Create and send online quotations and invoices, track sales, monitor staff performance, and sell & sync all your products via our POS and more.

Posted on 7 November 2023

Author : Haya Assem

Reviewed By : Enerpize Team

Author : Haya Assem

Reviewed By : Enerpize Team

Intercompany Transactions Accounting: Definition, Types, How it Works

Table of contents:

- What is intercompany transaction accounting?

- How does intercompany transaction accounting work?

- Different examples of intercompany transactions

- Types of intercompany transaction accounting

- Advantages of intercompany transaction accounting

- How can intercompany transactions be handled?

- How can an ERP system serve the accounting industry?

- Intercompany accounting risks and challenges

- Final thoughts

Intercompany transactions usually occur within a multinational organization with many subsidiaries. Transactions may take place between the parent business and one of its subsidiaries or between two subsidiaries. So, when these transactions occur, the corporation must adhere to the intercompany accounting regulations.

Intercompany transaction accounting guarantees a harmonious financial operation of a multi subsidiaries organization. It focuses on transparency, compliance, and precision. This article digs into the complexities of intercompany transaction accounting, shedding light on the underlying concepts and problems that support the financial stability of today's global corporations.

What is intercompany transaction accounting?

Intercompany transaction accounting is the practice of documenting and managing financial transactions between multiple entities within the same parent company or corporate group. So, intercompany transactions are prevalent in multinational companies and organizations with several subsidiaries or business divisions. These transactions can be depicted in several different forms such as the exchange of products, services, funds, or other assets between the different entities that form the larger corporate structure.

Accounting for intercompany transactions can be complicated, and the accounting treatment of these transactions can have a major influence on a company's financial statements and tax liability. As a result, many businesses collaborate extensively with auditors and tax specialists to verify that their intercompany transactions are compliant and transparent and that they comply with applicable accounting standards and tax rules.

How does intercompany transaction accounting work?

Intercompany transaction accounting is a complicated process that involves the systematic recording, documenting, and reporting of financial interactions between companies or subsidiaries within the same parent company or corporate group.

Documentation: The process starts with creating invoices, purchase orders, contracts, and other essential documents that define the terms and circumstances of the transactions. As these documents serve for documentation and support for the transactions.

Pricing transfers: A critical part of intercompany transaction accounting is determining suitable transfer pricing. Transfer prices should reflect fair market value, ensuring that transactions between connected companies are similar to those between unrelated parties. This procedure helps to avoid tax evasion and guarantees that international transfer pricing regulations are followed.

Recording transactions: The intercompany transaction should be recorded in the accounting records of both entities involved. Furtherly it should be recorded at fair market value, with the relevant accounts debited and credited to represent the value exchange. This includes intercompany transactions journal entries that account for the transactions' revenue, costs, and assets.

Compliance: Accounting standards, tax regulations, and transfer pricing rules must all be followed. Since Different countries may have different legislation governing intercompany transactions; therefore, it's critical to follow these guidelines to avoid legal and financial consequences.

Reconciliation: Intercompany account reconciliation is required on a regular basis to guarantee that the balances in these accounts across multiple organizations match. Hence, any discrepancies should be thoroughly investigated and resolved to maintain financial accuracy.

Reporting: Financial transparency and compliance need transparent and accurate reporting. Companies must provide extensive disclosures about intercompany transactions, particularly related-party transactions, in their financial statements and reports. This reporting assists shareholders, regulators, and other stakeholders in understanding the business group's financial health.

Different examples of intercompany transactions

Intercompany transactions are not only financial in nature; they can also involve the exchange of assets, services, loan transfers, or products between two companies that are owned by the same parent company. These transactions can take many different shapes and fulfill a variety of functions inside the company. Here are some examples of common intercompany transactions:

Intercompany purchases and sales

A subsidiary within the same business group that manufactures a product or offers a service to another subsidiary. For example, subsidiary A offers electronic products, while subsidiary B is a distribution company that purchases products from Company A and resells them at an agreed-upon transfer price.

Intercompany loans

The parent company or a subsidiary can provide a loan or advance funds to another subsidiary. This might be for various reasons, such as financing expansion or meeting short-term liquidity demands.

Intercompany services

Both the parent company and subsidiaries might share services such as IT support, human resources, or accounting services with each other. The providing entity should charge the receiving entity for these services.

Intellectual property transfer

Companies may transfer intellectual property ownership (e.g., software, copyrights, or trademarks) to another subsidiary, sometimes in exchange for royalties or licensing payments.

