an asset's useful life, reflecting the fact that assets frequently lose value rapidly in the early years.

The formula to calculate declining balance depreciation is:

Depreciation Expense = Current Book Value × Depreciation Rate

.png)

Importance of Declining Balance Method

The declining balance method is significant as it aims to allocate higher depreciation expenses in the early, more productive years of an asset. This method accurately represents the economic realities of assets with high maintenance costs or rapid technical obsolescence.

Additionally, it offers potential tax advantages by allowing businesses to deduct a larger portion of an asset's cost in the initial years, reducing taxable income and providing a tax shield.

Example of Declining Balance Depreciation:

- The current book value represents the net value of the asset at the beginning of an accounting period, determined by subtracting the accumulated depreciation from the fixed asset's cost.

- The residual value indicates the anticipated salvage value when the asset reaches the end of its useful life. The depreciation rate is determined based on the projected usage pattern of the asset throughout its useful life.

- To illustrate, consider an asset with a cost of $2,000, a salvage value of $200, and a 15-year life, depreciating at a rate of 20% per year.

- In this case, the expense would be $400 in the first year, $320 in the second year, $256 in the third year, and so on for the rest of the years

3- Units of Production Depreciation Method

The Units of Production depreciation method is an accounting method that distributes the cost of an asset based on its actual usage or output during its useful life. This method is especially useful for assets whose wear and tear is directly proportional to the volume of production or usage.

The formula to calculate Units Of Production depreciation is:

(Cost of Asset - Salvage Value ÷ Estimated total production units) × Actual Units Produced

.png)

Importance of Units Of Production Method

The Units of Production depreciation method is useful because it aligns depreciation expenses with the asset's actual use. This is particularly beneficial for businesses where the wear and tear on assets are directly proportional to their level of activity or production.

Example of Units of Production Depreciation

Assume you own a manufacturing machine that costs $50,000, has a $5,000 salvage value, and is estimated to produce 100,000 units throughout its useful life. Each year, the machine actually produces 10,000 units.

Following the unit-of-production depreciation formula, the yearly depreciation expenses will be determined as follows:

Depreciation Expense = Cost of Asset - Salvage Value ÷ Estimated Total Production Units × Actual Units Produced

Depreciation Expense = ($50,000 - $5,000 ÷ 100,00) × 10,000

Depreciation Expense = $4,500

Want to calculate depreciation? Download the free depreciation schedule template from Enerpize

