Author : Mohamed Tantawy

Reviewed By : Enerpize Team

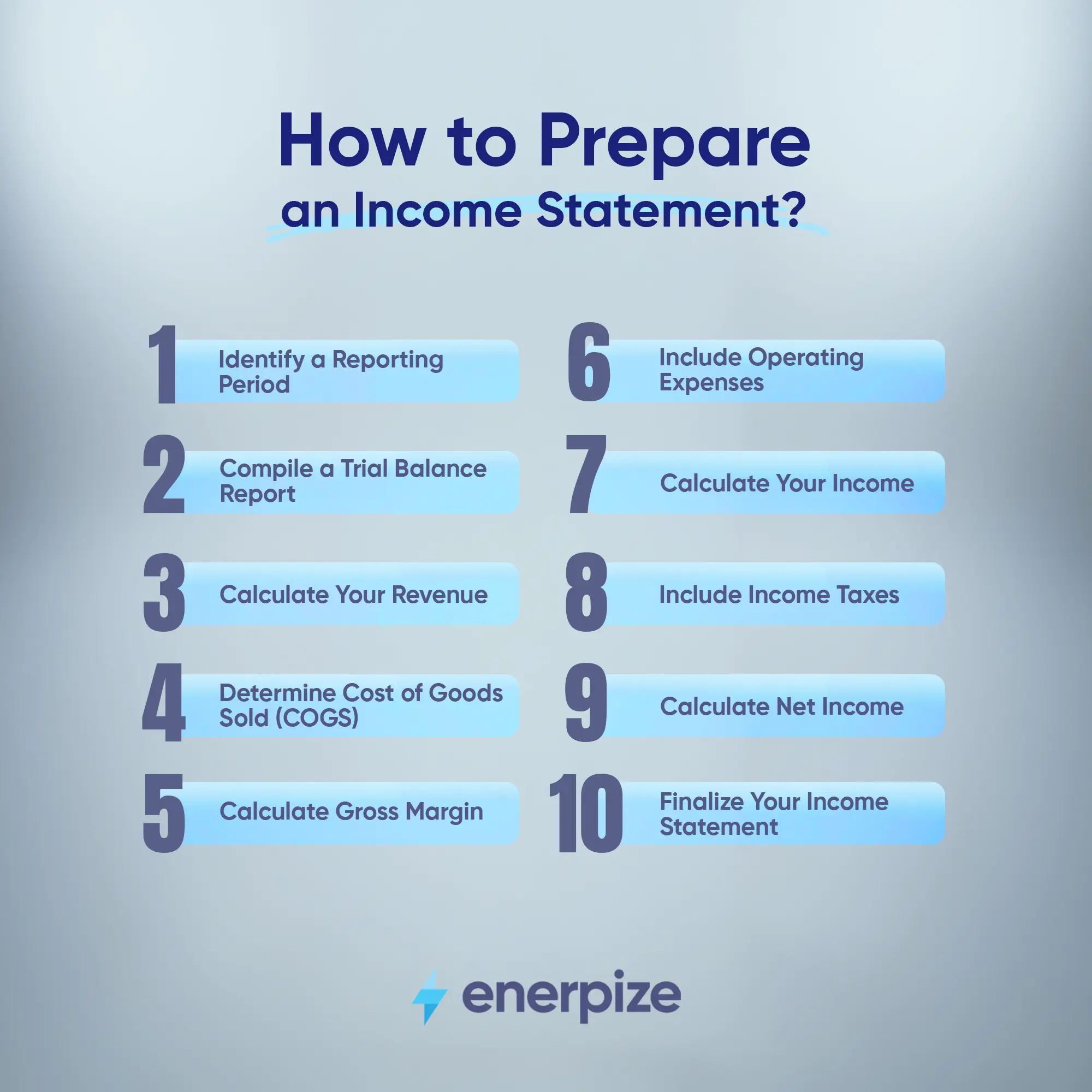

How To Create An Income Statement: 10 Steps

All companies must account for revenue and expenses in a given reporting period. There is every reason to do so: regulatory oversight, internal financial control, expedited profit and loss reporting over a short span, and more.

Typically, an income statement is created to account for a company’s revenues and expenses. It amounts to a business income statement where a given company can assess—using detailed financial information—its current or future operational or non-operational revenue and expense position.

As a business owner or executive manager, you need to know specific steps to learn how to prepare an income statement. You must also learn how to fill out an income statement using an income statement sheet.

To understand what an income statement is, how to create an income statement, how to write an income statement, and more, read on to be best prepared to get your revenue and expenses in perfect order.

Key Takeaways

- An income statement shows a company’s revenue and expenses over a set period, helping assess profitability and guide financial planning.

- It starts by choosing the reporting period and gathering accurate figures from the trial balance, ensuring data is up to date.

- Revenue includes all earned income during the period. COGS is then calculated to reflect the direct costs of producing goods or services.

- Gross margin is found by subtracting COGS from revenue. Operating expenses like wages and rent are then deducted for clarity on operations.

- Pre-tax income is the result of subtracting operating costs from gross margin. Taxes are applied based on local rates to find the total tax owed.

