Author : Haya Assem

Reviewed By : Enerpize Team

Financial Accounting and Its Importance: A Detailed Guide

Table of contents:

- What is Financial Accounting?

- Principles of Financial Accounting

- Types of Financial Accounting

- Importance of Financial Accounting For Business

- How Financial Accounting Works?

- 4 Basic Financial Accounting Statements

- How To Use Financial Accounting?

- Examples of Financial Accounting

- Financial Accounting VS Managerial Accounting

- Best Financial Accounting Software

Financial accounting is a fundamental aspect of business that involves recording, summarizing, and reporting the myriad financial transactions arising from business operations over a period of time. It provides a clear and systematic way to track a company's financial performance and position, offering invaluable insights to stakeholders such as investors, creditors, and management.

This article discusses the relevance of financial accounting in the business world, the various types of financial accounting, and practical examples to illustrate its application.

Key Takeaways

- Financial accounting tracks and summarizes all financial transactions of a business, organizing them into clear reports like income statements and balance sheets for a better understanding of performance and position.

- It follows standardized principles such as consistency, reliability, and the matching principle, ensuring that financial data remains accurate and comparable across time and among different entities.

- Depending on the business type and needs, financial accounting can use either the accrual method, which records income and expenses when they occur, or the cash method, which records them when cash is received or paid.

- Financial accounting's main role is to communicate financial information externally, providing stakeholders, investors, and regulatory bodies with reliable insights into the company’s health and operations.

- It produces four essential financial statements: the income statement, balance sheet, cash flow statement, and statement of changes in equity, each offering a different view of financial performance.

What is Financial Accounting?

Financial accounting involves recording and reporting a company's financial activities within a defined timeframe. It involves tracking all money earned and spent by the company and organizing this information into standardized financial statements, such as the income statement, balance sheet, and cash flow statement.

These statements provide a clear image of the business's financial health, showing its profitability, assets, liabilities, and cash flow. Financial accounting follows specific rules and standards to ensure accuracy and consistency, making the information reliable for business owners, investors, and other stakeholders to make informed decisions.

Principles of Financial Accounting

Understanding the fundamental principles of financial accounting is essential to keeping reliable and precise financial records. These principles promote consistent, transparent, and comparable financial reporting, which is critical for businesses, investors, and regulatory agencies. Below are explanations of several key accounting principles that form the foundation of financial accounting practices.

Accrual Principle

The accrual principle requires that revenues and costs be recorded as generated or incurred, regardless of when the cash transactions occur. This implies that income is recognized when earned and expenses are recognized when spent, resulting in a more realistic picture of a company's financial status and performance over time.

Read More About: How to Track Business Expenses?

Cost Principle

The cost principle requires that assets be recorded at their original purchase cost, not at their current market value. This historical cost remains on the financial statements throughout the asset's life, ensuring that the reported figures are objective and verifiable. This principle provides consistency in financial reporting, although it may not always reflect the current market conditions.

Matching Principle

The matching principle requires that expenses be recognized in the same period as the revenues they contributed to generating. This principle ensures that financial statements accurately reflect the costs associated with earning revenue, providing a clear picture of a company's profitability during a specific period. It helps in assessing the true financial performance of the business.

Objectivity Principle

The objectivity principle emphasizes that financial information should be based on objective evidence and verifiable statistics, rather than personal opinions or biases. This ensures that financial statements are credible and can be trusted by external parties such as investors, auditors, and regulators. Objective evidence can include receipts, invoices, and other documents that provide proof of transactions.

Revenue Recognition Principle

The revenue recognition principle states that revenue should be recognized and recorded at the time it is generated and earned, regardless of when the cash is received. This principle ensures that revenue is reported within the correct accounting period, resulting in an accurate representation of a company's financial success. It is critical to compare financial performance from various periods.

Full Disclosure Principle

The full disclosure principle states that all relevant financial information must be completely disclosed in the financial statements. This includes any data that might impact users' understanding of the company's financial situation and performance. Full disclosure ensures transparency and enables stakeholders to make informed decisions based on complete information.

Types of Financial Accounting

Understanding the types of financial accounting is critical for businesses to monitor their financial activity and meet regulatory requirements effectively. Each type of accounting has its procedures and applications. Below, we will explore the essential types of financial accounting.

Accrual Accounting

Accrual accounting is a way of recording transactions as they are earned or incurred, rather than when cash is exchanged. This method gives a more accurate and comprehensive overview of a company's financial status and performance by recognizing revenue and expenses in the period in which they occurred.

For example, if a company provides a service in December but only receives payment in January, the revenue is recorded in December under accrual accounting.