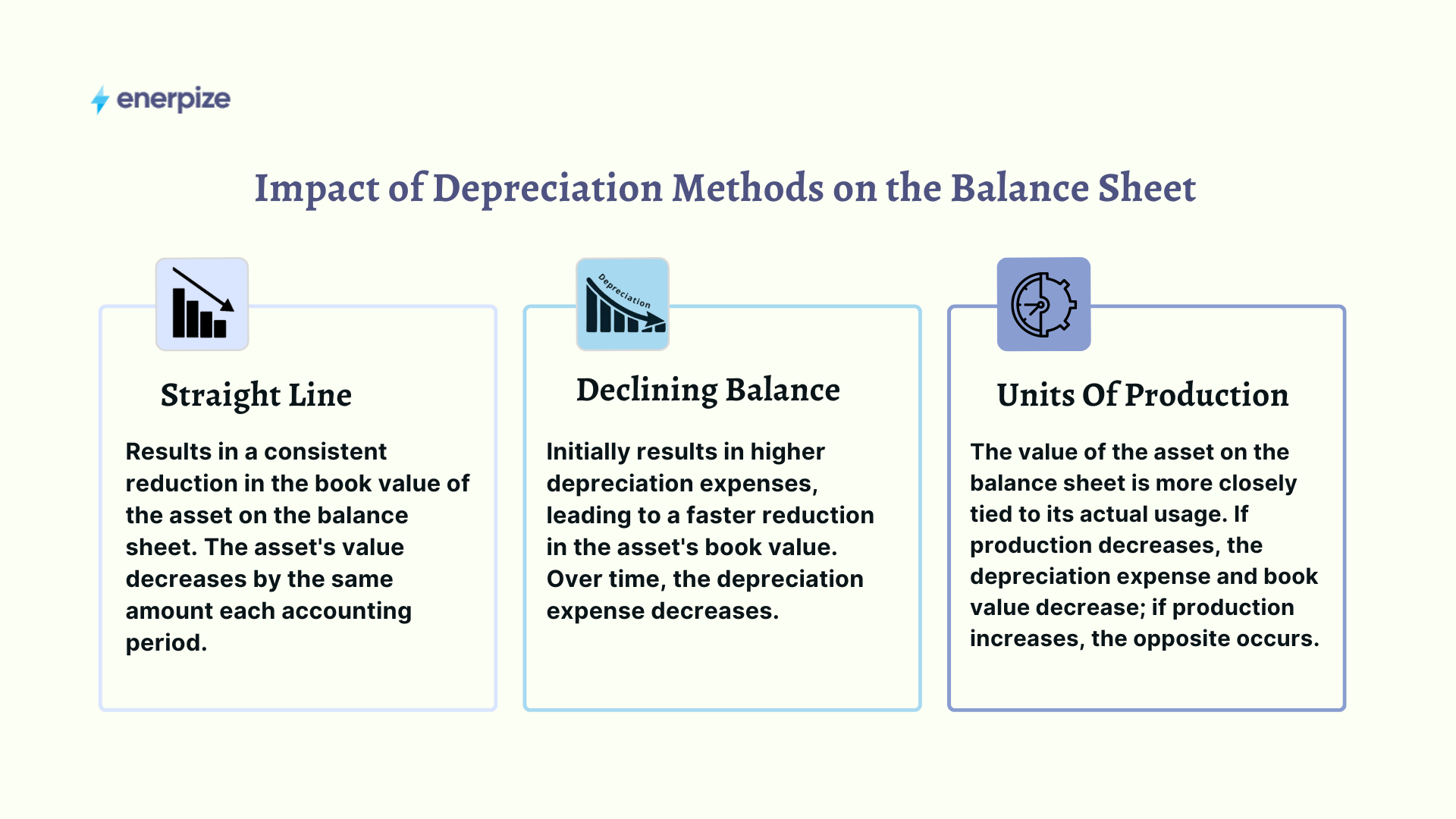

How Depreciation Methods Affect Asset Value on the Balance Sheet

The depreciation method used impacts the time and amount of depreciation expenses reported on the income statement, which in turn affects the asset's book value on the balance sheet.

Companies can select a certain depreciation method depending on several factors, including accounting standards, tax regulations, and the asset's usage. It's essential to consider the financial reporting implications and the effects on financial reporting when choosing a depreciation method.

Here is how each method impacts the balance sheet:

Straight-Line Depreciation: Results in a consistent reduction in the book value of the asset on the balance sheet. The asset's value decreases by the same amount each accounting period.

Declining Balance Depreciation: Initially results in higher depreciation expenses, leading to a faster reduction in the asset's book value. Over time, the depreciation expense decreases.

Units of Production Depreciation: The value of the asset on the balance sheet is more closely tied to its actual usage. If production decreases, the depreciation expense and book value decrease; if production increases, the opposite occurs.

How to Determine Salvage Value

Salvage value, also known as residual value or scrap value, represents the estimated residual worth of an asset at the end of its useful life. Determining salvage value is crucial for calculating depreciation and is often a key component in various depreciation methods. Businesses use different approaches to estimate salvage value:

It's important to note that salvage value is an estimate, and the actual amount realized when the asset is depreciated may differ. External factors such as market conditions, technological advancements, and changes in regulations can impact the actual salvage value.

Salvage value formula:

Purchase Price - ( Depreciation × Useful Life )

.png)

Read Also:

Adjusting Journal Entries: Definition, Types, and Examples

Amortization of Intangible Assets: Methods and How To Calculate

How Can Enerpize Help You with Asset Depreciation

Enerpize streamlines the process of managing asset depreciation by offering flexible and automated solutions. Users can select the most appropriate depreciation method for each asset, whether it be straight-line, declining balance, or production units. Once the method is chosen, users can easily determine the depreciation period and amount. Our fixed asset management software then takes over, automatically updating the periodic depreciation amounts until the end of the asset's life cycle.

This automation ensures that depreciation calculations are accurate and consistent, reducing the risk of human error. By regularly updating depreciation values, Enerpize keeps your financial records up-to-date, providing a clear and precise picture of your assets' value over time.

Depreciation calculation is easy with Enerpize.

Try our accounting module to calculate your depreciation

Depreciation calculation is easy with Enerpize.

Try our accounting module to calculate your depreciation