- Net income is calculated by subtracting taxes from pre-tax income. It shows actual profit and helps in evaluating business success.

- Using accounting software automates income statement preparation, reduces errors, and offers real-time insights for better decision-making.

What is the Income Statement?

The income statement is simply an account of a company’s expenses and revenues over a given reporting period: monthly, quarterly, annually, or whichever suits that company’s business needs, operational mandates, and regulatory requirements.

The income statement, aka the Profit & Loss (P&L) statement, is a critical financial statement every business must have (more about why income statements are essential in a bit).

As a business owner or executive manager, you may need more accounting background and experience to create an income statement. In that case, you might need to hire a pro accountant (or a team) to get your accounting house in order - but that may be an expensive option, particularly if you are operating at a small scale and are boot-strapped.

Or you might opt for an end-to-end accounting solution. That, too, needs some consideration, as explained in a bit.

Then again, why income statements are important anyway?

Importance of Income Statement Usage

Income statements are critical for business financial health. By correctly accounting for expenses and revenues, businesses are best positioned to:

- Identify any expense or revenue gaps so that adjustments can be made accordingly.

- Analyze reported expenses and revenue for better financial planning and management.

- Generate various reports to gain insights into broader market dynamics, business operations, and revenue-generating or loss-making streams.

- Report end-of-period expenses and revenue to relevant regulatory authorities.

- Perform insightful forecasts about your business.

- Decide on optimum automation solutions to scale accounting operations and business processes.

- Scale up or down depending on evolving business needs and market dynamics.

- Generate a range of financial reports for various auditing and regulatory purposes.

The list can go on. These are only a few reasons an income statement is a life-and-death financial document. The bottom line is, income statements are fundamental financial documents businesses stand to gain much crafting right and compliantly and stand to lose just as much, or even more, if done inappropriately.

Now what?

Learning how important income statements are, you need to know how to prepare an income statement.

How to Prepare an Income Statement

As noted, specific steps must be followed to prepare a professional - and, notably, reportable - income statement. These are as follows:

1. Identify a Reporting Period

Intuitively, you need, first of all, to identify a given reporting period over which you create your income statement. That could be over a month, quarter, or year. Or, if you are a small business, reporting periods are less strictly regulated than for bigger businesses.

Identifying a reporting period, however, enables you to identify specific patterns within a broader financial mosaic so you can act in a certain way depending on your findings. For example, you may recognize certain revenue-generating streams from specific products or services where your income surges compared to other products over your identified reporting period. This recognition might lead to sales, marketing, operations, or revenue generation breakthroughs.

2. Compile a Trial Balance Report

The second step in creating an income statement is to put together a trial balance report by culling financial data from your general ledger. Specifically, make a trial balance by pulling expense and revenue data from your ledger, where an end-of-balance record of each account exists. That way, you get all end-balance figures required to create your income statement.

Read Alos: Key Differences between General Ledger and Trial Balance

3. Calculate Your Revenue

Calculating how much your business makes is a starting point in creating your overall income and spend. Start by calculating your overall sales revenue over your identified reporting period. Specifically, add all earned revenue over your identified reporting period - even for income you have yet to receive. Then, after adding all revenue lines from your created trial balance, nest the calculated amount under the revenue line of your P&L.

4. Determine Cost of Goods Sold (COGS)

The COGS covers all costs incurred to produce your products or services, including labor, input material, and overheads. Once identified, add all your COGS recorded in your created trial balance and nest your calculated total under the revenue line of your P&L.

Notably, calculating your COGS may vary substantially if you operate in different markets or if you source your input material from markets where raw materials are extracted at substantially different costs—at considerable cost to your overall bottom line. So, one best practice to calculate your COGS is to properly source your material before going all out and calculating what you have. This is Accounting 101 and should help you leverage your profitability potential should you follow best-in-industry sourcing and accounting practices.

5. Calculate Gross Margin

Gross Margin = Total Revenue - COGS

The gross margin is the gross amount earned from selling your goods and services.

6. Include Operating Expenses

Add up your operating expenses, which are recorded in your created trial balance, and nest your calculated total into the P&L statement right under your gross margin line.

Calculating operating expenses is particularly important to small companies where double-digit growth is a norm for successful companies. Small companies burn so much cash during growth and may even overlook some operational efficiencies for growth’s sake. That might result in operating expenses far beyond what many small companies can afford. That is why minding how much you spend as you grow is essential to keep on track.

7. Calculate Your Income

(Pre-Tax) Income = Gross Margin - Selling & Administrative Expenses

Nest your calculated pre-tax income at the bottom of your P&L.

Pre-tax income is particularly important for companies to determine profitability before tax accounting. While income taxes still need to be calculated, pre-tax income helps companies gain direct insights into profitability—and, perhaps more importantly, operational efficiency—by understanding how in-place business processes and operations leverage organizational performance to maximize earnings and minimize expenses and losses.

8. Include Income Taxes

Income Tax = Applicable State Tax X Pre-Tax Income

Nest your calculated income tax under your calculated pre-tax income in your P&L.