This method aligns with the matching and accrual principles, ensuring that revenue and associated expenses are recorded within the same period. Accrual accounting is widely used and required under Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

Cash Accounting

Cash accounting, on the other hand, only records transactions in which cash is exchanged. Revenues are recognized when cash is received, whereas costs are recorded when cash is disbursed. This method is simpler and often used by small businesses or individuals due to its straightforward nature.

For example, if a company provides a service in December but receives payment in January, the revenue is recorded in January using cash accounting.

While this method gives a clear picture of cash flow, it may not accurately reflect a company's financial performance over a given time since it does not account for receivables and payables.

Importance of Financial Accounting For Business

Financial accounting is critical for business performance and long-term sustainability. It provides a framework for accurately recording, summarizing, and reporting financial transactions, which improves your company's credibility with investors and lenders. Below are key points highlighting the importance of financial accounting:

Standardized Financial Reporting

Financial accounting provides a consistent framework for recording and reporting financial transactions. Businesses that adhere to standards such as GAAP or IFRS ensure that their financial statements are comparable across industries and periods, facilitating better analysis and decision-making.

Enhanced Risk Management

Companies can identify potential risks early by maintaining accurate financial records. Financial accounting provides the data necessary to conduct detailed risk assessments, allowing businesses to implement efficient strategies to reduce financial uncertainty and protect assets.

Enhancing Business Credibility

Transparent financial reporting promotes trust among all stakeholders, including investors, creditors, and employees. Businesses that provide a clear and honest assessment of their financial performance and situation can attract investment, acquire loans, and maintain robust stakeholder relationships.

Regulatory Compliance

Adhering to financial accounting standards ensures that organizations meet regulatory obligations. This compliance helps avoid legal complications, fines, and penalties. The Securities and Exchange Commission (SEC) and other regulatory organizations need accurate financial reporting to safeguard investors and maintain market integrity.

Informed Decision-Making

Accurate and clear financial records are crucial for management to make informed strategic decisions. Financial accounting provides insights into various aspects of the business, such as profitability, cost control, and investment opportunities, aiding in the planning and execution of business strategies.

Improved Accountability

Financial accounting holds businesses accountable by providing a detailed record of their financial transactions and operations. This accountability is crucial for internal control since it aids in monitoring performance, detecting fraud, and ensuring that resources are utilized properly and effectively.

How Financial Accounting Works?

Financial accounting is an organized procedure that includes many critical processes for accurately recording, summarizing, and reporting a company's financial transactions. These steps aid in the creation of financial statements that provide a clear picture of a company's financial health and performance.

Recording Transactions

The first step in financial accounting is to record all financial transactions that occur within the business. This includes identifying and capturing all financial transactions, such as sales, purchases, expenses, and income. Transactions are recorded in the form of journal entries, which operate as the initial point of entry for financial data.

Read Also: Adjusting Journal Entries: Definition, Types, and Examples

Classifying Transactions

After recording, transactions are classified into categories such as assets, liabilities, equity, income, and expenses. This categorization helps in data organization and ensures that related transactions are grouped for accurate analysis and reporting purposes.

Posting to the General Ledger

Classified transactions are then posted to the general ledger, which is a comprehensive record of all the company’s accounts. Each account in the ledger reflects a specific category of transaction, and postings ensure that the financial data is systematically organized for easy retrieval and analysis.

Read Also: General Ledger VS Subledger: A Comprehensive Guide

Adjusting Entries

Before preparing financial statements, adjusting entries are made to account for any accrued or deferred items that have not yet been recorded. These adjustments ensure that revenues and expenses are recognized in the correct accounting period, adhering to the accrual basis of accounting.

Preparing Financial Statements

The financial statements are created using the adjusted trial balance. The major financial statements are the trial balance, income statement, and cash flow statement.

Closing Entries

Closing entries are made at the end of the accounting period to shift the balances from temporary accounts—such as income, expenses, and dividends—into permanent accounts like retained earnings. This action resets the temporary accounts to zero, ensuring they are ready for the upcoming accounting period.

