![<?$related_template['Template']['title'];?>](/files/business_templates/discounted_cash_flow_template.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/proforma_invoice_template1.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/auto_repair_invoice_template.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/payslip_template.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/sales_invoice_template.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/lease_amortization_schedule_template.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/depreciation_schedule.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/profit_and_loss_statement_template.webp)

![<?$related_template['Template']['title'];?>](/files/business_templates/accounts_receivable.webp)

Create and send online quotations and invoices, track sales, monitor staff performance, and sell & sync all your products via our POS and more.

Posted on 20 March 2025

Amortization Schedule Template Excel & Google Sheets

- The amortization schedule template is available in Excel and Google Sheets.

- It's a structured framework for visualizing loan repayment schedules, ensuring that borrowers understand their financial commitments over time.

- Used for tracking outstanding balances, monitoring interest accumulation, and assessing the impact of extra payments for smarter debt management.

Download it from here:

What is The Amortization Schedule Template?

An amortization schedule template is a structured financial tool that outlines the complete payment plan for a loan, ensuring clarity and predictability in debt repayment. It serves as a roadmap that details each periodic payment over the loan term, breaking it down into principal and interest components. The amortization schedule is handy for fixed-rate loans, where the payment remains constant, but the distribution between principal and interest shifts over time. Initially, a more significant portion of each payment covers the interest, while gradually, more is applied toward reducing the principal. The template provides a complete view of the loan's lifecycle, helping borrowers understand the exact timeline for repayment, the total interest paid over time, and the outstanding loan balance after each installment. Amortization, derived from the Latin word meaning "to die off," signifies the gradual elimination of a financial obligation. This process aids borrowers in financial planning and supports lenders in tracking payment progression.

Importance of Amortization Schedule Template

Provides a Clear View of Loan Repayments

Understanding loan repayment can be complex, but an amortization schedule simplifies it by separating each payment into principal and interest. This transparency allows borrowers to see precisely how their payments contribute to reducing their debt over time. It also highlights how much interest they will pay over the loan’s duration, enabling them to make informed financial decisions about loan terms, refinancing, or early repayments.

Helps Evaluate Loan Options

Comparing different loan offers can be challenging without a clear perspective on how interest rates and loan durations affect overall costs. An amortization schedule provides a side-by-side comparison of various loan terms, showing the actual cost of borrowing. This enables borrowers to assess whether a longer loan term with lower monthly payments is financially advantageous or if a shorter loan term with higher payments will save more in interest over time. Lenders, too, use amortization tables to present structured loan options to potential borrowers.

Facilitates Early Repayment Strategies

Making extra payments toward the principal can significantly reduce the total interest paid and shorten the loan term. The amortization schedule highlights how additional contributions affect the remaining balance and overall cost. Borrowers can plan early repayment strategies, ensuring their extra payments are applied correctly.

Aids in Budgeting and Financial Planning

An amortization schedule helps businesses and individuals forecast financial obligations. Borrowers can allocate their budget effectively by providing a clear structure of upcoming payments, avoiding cash flow issues. Companies can use amortization schedules to predict future debt expenses, optimize investment strategies, and plan for capital expenditures while ensuring they meet their loan commitments without financial strain.

Builds Home Equity Strategically

For mortgage holders, tracking amortization is essential for building home equity—the portion of the property owned outright. As more payments go toward reducing the principal, equity increases. Borrowers aiming to tap into their home equity for refinancing, home improvement, or investment purposes can use the schedule to determine the optimal time to leverage their accumulated value.

Who Can Use Amortization Schedule Template?

Homeowners and Mortgage Borrowers

Homeowners with mortgages can use an amortization schedule to track their loan payments, understand how much of their monthly payment goes toward principal and interest, and plan for early repayment strategies. It helps them visualize their home equity growth and assess refinancing opportunities for better loan terms.

Business Owners and Entrepreneurs

Business owners who take out loans for equipment, real estate, or operational expenses can use an amortization schedule to manage their financial obligations. It assists in cash flow planning, ensuring they allocate resources efficiently while maintaining timely debt payments.

Financial Advisors and Accountants

Financial professionals use amortization schedules to advise clients on loan management, repayment strategies, and refinancing decisions. Accountants rely on these schedules to track interest expenses for tax purposes and ensure accurate financial reporting for businesses and individuals.

Lenders and Financial Institutions

Banks, credit unions, and other lenders use amortization schedules to structure loan repayment plans for borrowers. These help financial institutions track outstanding balances, interest accruals, and payment progress, ensuring compliance with lending agreements.

Students and Personal Loan Borrowers

Individuals with student or personal loans can benefit from amortization schedules to understand repayment timelines and interest costs. By reviewing the schedule, borrowers can explore extra payments, refinancing, or debt consolidation options to manage their financial commitments more effectively.

Real Estate Investors

Investors who finance property purchases through loans can use amortization schedules to assess their long-term financial obligations. Understanding how loan payments affect cash flow and equity growth enables real estate investors to make informed decisions about property financing and portfolio expansion.