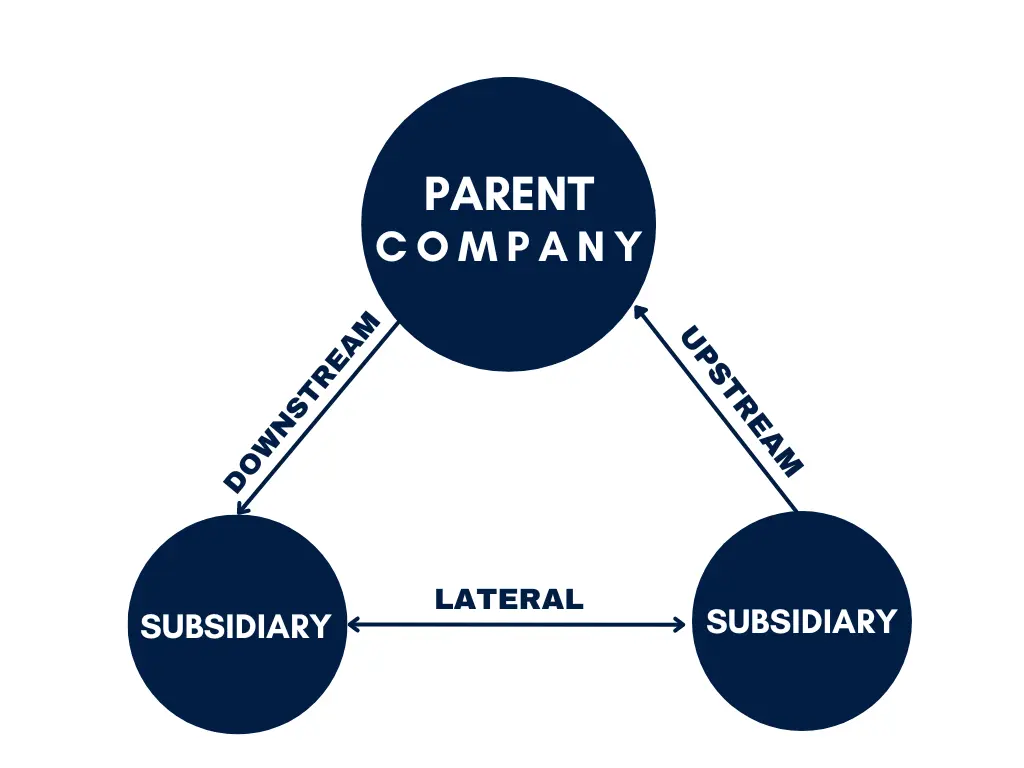

Types of intercompany transaction accounting

Intercompany transactions can be classified into three types, all of which take place within the same business group.

- Downstream transactions: The flow of funds, products, or services is from the parent company to any of its subsidiaries. In this case, the parent company transaction that falls under the classification of "downstream" is a parent company selling an asset to a subsidiary.

- Upstream transactions: The flow is from a subsidiary to the parent company. For example, an upstream transaction occurs when a subsidiary generates revenue from an external customer and pays dividends to its parent company.

- Lateral transactions: The transaction takes place between two subsidiaries of the same business group. For example, if two subsidiaries, a manufacturer and a distributor, exchange services or products, the flow is horizontal, so the transaction is lateral.

Advantages of intercompany transaction accounting

Efficient resource allocation: Intercompany transactions enable corporate groups to efficiently allocate resources. Subsidiaries can collaborate by sharing services, products, and assets, resulting in optimizing the utilization of the group's existing resources.

Cost reduction: Sharing services and goods across subsidiaries or with the main company saves expenses and can achieve cost efficiency.

Consolidated reporting: Accounting for intercompany transactions is required for combining financial statements at the parent company level. This gives a comprehensive perspective of the corporate group's financial performance, making it easier to analyze the organization's overall health.

Tax optimization: Intercompany transactions offer means to optimize a corporate group's tax considerations. Implementing transfer pricing solutions can effectively lower the group's total tax liability while ensuring adherence to tax regulations.

Time-saving: The intercompany transactions accounting procedure saves time when reviewing accounting and financial records at the end of the month, quarter, or year.

Keep track of transactions: Intercompany transaction accounting necessitates the documenting of all transactions done during a specific period of time, and this documentation and records help the accounting department keep track of the company's activities.

How can intercompany transactions be handled?

While intercompany transaction accounting provides various benefits, it is critical to handle these transactions with accuracy, transparency, and adherence to applicable requirements. Failing to do so may result in legal and financial consequences. Subsequently it is usual for companies to employ an ERP system in the accounting, tax, and legal domains to guarantee that intercompany transactions are carried out efficiently and following their strategic goals.

How can an ERP system serve the accounting industry?