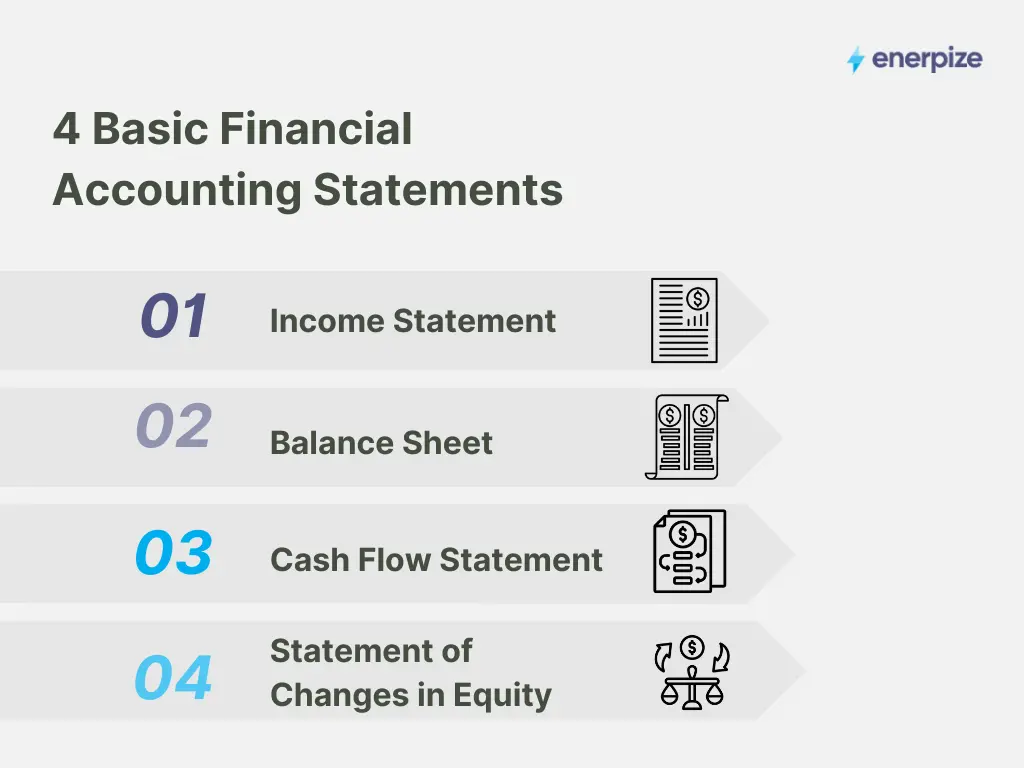

4 Basic Financial Accounting Statements

Financial accounting revolves around the preparation of four primary financial statements that provide a comprehensive overview of a company’s financial performance and position. Investors, creditors, management, and other stakeholders rely on these disclosures to assess a company's financial health. The four basic financial accounting statements are:

1. Income Statement

The income statement, also known as the profit and loss statement, provides a summary of a company’s revenues, expenses, and profits over a specific period, such as a quarter or a year.

The income statement helps stakeholders understand the profitability of the business, identify trends in income and expenses, and evaluate overall financial performance.

Key Components

- Revenue: Total income earned from sales of products or services.

- Expenses: Costs incurred in the process of earning revenue, including operating expenses, cost of goods sold (COGS), and non-operating expenses.

- Net Income: The remaining amount (profit or loss) after subtracting all expenses from total revenue.

Recommended for you: What is a Profit and Loss Statement and How to Analyze?

2. Balance Sheet

The balance sheet presents an overview of the company’s financial state at a specific period of time. detailing its assets, liabilities, and equity. The balance sheet provides insights into the company’s solvency and financial stability, helping stakeholders assess its ability to meet short-term and long-term obligations.

Key Components

- Assets: Resources owned by the company, classified as current (e.g., cash, accounts receivable) and non-current (e.g., property, equipment).

- Liabilities: Obligations owed to external parties, classified as current (e.g., accounts payable) and long-term (e.g., loans, bonds).

- Equity: The residual interest in the assets of the company after deducting liabilities, including common stock and retained earnings.

Read Also: Main Differences Between Income Statement and Balance Sheet

3. Cash Flow Statement

The cash flow statement reports the cash inflows and outflows from operating, investing, and financing activities over a specific period. The cash flow statement provides a detailed view of how the company generates and uses cash, highlighting its liquidity and financial flexibility.

Key Components

- Operating Activities: Cash flows from primary business operations, such as cash received from customers and cash paid to suppliers.

- Investing Activities: Cash flows from the purchase and sale of long-term assets, such as equipment or investments.

- Financing Activities: Cash flows from transactions with the company’s owners and creditors, such as issuing stock or repaying loans.

4. Statement of Changes in Equity

The statement of changes in equity, also known as the statement of retained earnings, outlines the changes in the company’s equity over a specific period. This statement helps stakeholders understand the factors contributing to changes in equity, including retained earnings and dividends, providing a complete picture of the company’s financial health.

Key Components

- Opening Balance: The equity balance at the beginning of the period.

- Additions: Contributions from owners and net income earned during the period.