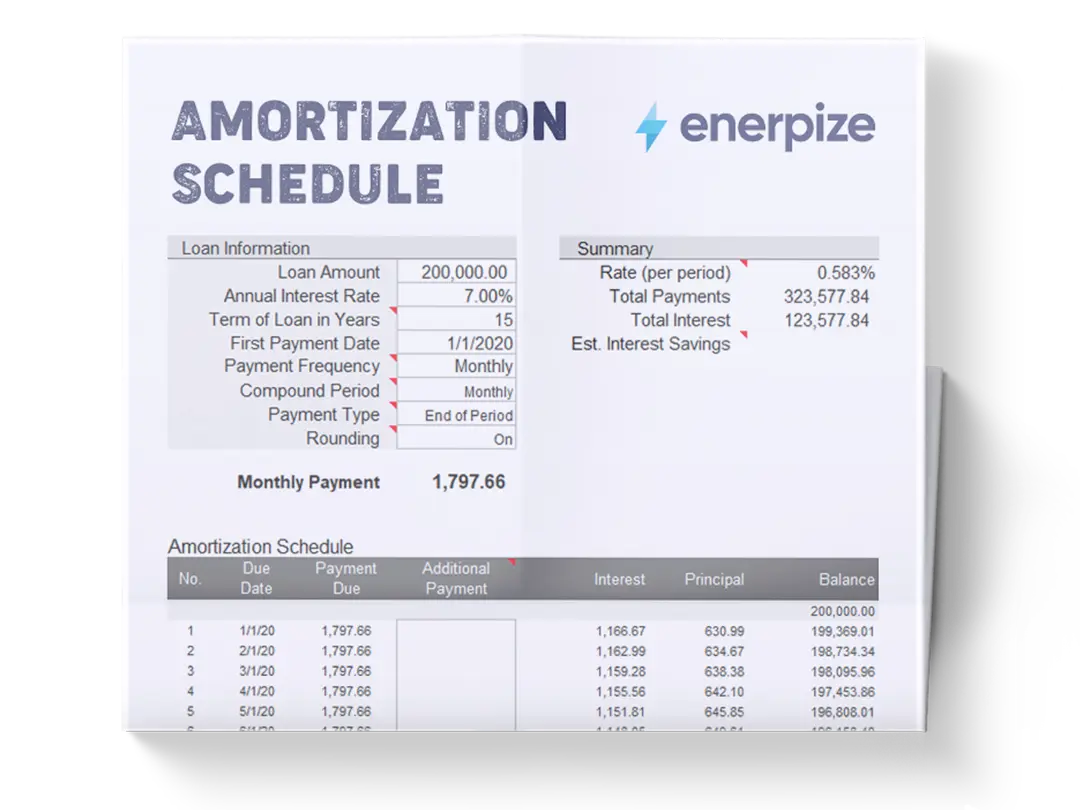

What Does The Amortization Schedule Template Contain?

1- Lender Details:

All lender information includes the lender’s name, address, phone number, and email. These details are essential for record-keeping and future correspondence related to the loan.

2- Loan Details:

- Purchase Price: The total cost of the asset or amount financed.

- Percent Down Payment: The initial upfront payment percentage made by the borrower.

- Total Down Payment: The actual monetary amount of the down payment.

- Loan Amount: The principal amount borrowed after the down payment.

- Annual Interest Rate: The yearly percentage rate charged by the lender.

- Length of Loan in Years: The total duration over which the loan will be repaid.

- Payment Frequency: How often payments are made (e.g., monthly, bi-weekly).

- Monthly Interest Rate: The interest rate applied each month is calculated from the annual rate.

- Monthly Payment: The fixed amount paid each period, encompassing both principal and interest.

- Number of Payments: Total count of installments over the loan term.

- Interest Total: Cumulative interest paid over the life of the loan.

- First Payment Date: Scheduled date for the initial payment.

3- Amortization Schedule Table:

- Payment Number (PYMT #): Identifies each installment sequentially.

- Date of Payment: Specifies when each payment is due.

- Beginning Balance: The outstanding loan balance before the payment is applied.

- Scheduled Payment: The fixed amount due each period.

- Additional Payment (if any): Any extra amount paid beyond the scheduled payment to reduce loan principal faster.

- Interest Paid: The portion of the payment applied to loan interest.

- Principal Paid: The portion of the payment that reduces the loan principal.

- Remaining Balance: The loan balance after each payment.

How to Use Amortization Schedule Template?

1- Enter Loan and Borrower Information

Begin by filling out the lender and borrower details. Input essential fields such as the lender’s name, borrower’s name, loan type, and contact information. This ensures clarity and proper documentation for future reference.

2- Input Loan Details

Enter key financial details, including the total purchase price, down payment amount, interest rates, and loan term. Ensure accuracy, as these inputs determine the schedule's calculations.

3- Configure Payment Terms

Set the payment frequency (e.g., monthly, bi-weekly) and input the start date of payments. The template will use these details to generate a structured schedule.

4- Review the Amortization Table

Once the information is entered, the template automatically calculates:

- Scheduled Payments: The recurring payments required to clear the loan.

- Principal and Interest Breakdown: How much of each payment goes toward the principal and interest.

- Remaining Balance Updates: A real-time view of the outstanding loan balance after each payment.

5- Adjust for Extra Payments (Optional)

If you plan to make additional payments, input these amounts in the corresponding column. The template will recalculate the impact on interest savings and loan duration, helping you see potential benefits.

6- Track and Update Regularly

Use the template to track payments over time. Cross-check with bank records to ensure consistency. Regular updates help maintain financial transparency and support long-term planning.

7- Utilize for Financial Planning and Analysis

Beyond basic tracking, leverage the amortization schedule to:

- Evaluate refinancing options by comparing interest savings.

- Plan for early payoff scenarios by analyzing how extra payments reduce total interest.

- Monitor budget alignment by forecasting future financial obligations.