Income tax is mandatory in many jurisdictions, so calculating income tax is a mandate all businesses must abide by in relevant jurisdictions. The tax amounts—and how calculated—companies must pay are a matter of much debate and are subject to many factors at local, national, and international levels. Here is where best-in-industry tax practices come in, where companies must not only calculate and report taxes but must also be attentive to how taxes are calculated, manually or automatically, in different jurisdictions.

9. Calculate Net Income

Net Income = Pre-Tax Income - Income Tax

Nest your calculated net income in the final line item of your P&L.

Net income (aka after-tax income) helps companies determine how much income is at hand and, importantly, make projections about cash flows required to make a wide range of investments, such as buying assets, equipment, M&As, etc. - all of which increase a company’s overall valuation.

Read Also: Cash-Flow Statements: Importance and How to Use

10. Finalize Your P&L

This is a formatting step where you give shape to your income statement for as many formal purposes as you want. Typical formatting of your income statement includes:

- Adding a header to identify your P&L as an income statement.

- Adding your official business details, such as your registered address and contact information.

This finalized income statement is your go-to financial statement of record, giving you immediate insights into your business's performance.

Formatting your income statement is not a light matter. Indeed, your formatted income statement might be a differentiator in deciding whether your statement is or will be accepted by relevant tax authorities. If anything, different jurisdictions have different formatting requirements. Unsurprisingly, tax services include, among many things, preparing income statements after being created to be presentable and reportable to tax authorities.

Download Now: Income Statement Template Excel & Google Sheets

Income Statement Example

For the Year Ended December 31, 2023

| Category | Amount (USD) |

| Revenue | |

| Sales Revenue | 500,000 |

| Service Revenue | 150,000 |

| Total Revenue | 650,000 |

| Cost of Goods Sold (COGS) | |

| Cost of Products Sold | 200,000 |

| Total COGS | 200,000 |

| Gross Profit | 450,000 |

| Operating Expenses | |

| Salaries and Wages | 100,000 |

| Rent | 30,000 |

| Utilities | 5,000 |

| Marketing Expenses | 10,000 |

| Depreciation and Amortization | 20,000 |

| Total Operating Expenses | 165,000 |

| Operating Income | 285,000 |

| Other Income and Expenses | |

| Interest Expense | (5,000) |

| Interest Income | 2,000 |

| Net Other Income/Expense | (3,000) |

| Income Before Tax | 282,000 |

| Income Tax Expense (25%) | 70,500 |

| Net Income | 211,500 |

How to Automate Income Statement with Enerpize?

Enerpize is a leading online accounting software geared to cater to every business’s accounting needs. The multiplatform, multicurrency, and multijurisdiction built-in features are all created and designed with accounting operations management in mind, including generating financial statements such as income statements.

In accounting management, you can go manual with all involved costs, effort, or time.

Or, you can opt for Enerpize’s automated solution, where our end-to-end, cloud-based accounting management solution helps businesses:

- Prepare P&L reports by displaying your overall revenue, expenses, and net income.

- Track expenses and income by adding expenses from any device anywhere so you can allocate and forward billable expenses to customers.

- Define and customize tax brackets and options (GST, VAT, EXP, etc.) according to each jurisdiction’s laws and regulations you are operating in on a monthly, quarterly, or annual basis.

- Track your operational expenses to keep a tab on costs and calculate profitability per product or department.

- List all accounts available for recording in your general ledger.

- Maintain timely and accurate records of all your financial transactions for easy retrieval and compliant auditing.

- Use multiple currencies to cater to different payment methods, currency exchange, and volatility issues in various jurisdictions.

Messing up with your income statement, if done incorrectly, may cost you dearly. So, opting for an optimum accounting management solution is all you need to get your accounting operations up and running and become a game changer for your business.

Try Enerpize’s unmatched features for 14 days for free and reap every accounting benefit every business has stood to gain, getting us aboard.

Final Thoughts

The income statement to a business is a record of expenses and income to a household. A company can only survive if a comprehensive profit and loss statement has been made. Here is where income statements come in.

The importance of income statements cannot be overstated. If you do not know your gains and losses, how can you aim to grow as a business?

With that understanding of income statements, properly creating income statements comes as a no-brainer. To create an accurate and reportable income statement, you need to follow ten specific steps:

- Identify a Reporting Period.

- Compile a Trial Balance Report.

- Calculate Your Revenue.

- Determine Cost of Goods Sold (COGS).

- Calculate Gross Margin.

- Include Operating Expenses.

- Calculate Your Income.

- Include Income Taxes.

- Calculate Net Income.

- Finalize Your P&L.

Following the above steps, a standard in preparing income statements, should ensure your statements are accurate, compliant, and always accessible for any current or future use.

You can create your income statement and a wide range of your financial statements manually or automatically.

Going manual is not only time-consuming but may also lead to unintended human errors, especially in the case of creative accounting practices. These regulatory fines can cause broad damage to your business.

You can also automate your accounting operations by opting for leading and result-oriented solutions like Enerpize.

Income statement is easy with Enerpize.

Try our accounting module to create your financial statements automatically.

Income statement is easy with Enerpize.

Try our accounting module to create your financial statements automatically.