- Deductions: Dividends paid and other withdrawals by owners.

- Closing Balance: The balance remained at the end of the accounting period.

How To Use Financial Accounting?

Implementing financial accounting best practices is critical to maintaining accurate financial records, informed decision-making, and regulatory compliance. Regular training and staying up-to-date with the latest standards also improve the effectiveness of financial accounting. Choosing the right accounting software, keeping accurate records, and analyzing financial data regularly can help businesses optimize their financial health and performance.

Set up Accounting Systems

Choose accounting software that is suitable for your business size and industry requirements. Make sure the software supports features like automated bookkeeping, financial reporting, and compliance tracking.

Create a detailed chart of accounts to categorize all of your financial activities. This should include all income, expenses, assets, liabilities, and equity accounts tailored to your business operations.

Read Also:

How to Optimize Your Business Thanks to Accounting Software

6 Reasons that Shows You Why to Use Online Accounting Software

Regular Record-Keeping

Maintain accurate records for all financial transactions regularly and accurately. These records include sales, purchases, salaries wages, and others. Use double-entry accounting to record each transaction in at least two accounts.

To ensure that your records reflect your current financial status, reconcile your bank statements, accounts receivable, and accounts payable regularly. This helps detect errors early and maintain accuracy.

Read Also: Journal Entries for Bank Reconciliation: A Comprehensive Guide

Financial Reporting and Analysis

Regularly prepare key financial statements to assess your financial health and performance. Analyze financial ratios for deeper insights. Compare actual performance against budgets and forecasts to identify and address significant variances.

Budgeting and Forecasting

Set detailed budgets relying on historical financial data and future projections. This helps in setting financial goals and allocating resources efficiently. Use financial models to predict future revenue, expenses, and cash flows. Regularly update these forecasts based on current business conditions and market trends.

Cost Management

Regularly review and analyze your cost structures. Identify areas where costs can be reduced without compromising the quality of your products or services.

Compliance and Reporting

Stay compliant with all relevant accounting standards and regulatory requirements. This includes tax laws, financial reporting standards, and industry-specific regulations. Ensure timely and accurate preparation of reports required by tax authorities to avoid penalties and maintain good standing.

Training and Development

Provide training for your accounting staff on financial accounting principles and the use of your accounting software. Ensure they are aware of the latest accounting standards and regulations.

Examples of Financial Accounting

Example 1: XYZ Retail Inc. Shareholders’ Equity

Shareholders’ Equity:

- Shareholders’ equity on January 1: $1,000,000

- Shares issued for cash: $300,000

- Net income: $600,000

- Dividends paid out: ($150,000)

- Total Shareholders’ Equity on December 31: $1,750,000

Example 2: DEF Services Income Statement for 2024

Revenues:

- Net sales: $800,000

- Other revenue: $20,000

- Returned services: ($5,000)

- Total revenues: $815,000

Cost of services provided: $250,000

Gross profit: $565,000

Expenses:

- Accounting: $3,000

- Marketing: $30,000

- Employee payroll tax: $20,000

- Wages: $200,000

- Insurance premiums: $3,500

- Office supplies: $1,500

- Utilities: $4,000

- Total expenses: $262,000

Net income before taxes: $303,000

Financial Accounting VS Managerial Accounting

Financial accounting and managerial accounting serve distinct purposes and audiences, with major differences in approach and focus. Financial accounting provides standardized financial information to external stakeholders such as investors and regulators in accordance with GAAP or IFRS, with an emphasis on historical data through periodic reports such as income statements and balance sheets.

Managerial accounting, on the other hand, serves internal stakeholders such as managers by providing customized reports for decision-making, planning, and control. It focuses on both past and future data, providing extensive, frequently real-time reports tailored to departments or projects, and is not bound by standardized regulations.

While financial accounting seeks to present a realistic financial image to external parties through objective, aggregate data, managerial accounting helps internal management by providing subjective, specific information tailored to their requirements.

Best Financial Accounting Software

Enerpize is a comprehensive financial accounting software that streamlines financial management for businesses of all sizes. It features a user-friendly interface, detailed financial reporting, and a customizable chart of accounts.

Our online accounting software automates processes like invoicing, billing, and payroll, ensuring accurate and timely transaction recording. Real-time financial data enables informed decision-making, while robust security measures and compliance with accounting standards provide peace of mind.

Enerpize also offers excellent customer support and flexible, cost-effective pricing plans, making it an invaluable and affordable tool for efficient financial management.

Financial Accounting is easy with Enerpize.

Try our accounting module to manage your business finances.

Financial Accounting is easy with Enerpize.

Try our accounting module to manage your business finances.