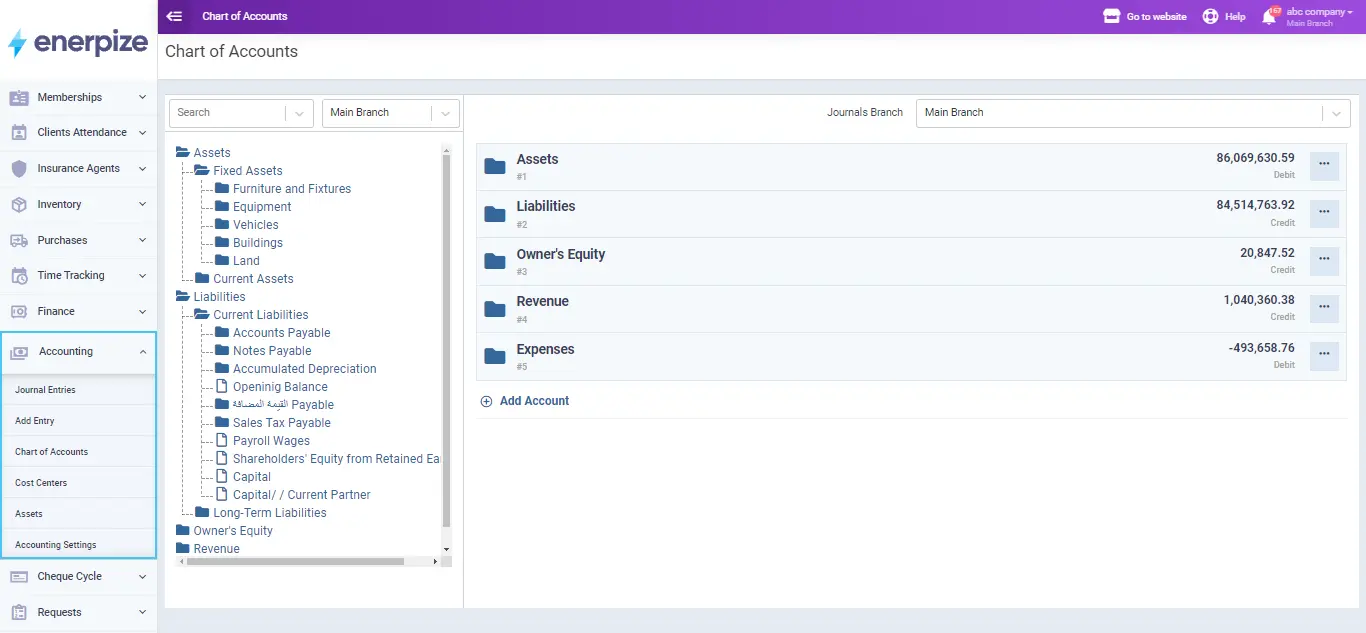

Enterprise Resource Planning (ERP) is a database system that covers all of a company's activities and operations, such as accounting, manufacturing, financial, and human resources. In other words, the purpose of ERP is to have an integrated system for the whole company.

Enerpize is an ERP system built to manage a business’s finance, accounting, sales, invoices, inventory, client relations, HRM, and operations. The accounting module manages and tracks a company’s cash flow, purchases, taxes, profit and loss, balance sheet, sales, chart of accounts, income statement, assets, and everything else to stay on top of your business.

The Enerpize accounting software is critical in enabling and improving the tracking of transactions while also keeping the company in control of all entries, accounting records and automating various accounting operations, including transaction recording, invoice generation, and account payable and receivable management. This automation simplifies transaction processing, eliminating manual work and human error.

Intercompany accounting risks and challenges

Intercompany transactions often encounter numerous challenges due to their complex nature. Multinational corporations with multiple subsidiaries frequently depend on these transactions. Expansion poses one of these challenges, as it typically involves complexities related to local tax regulations, currency issues, transfer pricing, and various systems and applications.

Tax issues are one of the most critical challenges that businesses face. These issues can arise from a variety of sources, including inaccurate transfer pricing, which can result in tax issues, transfer price adjustments, and fines. Transfer pricing plans must be established and documented in order to comply with tax regulations in various jurisdictions.

Companies with subsidiaries in many countries are more likely to confront this type of challenge due to tax regulations that change from one country to another. Failure to follow each country's regulations can lead to legal liabilities, penalties, and reputational damage.

Failing to prepare consolidated financial statements with eliminated entries and proper disclosures can be a high risk for companies because intercompany accounts that are not settled within a reasonable time frame can result in financial misstatements and treasury issues such as unpredictable cash flow, foreign exchange losses, and even fraud.

Inefficiencies and higher risks could result from manual procedures and a lack of automation. So intercompany transactions can be automated to decrease the chance of mistakes and ensure consistency. That is why ERP systems eliminate these errors by precisely recording all transactions, assisting with tax compliance, and preventing human errors.

Effective risk management in intercompany transaction accounting is critical to a company's financial health and reputation. So, to manage these risks and challenges, companies must develop clear policies and processes, invest in ERP and accounting systems, automation, thorough documentation, and conduct regular internal and external audits.

Final thoughts

In short, intercompany transaction accounting is the link between a company and its subsidiaries, and this link is critical for both the parent company and subsidiaries to keep records and documentation of any transactions that occur between them, whether it is a loan provided, a shared service provided, or a product sold from one to the other.

To guarantee accuracy, compliance with relevant accounting standards, and adherence to transfer pricing regulations, each form of intercompany transaction requires specialized accounting treatment and documentation.

Maintaining financial transparency and integrity across complicated business organizations requires proper record-keeping and financial reporting to avoid facing the previously mentioned risks.

Transaction accounting is easy with Enerpize.

Try our accounting module to manage your transactions

Transaction accounting is easy with Enerpize.

Try our accounting module to manage your transactions